Articles

- BLOG / Articles / View

- Articles

Shale Breakeven: Basin Differences Are Now About Execution, Not Rock

By Avik on January 21, 2026 in Articles

Investors often talk about shale breakevens as if they are a single magic price. They are not. In the context of fracking, we have explained the break-even prices here. We discussed the significance of the BE prices for some major US energy producers. We even did scenario analysis, assuming a fall in oil price or a move towards lower-tier acreages.

The popular narrative of “$30 oil basins versus $80 oil basins” does not hold when the same framework is applied consistently. That shift in the numbers explains why competitive advantage has moved away from geology and toward execution. If basin economics converge at the full-cycle level, then the winners are no longer determined primarily by rock quality. They are determined by who can run the most efficient operating system.

Bottom of Form

Execution, Not Acreage, Now Defines Basin Competitiveness

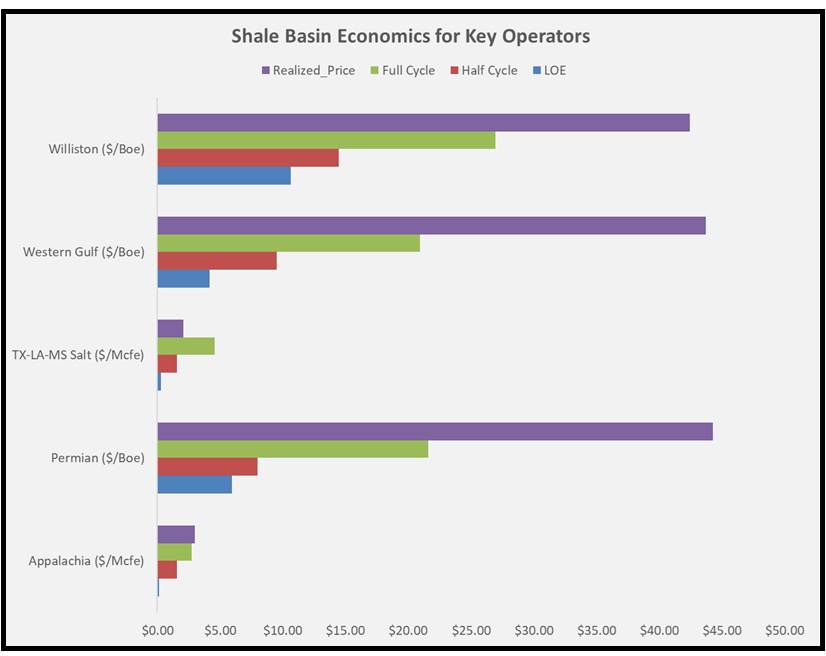

These charts show that shale economics now converge at the basin level once full-cycle costs are applied. Appalachia and TX-LA-MS still look cheapest on operating cost, but their full-cycle breakevens rise toward $3–5/Mcfe. Permian, Western Gulf, and Williston cluster tightly in the low-to-mid $20s per boe despite very different geology. The takeaway is clear: geology no longer explains competitiveness. Execution does.

Appalachia remains structurally low-cost, which is why EQT, Antero, and Expand (formerly Chesapeake, later merged with Southwestern) focus less on LOE and more on pricing, transport, and market access. Efficiency gains now come from higher stages per day, faster drillouts, and better pump-hour performance rather than step-change cost breakthroughs. The basin wins on cost. Outcomes depend on commercial strategy.

Permian economics are no longer exceptional on price, but the basin stays competitive because it industrialized faster than anyone else. SimulFRAC adoption, shorter cycle times, and system-level optimization drive continuous improvement across EOG, Diamondback, and Devon. The efficiency curve is still bending, even as the cost floor stabilizes. This is now a manufacturing advantage, not a rock advantage.

TX-LA-MS (Haynesville-style gas) sits in the middle on cost but has the highest sensitivity to execution. CRK and Expand are cutting well costs through redesigns like horseshoe wells and tighter operational control. The basin works at the cash level. But replacement economics only improve if structural cost per lateral foot keeps falling.

Western Gulf behaves like a portfolio basin. It is not cheap, but it is not broken. Operators such as EOG, Devon, and Coterra rely on system discipline rather than basin-specific advantage. Efficiency here comes from capital allocation and operational consistency, not geology.

Williston remains structurally higher cost. That forces CHRD and Devon to focus on incremental execution gains rather than growth. The basin survives through reliability and discipline, not upside surprise.

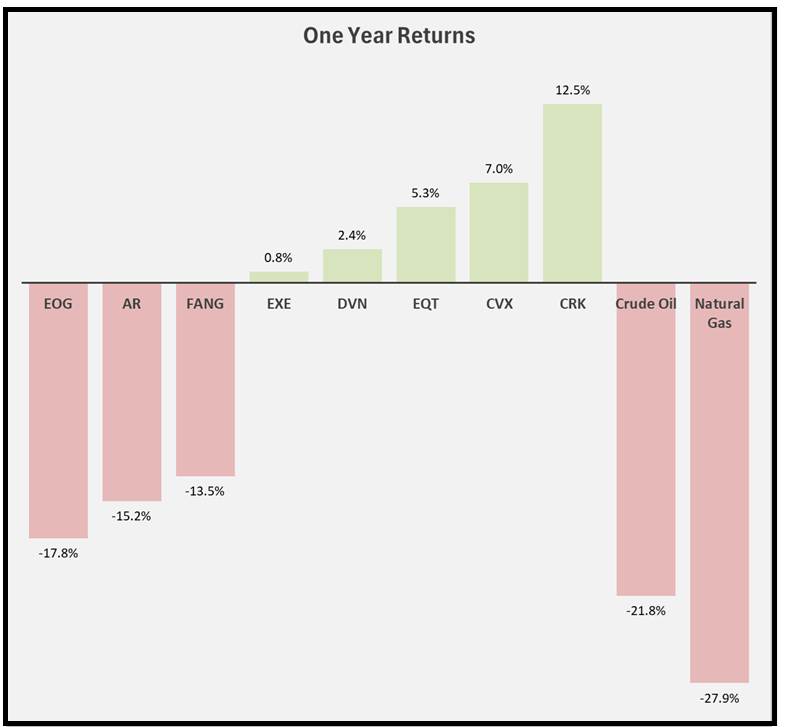

How is the market evaluating?

Breakevens explain which operators can survive. They do not explain recent stock returns. The market is rewarding LNG exposure, balance sheet comfort, and future optionality instead. That is why gas-levered names like CRK and EQT outperform while high-quality operators like EOG and FANG lag.

Bottom line

This model highlights a gap in the prevailing market narrative. When breakevens are measured consistently, basin competitiveness is no longer driven primarily by geology. It is driven by execution, scale, commercial positioning, and the ability to sustain operational improvements over time.

The winners and losers are managed by supply chain management as well. This is why you see some companies are pure play only. It’s why Expand limits itself from going to the Bakken, or Diamondback doesn’t go to the Marcellus. Chevron and Exxon, on the other hand, can operate everywhere because they keep buying companies that have figured out all the logistics, supply chains, etc., so they can leverage them and benefit from them.

Appalachia benefits from structurally low operating costs, but outcomes hinge on pricing and market access. The Permian remains advantaged by scale, yet only the most efficient operators can protect margins. TX-LA-MS Salt gains from proximity to LNG demand, but its economics depend on disciplined drilling and completion costs. Western Gulf outcomes are shaped by portfolio management rather than geology. Williston remains competitive only where operators continuously refine execution.

Shale has matured. The easy gains from rock quality have largely been captured. The next phase of advantage belongs to operators that run shale for what it now is: a manufacturing business built on discipline, repetition, and continuous improvement.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform