Offshore Strategic Shift

We have already discussed TechnipFMC's (FTI) Q4 2025 financial performance in our recent article. This article will dive deeper into the industry and its current outlook. TechnipFMC observes that the operators are shifting from single-project execution to portfolio-wide offshore development strategies. This integrated approach improves standardization, speeds production ramp, and lowers overall costs.

TechnipFMC’s iEPCI model and Subsea 2.0 solutions align directly with this shift, strengthening competitive positioning. Early collaboration is increasing pipeline visibility and improving cost and schedule certainty. Subsea opportunities have risen for six straight quarters to about $29 billion, signaling expanding offshore momentum.

Backlog Growth

Subsea orders reached $2.3 billion in the quarter and $10.1 billion for the year, led by iEPCI projects. TechnipFMC has won five of six sanctioned 20K projects, reinforcing its competitive edge. Here, “20K projects” refer to subsea developments designed for 20,000 psi (20K) pressure-rated equipment. These are next-generation ultra-high-pressure subsea systems.

Three-year inbound exceeded $30 billion, lifting backlog to $15.9 billion with minimal legacy exposure. Direct awards, iEPCI, and Subsea Services now represent over 80% of total inbound, supporting further backlog growth.

Segment Forecast and Outlook

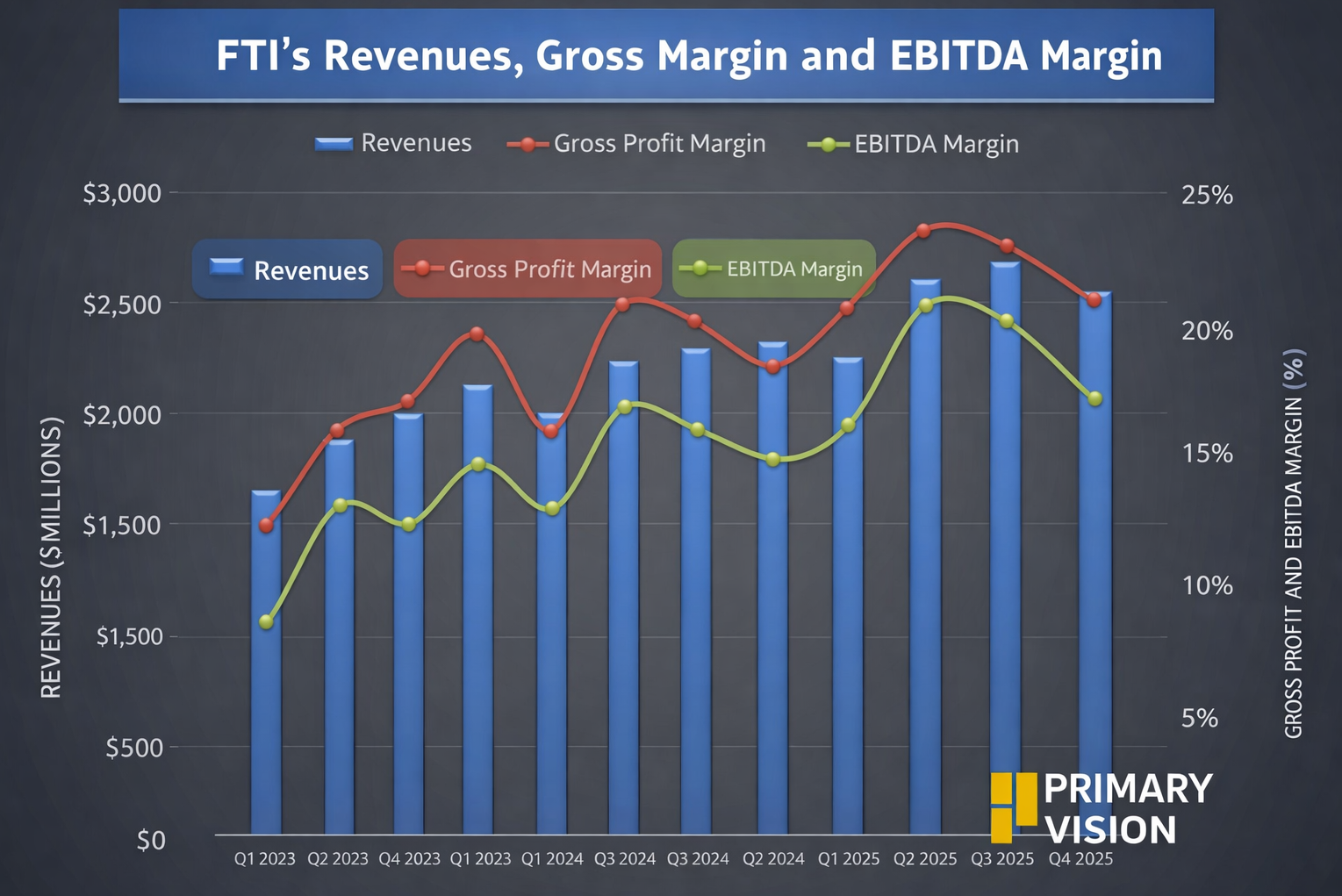

FTI has restructured its Subsea operations to drive efficiency and targets $9.4 billion of revenue with a 21.5% EBITDA margin, implying 16% EBITDA growth. It expects Q1 Subsea revenue to rise low single digits sequentially, with margins improving about 50 basis points.

FTI guides Surface Technologies revenue at just over $1.2 billion with a 17.25% margin, though Q1 revenue should decline around 10% sequentially. The company plans disciplined capex of about $340 million, just over 3% of revenue. It projects $1.3–$1.45 billion of free cash flow and intends to return at least 70% to shareholders.

Relative Valuation

![]()

FTI is currently trading at an EV/adjusted EBITDA multiple of 14.5x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 12.4x. The current multiple is higher than its five-year average EV/EBITDA multiple of 10x.

FTI's forward EV/EBITDA multiple contraction versus the adjusted current EV/EBITDA is steeper than peers' because the company's EBITDA is expected to increase more sharply in the next four quarters. This typically results in a higher EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (SLB, BKR, and HAL) average of 10.6x. So, the stock is reasonably valued compared to its peers.

Final Commentary

It appears that operators are shifting to portfolio-based offshore development, which favors integrated execution and cost efficiency. FTI’s iEPCI model and Subsea 2.0 platform are directly aligned with this trend, strengthening backlog visibility and competitive positioning. Subsea inbound reached $10.1 billion in 2025, with strong 20K project wins and backlog expanding to $15.9 billion.

Management expects Subsea EBITDA to grow 16% in 2026, supported by restructuring and margin expansion. Strong free cash flow generation and disciplined capex underpin a commitment to return at least 70% of cash to shareholders. The stock is reasonably valued compared to its peers.