Pressure Pumping Outlook

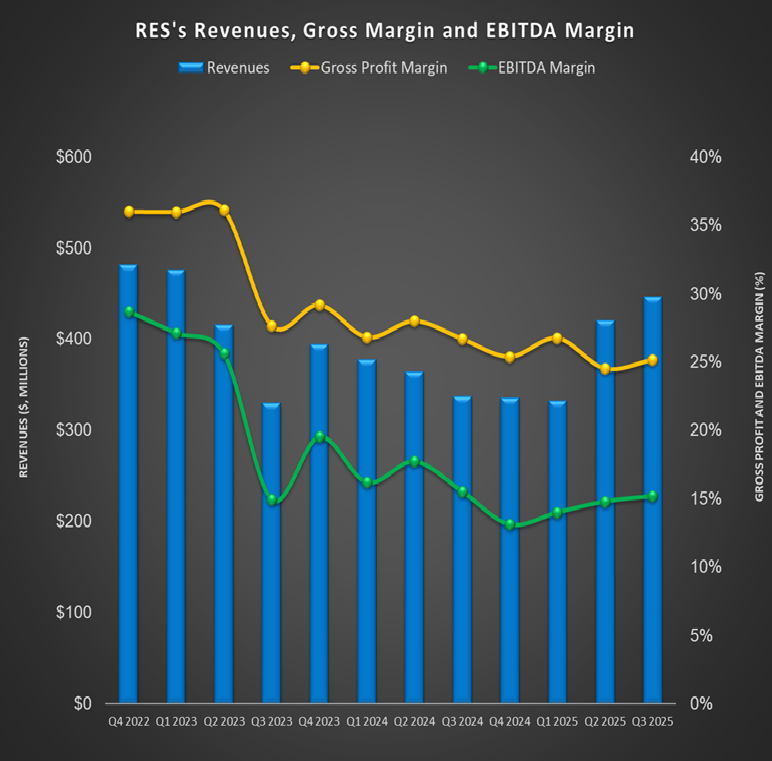

In our recent article, we have already discussed RPC's (RES) Q3 2025 financial performance. Here is an outline of its outlook. RES’s management observes that crude oil price volatility and market uncertainty are creating near-term risks. In this scenario, the management plans to stay disciplined with costs, returns, and capital allocation. RES saw better activity in Q3 as simul-frac jobs increased and downtime dropped. Even so, it idled one fleet in October to protect margins.

The company plans to keep only the most productive fleets active and expects market challenges to persist. It’s testing a fully natural gas-powered frac pump and another unit with a different design to assess new tech options. Management remains focused on shareholder returns and using its balance sheet strength to expand low-capex service lines..

Pressure Pumping Challenges

Pressure pumping now makes up a much smaller share of total revenue than before. Management sees some opportunities but isn’t investing heavily in the segment. The focus is shifting toward less capital-intensive service lines while maintaining discipline on future pressure pumping investments.

Other Completion Activities

RES is strengthening its Thru-Tubing Solutions to get a lead in downhole technology with strong adoption of its new A10 motor. The tool has shown excellent performance in long laterals and helped capture market share. The company is also promoting its Unplugged technology, which cuts drill-out time and can remove the need for bridge plugs. These innovations are expected to reinforce its industry leadership. Meanwhile, Cudd Pressure Control is expanding into gas storage maintenance work, supporting business diversification.

Capex and Balance Sheet Features

The company ended the quarter with strong liquidity, holding $163 million in cash and no debt on its credit facility. It expects full-year 2025 capex of $170–$190 million, mainly for maintenance and system upgrades.

Relative Valuation

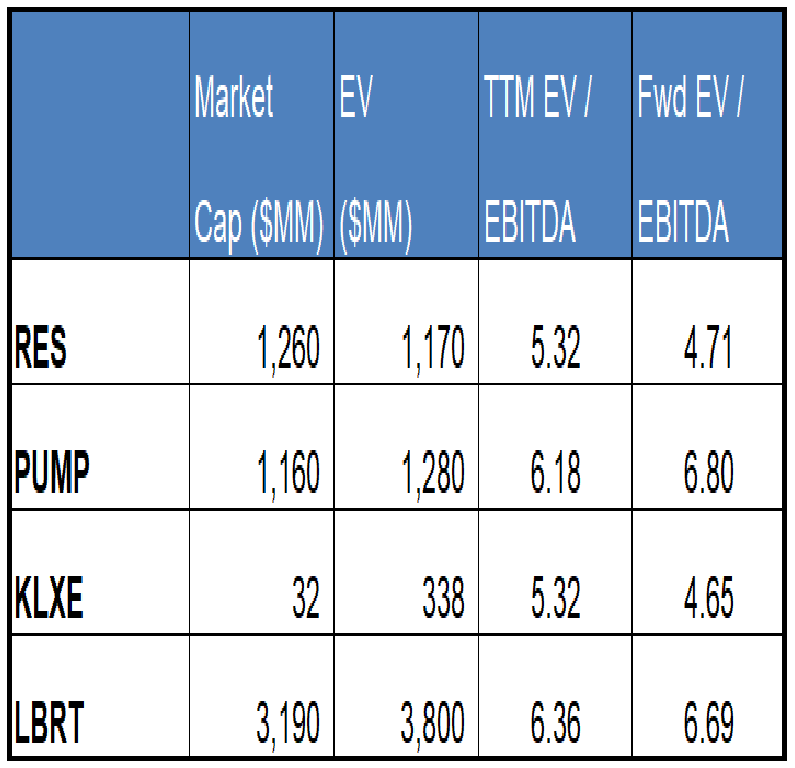

RES is currently trading at an EV/EBITDA multiple of 5.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 4.7x. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 26.7x.

RES's forward EV/EBITDA multiple is expected to contract more steeply than its peers. This implies that the company's EBITDA is expected to increase more sharply than its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple. The stock's EV/EBITDA multiple is slightly lower than its peers' (PUMP, KLXE, and LBRT) average. So, the stock appears to be undervalued compared to its peers.

Final Commentary

RPC stayed disciplined in Q3 as oil price swings and market uncertainty pressured operations. Activity improved with more simul-frac jobs and less downtime, but one fleet was idled in October to protect margins. Management is prioritizing cost control and shifting focus toward low-capex service lines rather than expanding pressure pumping.

Thru-Tubing Solutions is gaining traction with new downhole tools and its Unplugged technology, reinforcing its tech leadership. Liquidity remains solid, and 2025 capex will focus mainly on maintenance and system upgrades. Bottom of Form

The stock appears undervalued compared to its peers.