Articles

- BLOG / Articles / View

- Articles

ProPetro's Perspective in Q3 2025: KEY Takeaways

By Avik on December 5, 2025 in Articles

Frac'ing Update

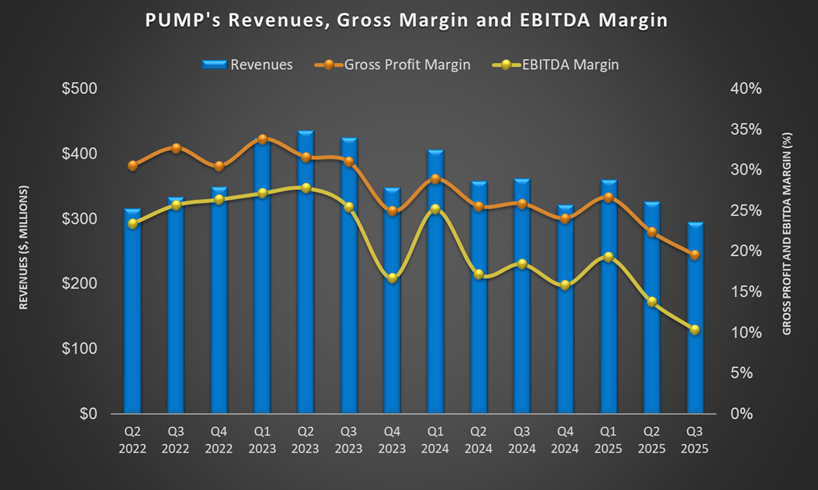

In our short article, we discussed our initial thoughts about ProPetro Holding's (PUMP) Q3 2025 performance a few days ago. This article will dive deeper into the industry and its current outlook. Completions activity in the Permian remains weak, with about 20% dropping at the start of the year. Management expects the tough environment to persist into mid-2026 amid tariff impacts and OPEC+ uncertainty. However, ProPetro looks to stay disciplined. It will likely keep idling uneconomic fleets and leverage its strong balance sheet and high-efficiency assets. The strategy will help it outlast smaller competitors.

ProPetro currently operates 10-11 active frac spreads, of which seven are now contracted. These include two simul-frac units, with about 75% of its fleet powered by next-gen gas-burning equipment. Roughly 70% of its active horsepower is locked into long-term contracts. This provides revenue stability. Its management plans to invest further in FORCE electric fleets. However, customer demand needs to improve before it expands. While completions demand remains weak, ProPetro expects to maintain the current frac spreads (10–11 active fleets) through Q4 and into 2026.

PROPWR Update

Recently, ProPetro landed a 60 MW contract to power a hyperscaler data center in the Midwest. That’s on top of an 80 MW, 10-year oilfield microgrid deal and another in-field power contract with a Permian E&P customer. It’s also close to finalizing a 70 MW long-term contract. This will bring total contracted power above 150 MW, which will likely hit 220 MW by December.

The company has ordered another 140 MW of equipment, pushing total capacity (delivered or on order) to 360 MW by early 2027. Management expects to reach 750 MW by 2028, with each MW costing around $1.1 million. To fund this growth, ProPetro lined up a $350 million lease facility to scale PROPWR without overleveraging. In another development, it paused share repurchases in Q3 to prioritize investment in its PROPWR power business.

Q3 Summary and Balance Sheet

Overall, ProPetro is focusing on capital-light, fast-growing businesses like PROPWR and FORCE electric fleets. The management is staying disciplined, cutting costs where needed to stay lean and efficient. They’ve also built flexibility into operations so they can quickly adjust if activity levels shift.

It plans to invest $200M–$250M in PROPWR in 2026, depending on equipment deliveries and new orders. The 360 megawatts on order are part of a larger goal to hit 750 megawatts by 2028. Liquidity remains solid with $158 million available, supported by $67 million in cash and $91 million of credit capacity.

Relative Valuation

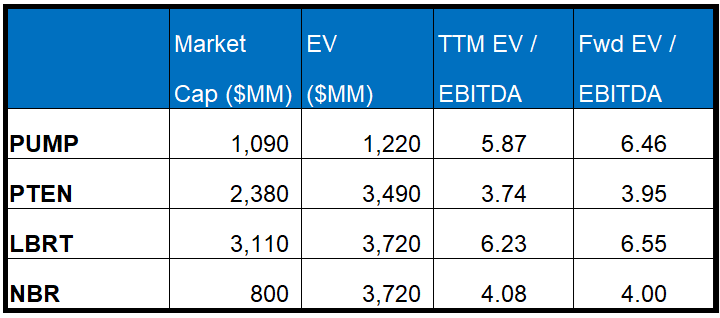

PUMP is currently trading at an EV/EBITDA multiple of 5.9x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 6.7x. The current multiple is above its five-year average EV/EBITDA of 5x.

PUMP's forward EV/EBITDA multiple expansion versus the current EV/EBITDA is steeper than its peers ' because its EBITDA is expected to decrease more sharply than its peers over the next year. This typically results in a lower EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is higher than its peers' (PTEN, LBRT, and NBR) average. So, the stock is overvalued compared to its peers.

Final Commentary

ProPetro continues to face a soft completions market, with weakness likely extending into mid-2026. Management is staying disciplined, idling uneconomic fleets and leaning on its efficient assets and strong balance sheet to preserve margins. Activity levels should remain steady as the company cautiously expands its electric fleet offerings.

Its PROPWR power business is scaling quickly with new long-term contracts and rising demand from both data centers and oilfield operators. Management is funding growth through flexible financing while keeping leverage low. The focus remains on capital-light expansion, cost control, and maintaining solid liquidity to stay agile through the cycle. The stock is overvalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform