Articles

- BLOG / Articles / View

- Articles

SLB's Perspective in Q4 2025: KEY Takeaways

By Avik on February 9, 2026 in Articles

The Market Outlook

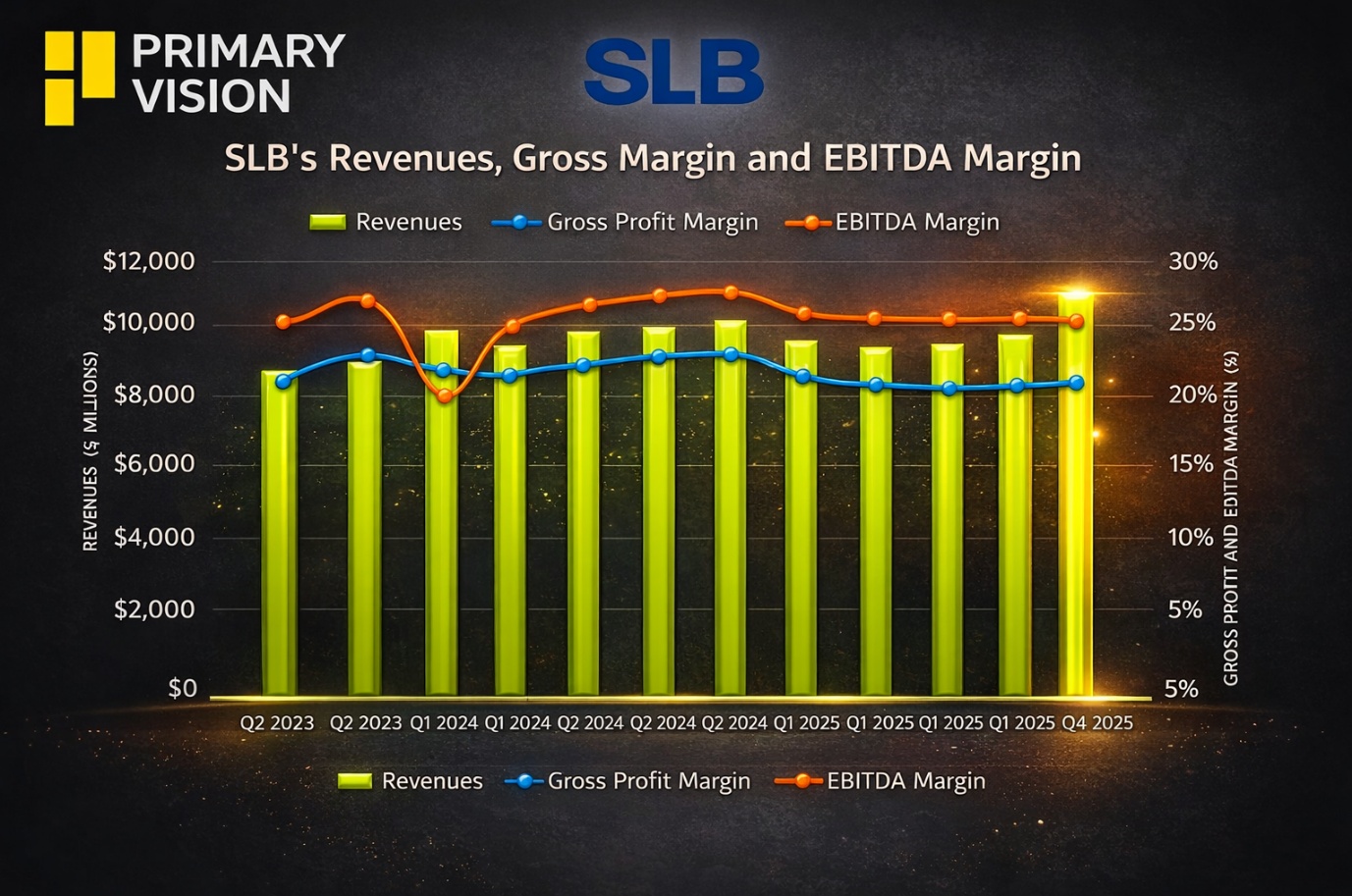

We have already discussed SLB's (SLB) Q4 2025 financial performance in our recent article. Here is an outline of the macro energy environment and the company’s strategies in a changing scenario. The management expects near-term oversupply to keep pressure on prices into H1 2026. So, operators are likely to stay cautious and push spending to the back half. As rebalancing extends into 2027, upstream investment should recover gradually, with international and deepwater exiting 2026 stronger than 2025.

Structural demand from economic growth, AI-driven power needs, and infrastructure spending should support oil and gas consumption. Natural decline rates then do the rest of the tightening. Operators are now focused on the lowest-cost barrels. This means more technology, more integration, and more digital across the asset lifecycle. SLB is leaning into this shift with digital operations and a stronger production portfolio.

International and Offshore Market Outlook

International markets are stabilizing and trending higher, led by Latin America and the Middle East and Asia in 2026. The Middle East remains the largest market, supported by rising oil activity under OPEC+ policy and sustained investment in gas. After mixed growth in 2025, a rebound in Saudi drilling and workover activity is now underway and should lift regional momentum through 2026.

Offshore, especially deepwater, should inflect toward the end of 2026, and SLB believes OneSubsea’s integrated subsea, digital, and well construction capabilities are a clear differentiator. With subsea tree awards expected to rise about 20% versus 2025 and bookings potentially exceeding $9 billion over the next two years, the growth opportunity looks real.

ChampionX and Data Center Push

SLB completed the ChampionX acquisition in July 2025, which strengthened its capabilities in production chemicals and artificial lift. A full year of ChampionX should add about $1.8 billion of revenue in 2026, partly offset by the loss of roughly $350 million from 2025 divestitures. Despite different divisional dynamics, adjusted EBITDA margins are expected to stay broadly in line with 2025.

SLB’s data Center Solutions is scaling faster than expected, with broader offerings, customers, and geographies, and management now expects to exit the year at a $1 billion annualized revenue run rate.

SLB's Guidance

SLB expects FY2026 revenue of $36.9B–$37.7 billion (assuming oil prices remain range-bound in the high-$50s to low-$60s). North America should benefit from ChampionX, offshore activity, and data center growth, although upstream land activity is still expected to decline. International revenue is expected to increase modestly, led by Latin America and the Middle East and Asia, while Europe and Africa are forecast to soften slightly.

In Q1 2026, the company expects revenue to decline “high single digits” sequentially due to the seasonal unwind of strong year-end deliveries. Adjusted EBITDA margin is forecast to contract by “150–200 bps”, with a recovery expected from Q2 onward.

Relative Valuation

SLB is currently trading at an EV/EBITDA multiple of 11x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 9.7x. The current multiple falls short of its five-year average EV/EBITDA multiple of 11.8x.

SLB's forward EV/EBITDA multiple versus the adjusted current EV/EBITDA is expected to contract more steeply than its peers because the company's EBITDA is expected to increase more sharply than its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is similar to its peers' (HAL, BKR, and FTI) average. So, the stock appears undervalued compared to its peers.

Final Commentary

SLB’s management holds a view that near-term oversupply should keep pressure on crude oil prices into 1H 2026, so operator spending is likely to stay cautious. Rebalancing into 2027 should lift upstream investment, with international, offshore, and deepwater exiting 2026 stronger than 2025. Operators are prioritizing lowest-cost barrels, which favors technology, integration, and digital where SLB is increasingly differentiated.

ChampionX and Data Center Solutions add credible new growth, while offshore bookings point to a real medium-term opportunity. FY2026 guidance implies modest top-line growth with a weak Q1, but a better setup into 2H 2026. The stock appears undervalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform