Articles

- BLOG / Articles / View

- Articles

Weatherford’s Perspective in Q4 2025: KEY Takeaways

By Avik on March 2, 2026 in Articles

Completion Market Strategies

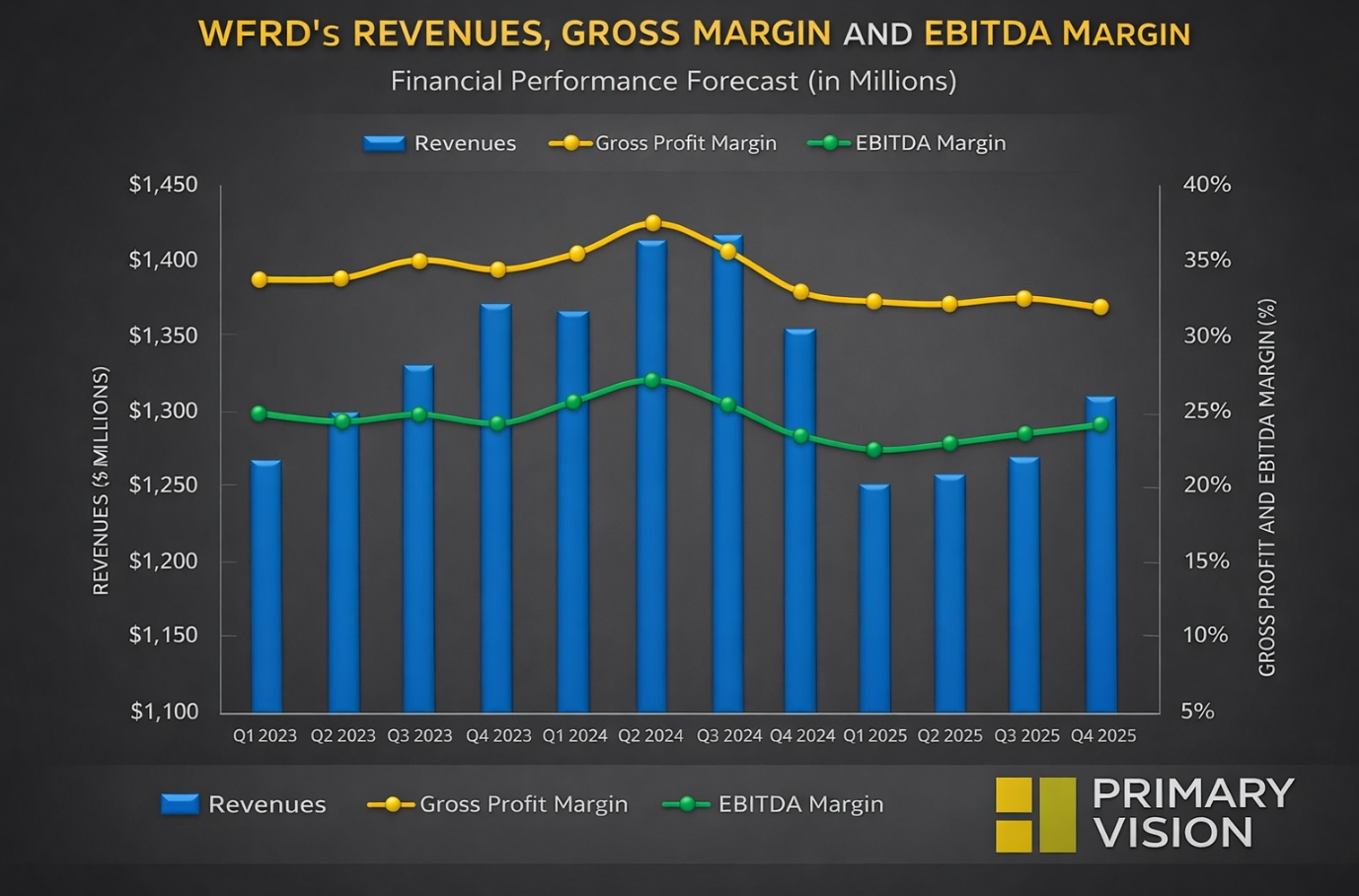

We discussed our initial thoughts about Weatherford International's (WFRD) Q4 2025 performance in our short article a few days ago. This article will dive deeper into its current outlook. WFRD’s WCC and PRI drove top-line growth, led by strong execution in completions and artificial lift. Completions has become the largest product line (42% of revenues), benefiting from low capital intensity, technology gains, and improved manufacturing scale. Artificial lift continues to benefit from a large installed base and the ability to scale North America expertise internationally. Recent wins in wireline, completions, and liner systems highlight progress in these product lines.

Its North America operation remains production-oriented, with artificial lift a key strength, even as rig- and well-count-driven product lines face pressure. The focus is on optimizing the footprint and driving innovation and digital differentiation to protect margins and generate higher-quality, higher-EBITDA revenue despite activity declines.

Short and Medium-term Outlook

WFRD expects customer spending to rise over the course of the year, though legacy pricing pressure will need to be managed with productivity and cost control in H1 2026. North America spending is expected to decline, with mid- to high single-digit activity reductions as operators maintain tight budgets. International activity should be weaker in the first half due to geopolitics and market volatility, then improve in the second half on contract awards and project start-ups.

As a result, WFRD expects 2026 international activity to be flat to slightly down, with the potential for year-on-year growth in the second half and improving offshore deepwater activity. Management remains constructive on 2027 and is taking steps to protect margins if markets move sideways. In FY2026, the company expects to see a marginal decline in revenues and adjusted EBITDA compared to FY2025. Free cash flow-to-EBITDA conversion can remain nearly unchanged at mid-40 percent.

Cost Cutting, Capex Plans, and Debt Restructuring

The company took an additional $7 million restructuring charge in Q4, bringing total 2025 charges to $58 million, as it rightsizes costs to align with activity and profitability. At the same time, productivity initiatives using shared services, digital tools, and AI are helping offset margin pressure from tariffs and divestitures.

WFRD’s FY2025 capEx was $226 million and its FY026 capEx is guided to $190–$230 million with a lower midpoint. The mix will shift, with lower spend on service tools and higher IT investment tied to ERP upgrades. The company also strengthened its balance sheet by reducing gross debt by $161 million and expanding its revolver to $1 billion. Net leverage has fallen to about 0.42x, supported by roughly $1.6 billion of total liquidity.

Relative Valuation

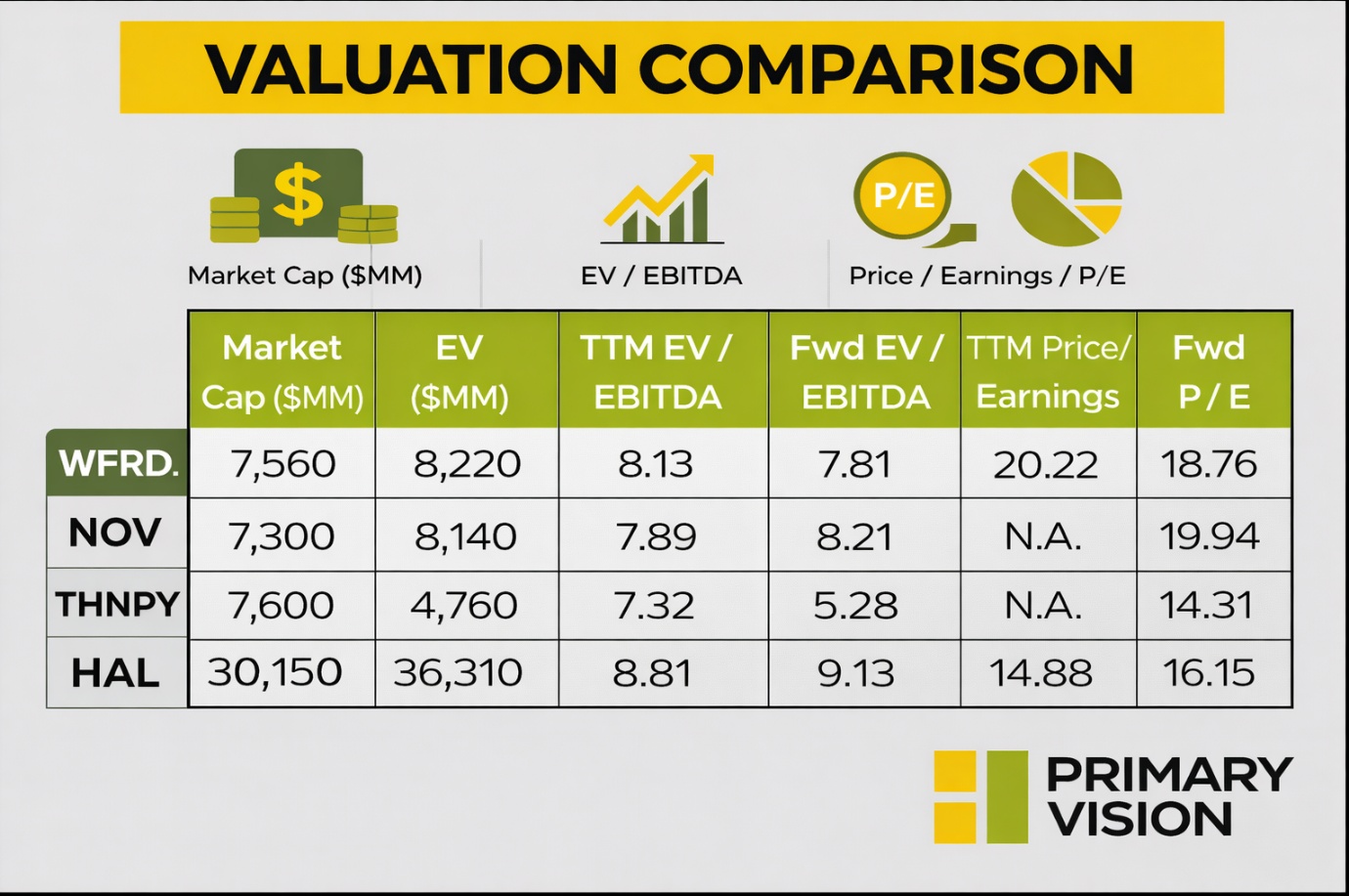

WFRD is currently trading at an EV/EBITDA multiple of 8.1x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 7.8x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 46x.

WFRD's forward EV/EBITDA multiple is expected to compress versus the current EV/EBITDA. This fall is less steep than its peers, as the company's EBITDA is expected to increase less sharply than its peers' EBITDA rise in the next year. This typically results in a lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is slightly higher than its peers' (NOV, THNPY, and HAL) average. So, the stock is overvalued compared to its peers.

Final Commentary

Completions and artificial lift are now the core growth engines for WFRD, supported by low capital intensity, technology gains, and international scale. North America remains production-oriented, where innovation and digital differentiation are being used to defend margins despite declining rig and well counts.

Near term, pricing pressure and softer activity weigh on revenues and EBITDA, but international momentum is expected to improve in the second half. Management is tightening costs, moderating capex, and shifting spend toward IT and efficiency to protect profitability. A stronger balance sheet and disciplined execution position WFRD to stabilize in 2026 and improve into 2027. The stock is relatively overvalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform