Articles

- BLOG / Articles / View

- Articles

ProPetro's Perspective in Q4 2025: KEY Takeaways

By Avik on March 16, 2026 in Articles

Frac'ing Update

In our short article, we discussed our initial thoughts about ProPetro Holding's (PUMP) Q4 2025 performance a few days ago. This article will dive deeper into the industry and its current outlook. Near-term conditions remain challenging into 2026, with about 11 active frac fleets expected in Q1, though winter weather will pressure profitability. PUMP has most of its active frac fleets under contract, supporting near-term stability. The company plans selective investment in FORCE electric equipment but will only commit to it with clear demand visibility and return assurance.

In 2026, capital will target Tier IV DGB refurbishments, fleet automation, and measured additions of direct drive gas units to enhance efficiency. These upgrades are intended to strengthen its Permian positioning and reduce future capital intensity. Pricing remains disciplined, and management will not deploy fleets at subeconomic levels, prioritizing margins and fleet quality over utilization.

PROPWR Update

PUMP’s PROPWR’s five-year growth outlook is intact, with 1H26 focused on derisking and 2H26 expected to begin generating meaningful earnings. PROPWR business advanced in 2025, reaching about 240 MW of committed capacity and deploying its first assets. It ordered another 190 MW, lifting total delivered or on-order capacity to roughly 550 MW. The portfolio is 70% gas reciprocating engines and 30% modular turbines, with delivery expected by 2027 at about $1.1 million per MW.

Management reaffirmed targets of at least 750 MW by 2028 and 1 GW or more by 2030, with flexibility to scale further. Demand from oil and gas remains strong as operators seek efficient microgrids to offset grid constraints in the Permian. Interest from data centers and industrial users is rising and could represent a larger share of future capacity. A recent $163 million equity raise and expanded credit and leasing facilities provide funding flexibility to support this growth.

Capex and Pressure Pump Plans

PUMP expects FY2026 capex of $390–$435 million, with $140–$160 million allocated to completions. About $40M–$50M of that will fund FORCE electric fleet lease buyouts. The original three-year leases helped defer upfront capital while securing attractive returns.

Buying out all five fleets from late 2026 through 2028 will lower lease expense and increase flexibility. Remaining completions capital will support Tier IV DGB refurbishments, automation upgrades, and selective direct drive gas unit investments.

Relative Valuation

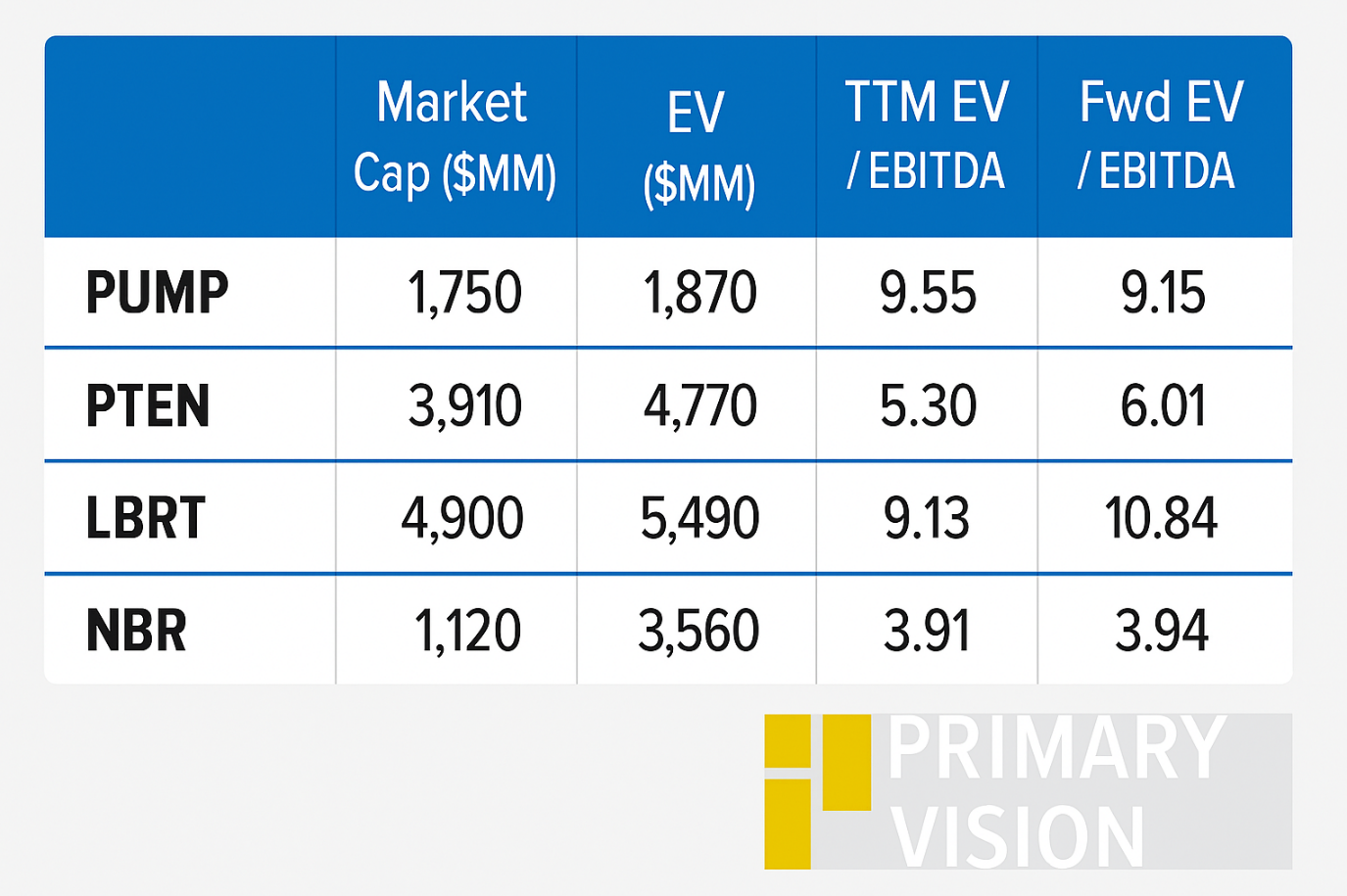

PUMP is currently trading at an EV/EBITDA multiple of 9.6x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 9.2x. The current multiple is above its five-year average EV/EBITDA of 5.1x.

PUMP's forward EV/EBITDA multiple contraction versus the current EV/EBITDA contrasts its peers because its EBITDA is expected to increase as opposed to a rise in EBITDA for its peers over the next year. This typically results in a much higher EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is higher than its peers' (PTEN, LBRT, and NBR) average. So, the stock is reasonably valued compared to its peers.

Final Commentary

ProPetro’s near-term frac markets remain pressured into 2026, with roughly 11 active fleets in Q1 and weather weighing on profitability. However, most fleets are contracted, pricing discipline is intact, and capital is being directed toward efficiency upgrades rather than volume growth. Investment is focused on FORCE electrification, Tier IV DGB refurbishments, automation, and selective direct drive gas units to strengthen Permian positioning and lower future capital intensity.

PROPWR is scaling meaningfully, with 550 MW delivered or on order and a clear path toward 750 MW by 2028 and 1 GW by 2030. A strengthened balance sheet and structured lease buyouts support disciplined growth while preserving returns. The stock is reasonably valued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform