Q3 Drivers and Q4 Outlook: RPC, Inc. (RES) witnessed a solid Q3 as pressure pumping performed strongly and the coiled tubing topline increased from new equipment deployment. Downhole tools demand stayed strong, supported by new product launches. Rental and wireline also saw modest gains.

RES’s management noted market stabilization late in the quarter. However, it warned that “the oilfield services market is likely to face additional headwinds.” The company plans to stay cautious on spending, focus on cost control, and invest selectively for long-term returns.

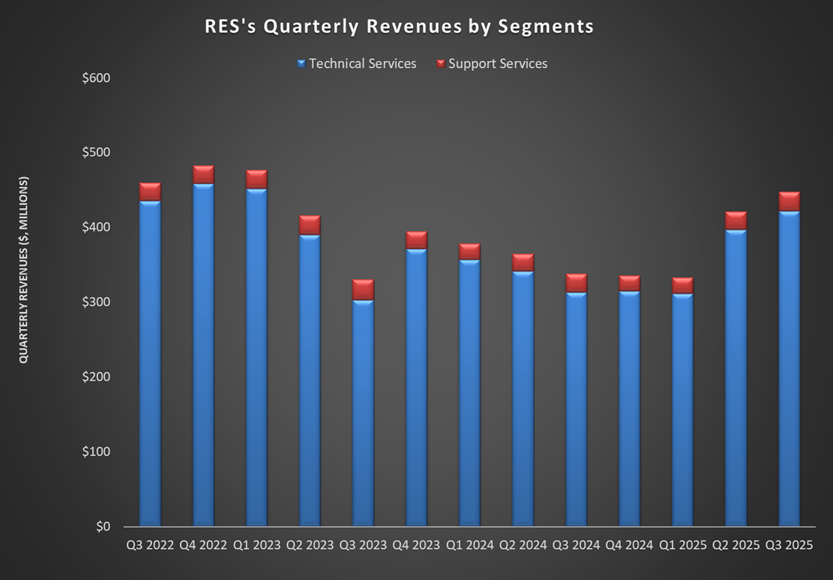

Segment Performance

Quarter-over-quarter, RPC's (RES) revenues increased by 6% in Q3, driven by strong growth in pressure pumping, downhole tools, and rental activity across both Technical and Support Services segments. Its adjusted EBITDA margin expanded modestly, by 60 basis points, as adjustments related to the Pintail acquisition costs impacted the margin in Q3.

The company’s operating income in the Technical Services segment increased by 16% quarter-over-quarter, while operating income in the Support Services segment remained nearly unchanged. The company's adjusted net income increased by 5% in Q3.

RES's FCF Decreased: RES incurred $50 million of debt (notes payable) as of September 30. This, along with a cash balance of $163 million and a $100 million revolving credit facility, allowed for the maintenance of a dividend payment of $0.04 per share. Cash flow from operations decreased by 45% in 9M 2025, while free cash flow decreased by 71% in the past year.

Thanks for reading the RES Take Three, designed to give you three critical takeaways from RES's earnings report. Soon, we will present a second update on RES earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.