Articles

- BLOG / Articles / View

- Articles

Patterson UTI's Perspective in Q4 2025: KEY Takeaways

By Avik on March 6, 2026 in Articles

The Market Outlook

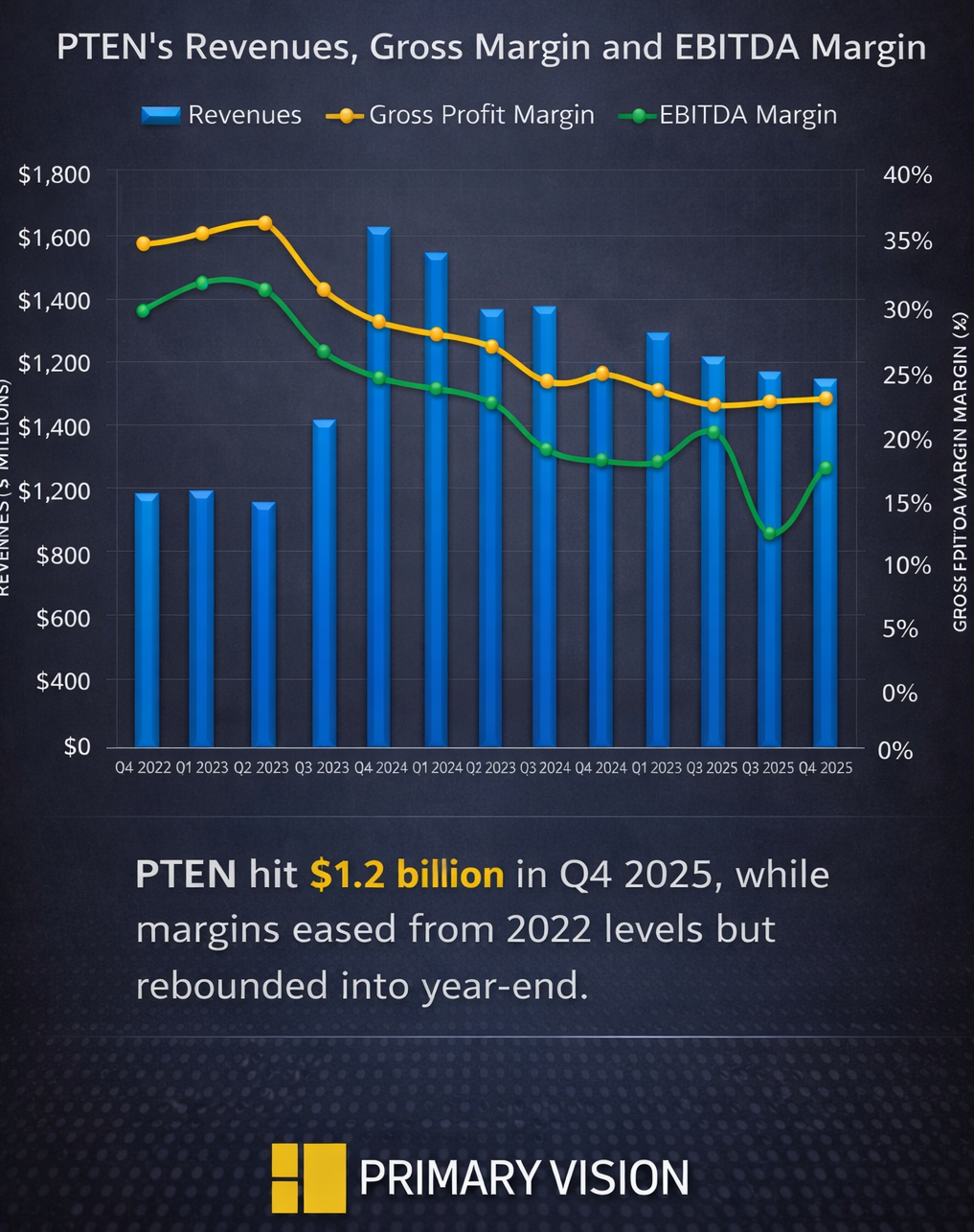

We discussed our initial thoughts about Patterson-UTI Energy's (PTEN) Q4 2025 performance in our short article a few days ago. This article will dive deeper into the industry and its current outlook. According to PTEN’s management, uncertainty is building around whether U.S. oil production can be sustained at current activity levels, as 2025 drilling and completion cuts are now showing up in output. The industry is nearing a crossroads: accept declining production or raise drilling intensity, because operating at lower levels will likely lead to sharper declines.

Long-term natural gas fundamentals remain constructive, but most operators will wait for post-winter price clarity before committing to higher activity, pushing service demand into 2H26. For 2026, oil activity should stay broadly steady near $60 pricing, gas carries upside later in the year, and early-year activity levels are encouraging but far from decisive.

Completion and Pressure Pumping Scenario

Across the industry, reported frac fleet counts are declining, but total deployed horsepower has remained broadly flat due to the shift toward larger fleets per well site. As a result, fleet count has become a weaker indicator of true completion activity than deployed horsepower.

PTEN’s pricing and activity in completions remained steady, with frac assets highly utilized and roughly 2.5 million horsepower either deployed or in maintenance during the first quarter. Spare capacity is minimal. Nameplate horsepower stood at 2.7 million at year-end 2025, down more than 600,000 horsepower versus two years ago. Further reductions are likely as diesel fleets are idled. PTEN is redirecting capital toward 100% natural gas equipment for Emerald, implying fewer operating fleets but a higher-quality pressure-pumping footprint.

Latest Completion Products

PTEN launched its proprietary eos Completions Digital Platform in Q4, giving customers real-time access to live frac data through a single, integrated system. PTEN views eos as a step toward push-button and closed-loop fracturing, with revenue-generating agreements already in place and rising customer interest.

International Drilling Market Outlook

Patterson-UTI is seeing rising international traction as customers increasingly adopt performance-based contracts tied to efficiency gains from advanced rig technology. In Argentina, the company signed a multiyear agreement to lease two high-spec rigs into Vaca Muerta, redeploying idle U.S. assets in a capital-efficient way.

International momentum is further supported by the opening of a new drill-bit manufacturing facility in Saudi Arabia, strengthening its position in the Middle East. Management expects international demand to improve through 2026, favoring differentiated, high-spec rigs as global unconventional drilling activity expands.

Capex Plans

PTEN’s management cut gross FY2026 capEx by about 15% to roughly $500 million in response to the macro environment. After expected asset sales (of idled or legacy diesel rigs, pressure pumping equipment), PTEN expects net capEx to remain below $500 million for the year. The reduction reflects lower maintenance needs driven by digital preventive maintenance, asset high-grading, and facility consolidation. Despite the tighter budget, management expects PTEN to exit 2026 with a more advanced and higher-quality asset base.

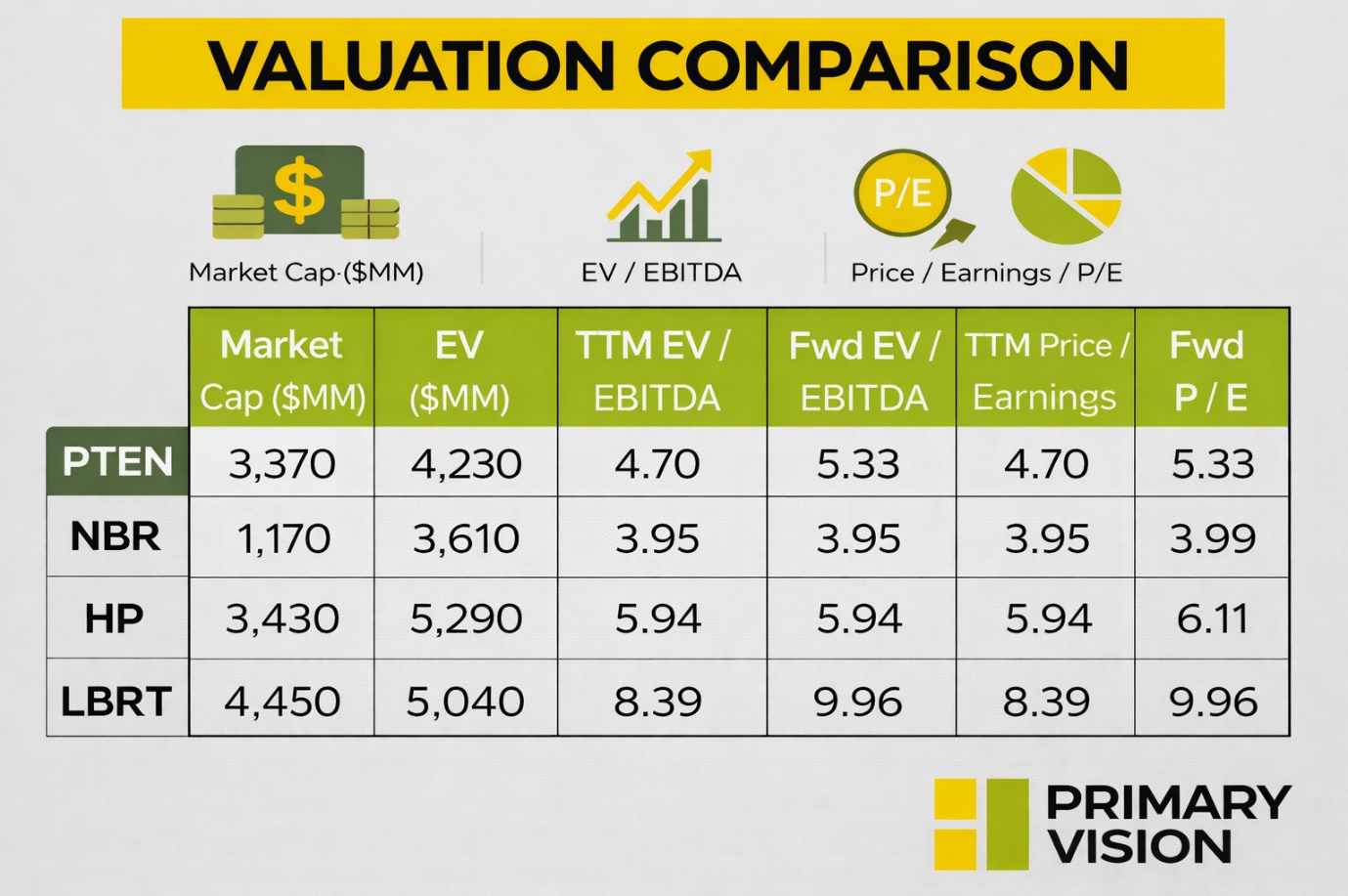

Relative Valuation

PTEN is currently trading at an EV/EBITDA multiple of 4.7x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 5.3x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 8.2x.

PTEN's forward EV/EBITDA multiple contraction versus the current EV/EBITDA is steeper than its peers. This means the company's EBITDA is expected to decrease more sharply than its peers in the next year. This typically results in a lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (NBR, HP, and LBRT) average of 6.1x. So, the stock is reasonably valued compared to its peers.

Final Commentary

PTEN’s management sees U.S. oil production nearing a decision point, as 2025 drilling and completion cuts are now translating into output pressure. Sustaining production likely requires higher drilling intensity, because operating at lower levels risks sharper declines. In completions, deployed horsepower remains tight. PTEN’s ~2.5 million horsepower is largely utilized with minimal spare capacity. The company is deliberately shrinking nameplate horsepower and idling legacy diesel fleets while pivoting toward higher-quality, natural gas–powered pressure pumping assets.

Internationally, momentum is building through redeployed U.S. rigs in Argentina and new manufacturing capacity in Saudi Arabia, improving utilization and positioning for growth through 2026. Against this backdrop, PTEN is cutting CapEx but using asset sales and digital efficiency gains to exit 2026 with a leaner, higher-quality asset base. The stock is reasonably valued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform