Q4 Drivers and Outlook: RPC, Inc.’s (RES) Q4 2025 activity moderated across most service lines, reflecting holiday-related slowdowns and customer pullbacks late in the quarter. Management noted increased volatility in crude prices and a challenging macro backdrop, prompting continued caution on spending and capital deployment. Entering 2026, RPC remains focused on disciplined execution, cost control, and preserving flexibility rather than pursuing growth in a soft market.

Segment Performance

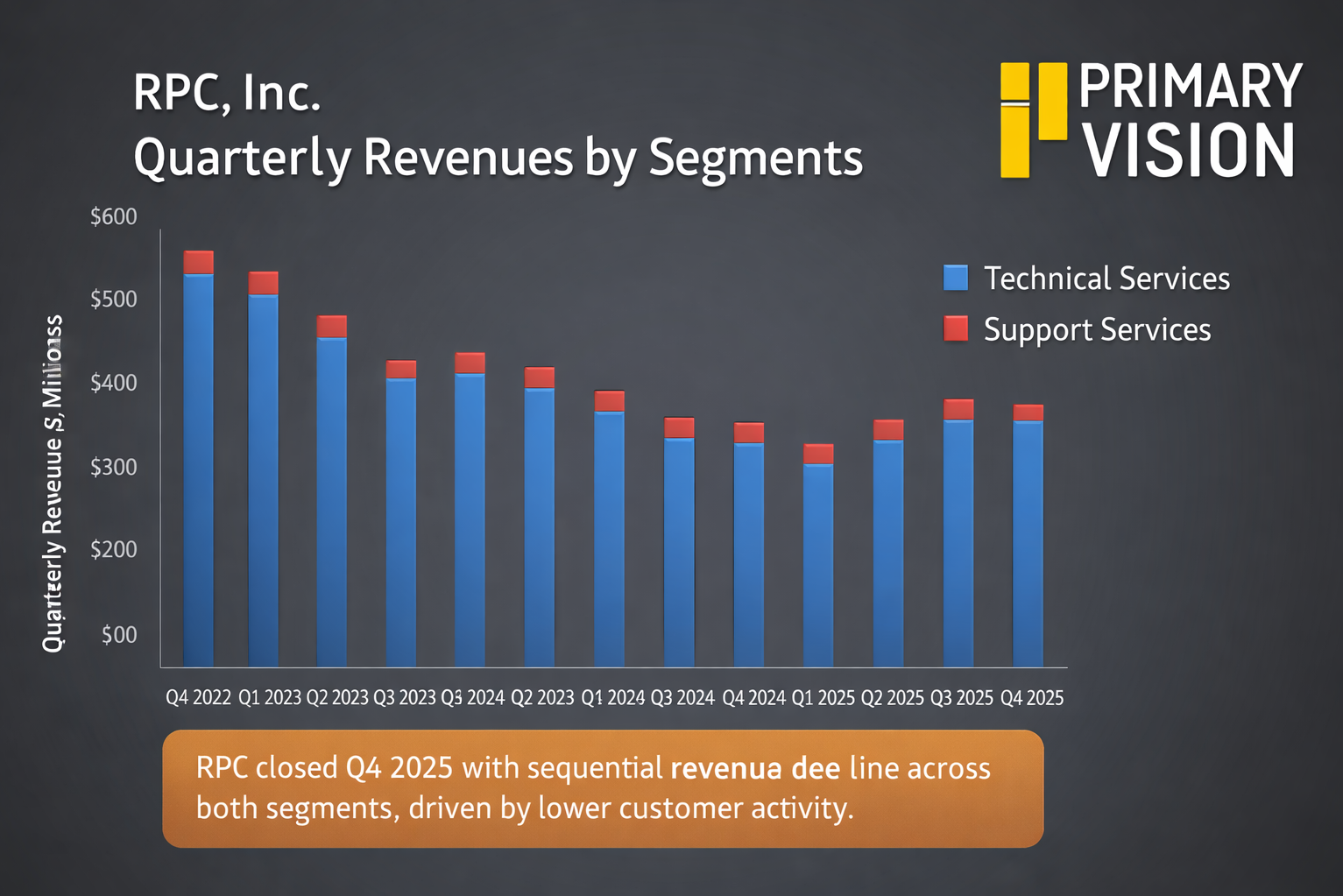

Quarter over quarter, RPC’s revenues declined, driven by weaker performance across both operating segments. Technical Services revenue fell as pressure pumping, downhole tools, wireline, and coiled tubing activity softened, while Support Services saw a sharper decline due to reduced utilization of rental tools, particularly in December.

Segment operating income dipped quarter over quarter, driven primarily by weaker results in Technical Services, while Support Services also softened on lower rental activity. RPC reported a Q4 net loss of $3.1 million, reversing $13.0 million of net income in Q3, which underscored the extent of late-quarter margin pressure.

RES's FCF Weakened: In FY2025, RPC’s cash flow generation declined year over year, reflecting lower earnings and working capital headwinds, while free cash flow also weakened. The company maintained shareholder returns through dividends and modest share repurchases, while leverage increased modestly following debt assumed in connection with acquisitions. Liquidity remained sufficient, providing balance-sheet flexibility despite a more cautious operating outlook.

Thanks for reading the RES Take Three, designed to give you three critical takeaways from RES's earnings report. Soon, we will present a second update on RES earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.