Articles

Free Read: Canada Emerges as an Important Oil Player

By Osama on January 28, 2026 in Free Articles

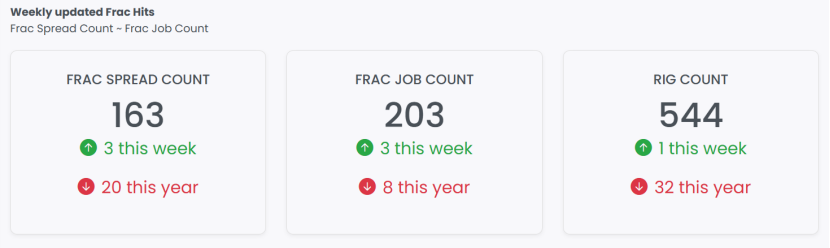

This week’s free read begins with the latest readings on U.S. shale activity. The most recent data show that operational momentum has improved modestly after a period of softening. Frac Spread Count increased by three units week over week and now stands at 160. While still below prior peaks, this level is only about twenty spreads lower than where the market stood at the same time last year. Frac Job Count also registered an uptick during the week, reinforcing the view that both service capacity and completion activity are gradually retracing higher. This pattern mirrors what was observed during the same phase last year, where short-term weakness was followed by a measured recovery rather than a structural contraction.

Source: Primary Vision

Against this backdrop, we recently published a special report expanding our Breakeven Series. The report builds on earlier work that disaggregates breakevens into multiple layers and then tests them against real operational behavior. It focuses on why price movements alone often fail to explain what actually happens on the ground. By examining how completion schedules, service capacity, and inventory depth interact, the report highlights the limits of using headline prices as a forecasting tool. Rather than offering a single threshold or static number, the analysis shows why shale activity often continues even when prices move sharply. The full report explores these dynamics in detail and explains why observed outcomes frequently diverge from simplified breakeven narratives.

Source: EFRACS, Primary Vision

Beyond U.S. shale, recent developments in Canada underscore a meaningful shift in global seaborne oil trade. Canada has emerged as a growing seaborne exporter, supported by structural changes in export infrastructure and destination markets. In 2025, Canadian seaborne crude oil exports surged to approximately 38.4 million tonnes, representing a year-on-year increase of more than sixty percent. As a result, Canada now accounts for roughly 1.7 percent of global seaborne crude oil loadings, placing it ahead of several traditional exporters that have historically played a larger role in waterborne markets.

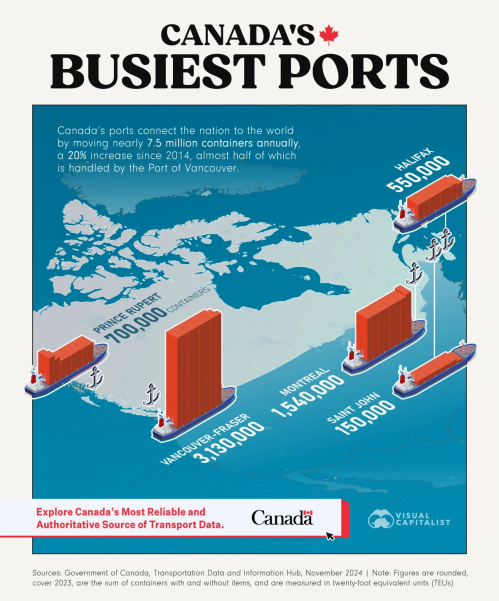

This growth is closely tied to expanded west coast export capacity. The Trans Mountain Expansion, operational since mid-2024, significantly increased crude export volumes from the port of Vancouver. In 2025, Vancouver accounted for nearly sixty percent of Canada’s seaborne crude loadings, followed by Whiffen Head and Point Tupper. Most of these barrels were carried on Aframax vessels, reflecting both port characteristics and the nature of Pacific Basin trade routes.

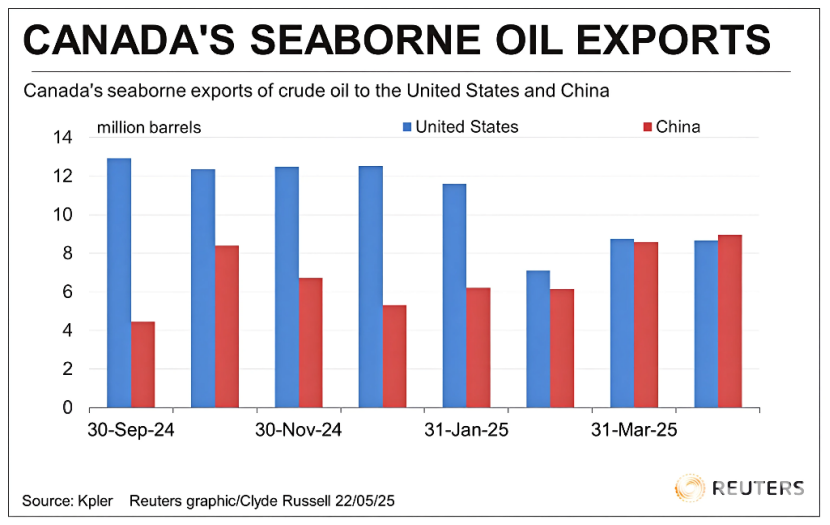

Destination data reveal a clear reorientation of Canadian crude flows toward Asia. While the United States remained the single largest destination for Canadian seaborne exports in 2025, accounting for about 45 percent of volumes, growth into the U.S. market was limited. Exports to the United States increased only modestly year over year, suggesting that incremental seaborne barrels are increasingly being directed elsewhere.

China has emerged as the most significant driver of this shift. Canadian crude exports to China surged sharply in 2025, rising to more than 12 million tonnes from minimal volumes just a year earlier. China now represents nearly one-third of Canada’s total seaborne crude exports. This increase reflects both China’s role as the world’s largest seaborne crude importer and Canada’s newfound ability to access Pacific markets at scale. The growth in shipments also aligns with broader trends in Asian demand, where import volumes into China and the wider ASEAN region remained resilient over the year.

Europe has also become a more meaningful destination for Canadian crude, albeit from a smaller base. Exports to the European Union rose sharply in percentage terms in 2025, while volumes to the United Kingdom and South Korea also increased. Although these flows remain modest in absolute terms, they underscore Canada’s transition from a predominantly pipeline-bound exporter to a more flexible participant in global seaborne trade.

Overall, Canada’s expanding role in seaborne oil markets reflects structural change. Infrastructure additions have altered export optionality, while destination data indicate a clear pivot toward Asia, particularly China. As global crude trade continues to adjust to shifting supply sources and demand centers, Canada is increasingly positioned as a marginal seaborne supplier. The implications of this shift will extend beyond trade flows, influencing tanker demand, regional pricing dynamics, and Canada’s strategic role within the global oil market.

Tags: