Articles

- BLOG / Articles / View

- Articles

Patterson UTI's Perspective in Q3 2025: KEY Takeaways

By Avik on November 17, 2025 in Articles

The Market Outlook

We discussed our initial thoughts about Patterson-UTI Energy's (PTEN) Q3 2025 performance in our short article a few days ago. This article will dive deeper into the industry and its current outlook. According to PTEN’s management in Q3, the U.S. oil production has not yet reflected recent activity cuts. Further declines, however, could pressure global supply in 2026.

In contrast, the natural gas outlook looks favorable as new LNG demand drives plans for higher drilling and completion activity. Despite softer shale activity in 2025, Patterson-UTI’s performance has remained resilient compared to previous downturns. Its drilling and completions technologies are helping maintain margins and strengthen its competitive position.

Completion Market Strategies

Patterson-UTI expects completion activity to stay steady through Q4, with some seasonal slowdown during the holidays. The company plans to invest in high-demand drilling and completions technologies to strengthen its competitive edge and drive strong returns into 2026.

During Q3, it continued to see high demand for the Emerald 100% natural gas-powered fleet. It plans to begin long-term work for the new direct drive pumps in Q4, offering a more capital-efficient alternative to electric frac fleets.

Pricing per horsepower hour in Patterson-UTI’s frac business held steady, though revenue dipped due to fewer low-margin sand and chemical sales. Its new EOS completions platform—featuring Vertex automation, Fleet Stream, and IntelliStim—is advancing AI and machine learning integration in completions.

Drilling and Segment Outlook

Patterson-UTI’s U.S. drilling activity stabilized in Q3 and is expected to hold steady through 2025, with rig revenues in the low to mid-$30,000s per day. Integrated service offerings now support its directional drilling business. The company is enhancing efficiency through Tier 1 APEX rigs and Cortex digital tools like adaptive auto drilling and predictive AI models to boost performance and reduce costs.

Key Drivers and Financial Plans

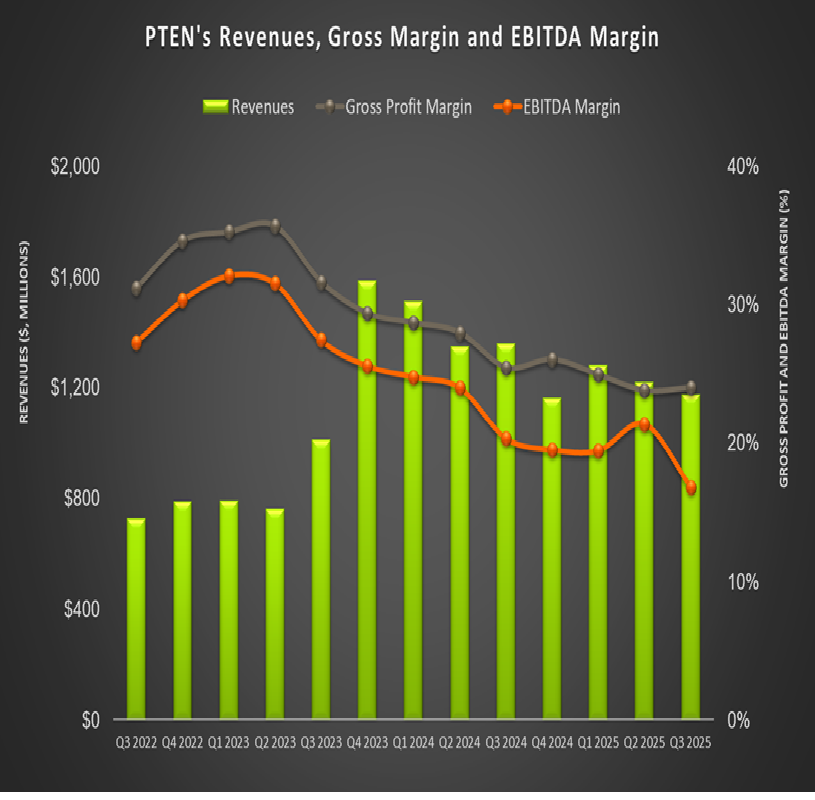

In Q3, PTEN’s Completion Services revenue reached $705 million in Q3, with margins improving due to higher efficiency and earlier cost reductions. Steadier fleet schedules and rising demand in its natural gas fueling business supported performance despite lower low-margin product sales. For Q4, the company expects adjusted gross profit of about $85 million, with less seasonality than last year.

The company expects lower capital spending in 2026 while maintaining high-demand fleet investments and continuing strong free cash flow generation. It remains focused on returning at least half of its free cash flow to shareholders and plans to strengthen capital flexibility through disciplined spending and potential buyback.

Relative Valuation

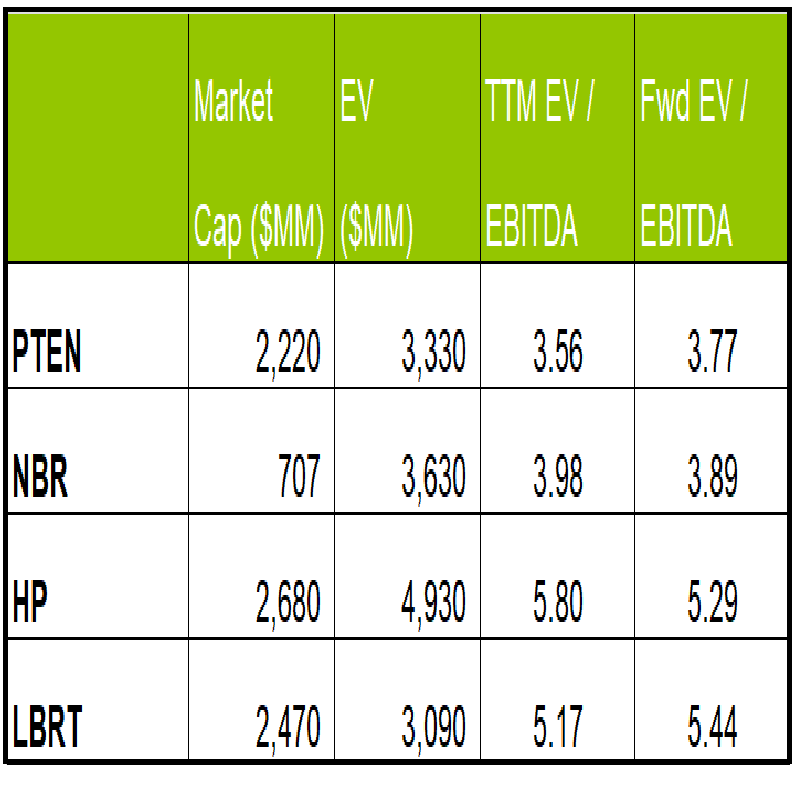

PTEN is currently trading at an EV/EBITDA multiple of 3.6x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 3.8x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 8.4x.

PTEN's forward EV/EBITDA multiple is expected to expand versus the current EV/EBITDA. This contrasts with the fall in the multiple for its peers, as the company's EBITDA is expected to decrease, whereas peers' EBITDA is expected to rise in the next year. This typically results in a much lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (NBR, HP, and LBRT) average. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

PTEN’s steady completions activity, supported by the Emerald natural gas fleet, new direct drive pumps, and the AI-enabled EOS platform, highlights its technology-led efficiency gains. It expects near-term U.S. oil activity to stay soft but sees a stronger outlook for natural gas as LNG-driven demand rises into 2026.

The company’s drilling activity has stabilized, with Tier 1 APEX rigs and Cortex digital tools driving performance improvements and cost reductions across integrated operations. Management plans to keep capital spending lower in 2026 while sustaining high-demand fleet investments, strong free cash flow, and consistent shareholder returns. The stock is reasonably valued, with a negative bias, compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform