Articles

Free Read: Who's Absorbing the Glut? China, Sanctions, and the 2026 Oil Outlook

By Osama on February 25, 2026 in Free Articles

Our Frac Spread Count continues its recovery, posting a gain of 7 on a week-over-week basis. What stands out is the early-year momentum. Despite operating at significantly lower absolute levels—averaging 155 spreads in 2026 compared to 194 at the same point last year—the pace of activity growth has been notably stronger. From the first week to the seventh week, FSC increased by 2.6% in 2026 compared to just 1.0% in 2025, more than double the rate. Whether this reflects operators catching up after a slower holiday period, improved well economics, or a deliberate effort to front-load completions ahead of anticipated price softness remains an open question. For those interested in deeper analysis on job-level activity and basin-specific insights, feel free to reach out directly at osama@primaryvision.co or osama@pvmic.com.

Completion activity, of course, does not operate in isolation. Oil prices remain a key variable that will influence—though not solely determine—the trajectory of U.S. shale production in the months ahead. And with several moving pieces right now, it is worth taking a step back to unpack them.

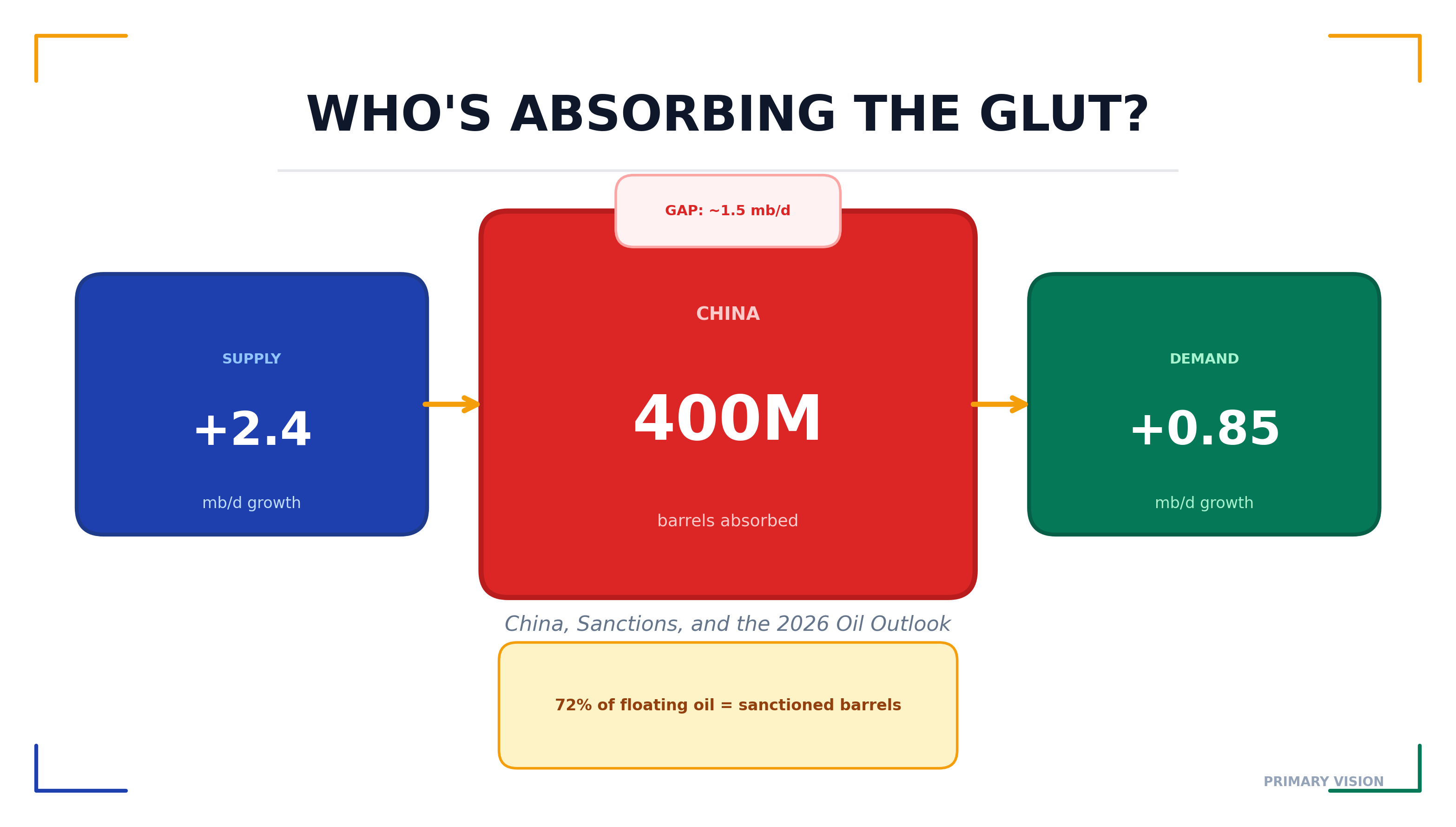

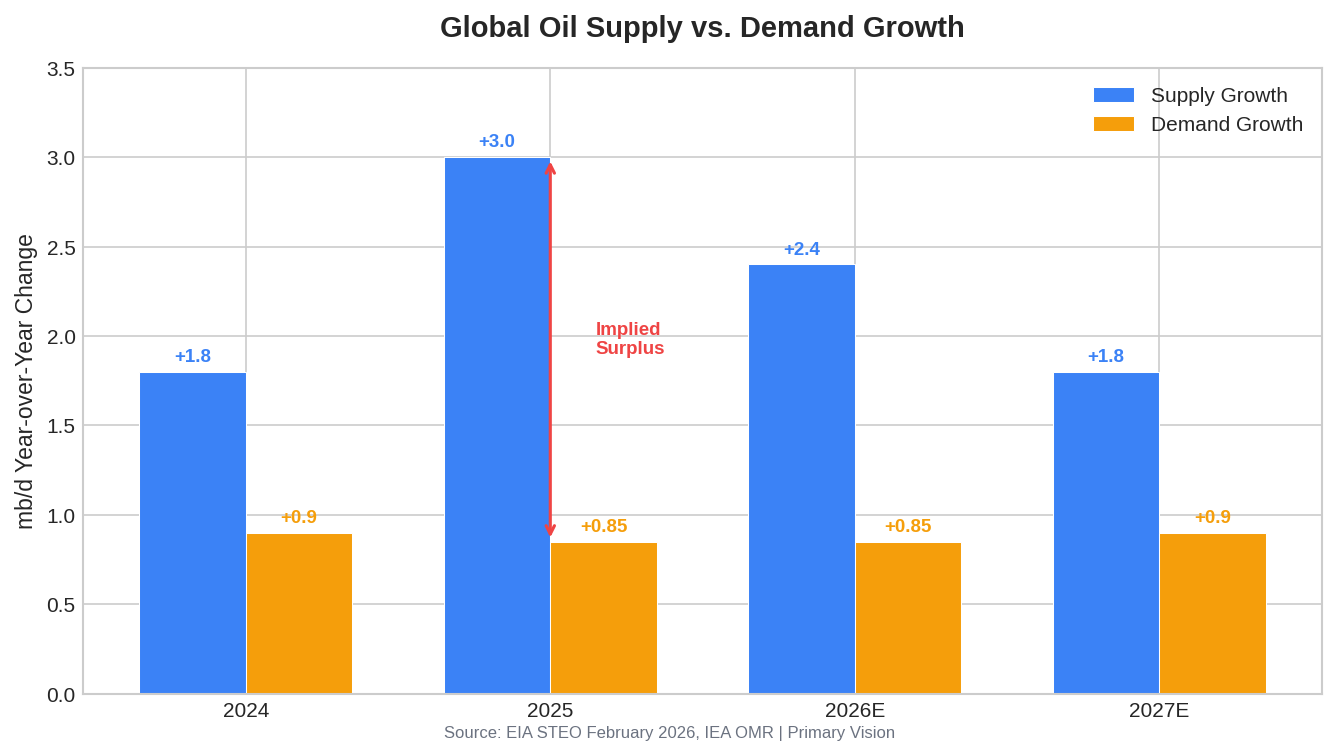

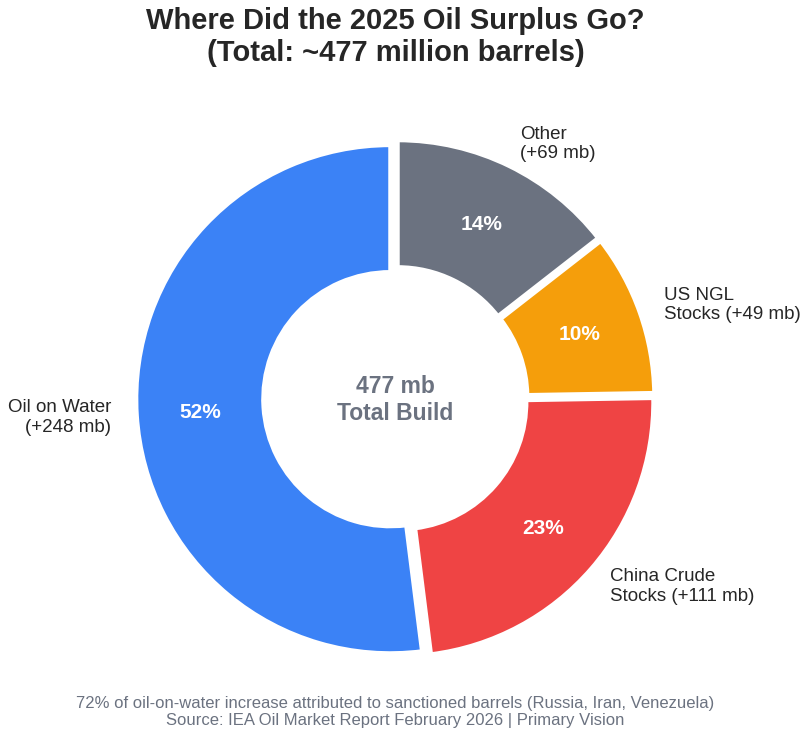

The headline narrative points toward oversupply. The EIA's February Short-Term Energy Outlook forecasts Brent averaging $58 per barrel in 2026, with global inventory builds of around 3.1 million barrels per day—more than in 2025. The IEA projects supply growth of 2.4 million barrels per day against demand growth of just 850,000. On paper, that is a significant imbalance. But the picture is more complicated than the headline numbers suggest. Saudi Aramco's CEO Amin Nasser recently dismissed the glut narrative as 'seriously exaggerated,' noting that global stocks remain below the five-year average and that much of the oil is sitting on water—roughly 1.3 billion barrels according to Kpler—consists largely of sanctioned barrels from Russia, Iran, and Venezuela that struggle to find buyers through conventional channels.

The IEA's own data shows that 72% of the increase in oil-on-water last year was attributable to sanctioned crude. These barrels are not truly 'surplus' in the traditional sense; they are stuck in logistical limbo, moving through dark fleet transfers and ship-to-ship operations that distort visibility into actual balances. Some analysts have argued that the glut forecasts are based on flawed assumptions, noting that EIA's own data show no major supply additions expected after late 2025. The reality is likely somewhere in between: supply growth is outpacing demand, but the 'untenable' 4 million barrel per day surplus some have projected may not materialize if sanctions continue to disrupt flows and China keeps absorbing excess barrels.

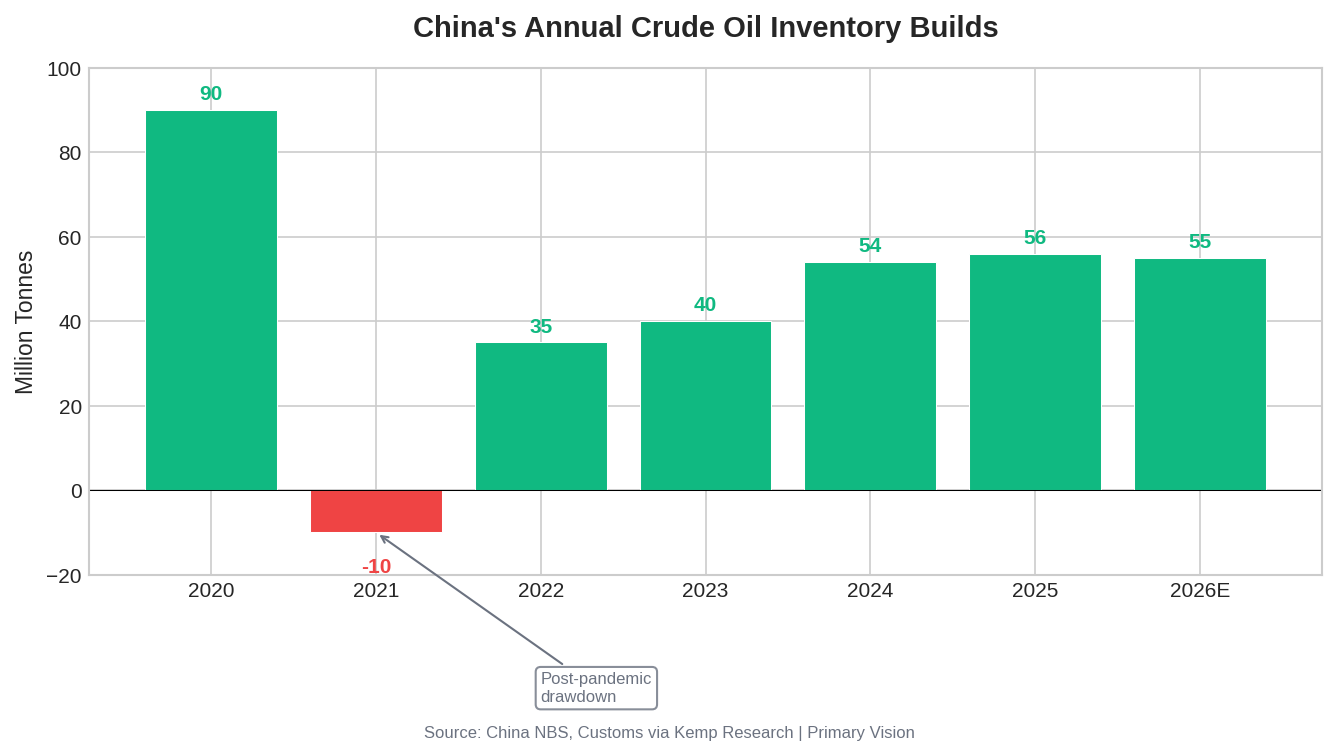

This is where China enters the picture. In 2025, China imported a record 11.6 million barrels per day of crude, up nearly 5% year-over-year. But here is the important detail: a significant portion of that increase went into storage rather than immediate consumption. According to analysis by John Kemp, China's crude inventories increased by around 54 million tonnes—roughly 400 million barrels, or about 1.1 million barrels per day—during 2025, following a similar build in 2024. The IEA estimates Chinese crude stocks rose by 111 million barrels over the course of last year. In effect, China acted as a substantial buffer, absorbing much of the global surplus that might have otherwise weighed more heavily on prices.

This is where China enters the picture. In 2025, China imported a record 11.6 million barrels per day of crude, up nearly 5% year-over-year. But here is the important detail: a significant portion of that increase went into storage rather than immediate consumption. According to analysis by John Kemp, China's crude inventories increased by around 54 million tonnes—roughly 400 million barrels, or about 1.1 million barrels per day—during 2025, following a similar build in 2024. The IEA estimates Chinese crude stocks rose by 111 million barrels over the course of last year. In effect, China acted as a substantial buffer, absorbing much of the global surplus that might have otherwise weighed more heavily on prices.

The EIA has described this stockpiling as a 'secondary source of oil demand'—a useful way to think about it. When barrels flow into strategic reserves rather than onto the open market, they effectively step out of the immediate supply-demand equation. The agency assumes China will continue building stockpiles at roughly 1.0 million barrels per day through 2026 before tapering in 2027. Chinese national oil companies have plans to add at least 169 million barrels of new storage capacity through 2026, and current facilities appear to be less than 60% full. There is room to continue.

That said, storage capacity has limits, and China's motivations extend beyond commercial considerations. The Communist Party's Central Committee recently issued a call for 'Building a Strong Energy Nation,' citing concerns about the 'politicization and weaponization of energy issues' and the need to enhance security capabilities. Inventory levels are treated as a state secret, which makes forecasting purchasing behavior inherently uncertain. If stockpiling were to slow—whether due to storage constraints, policy shifts, or the accelerating energy transition driven by electric vehicle adoption—that source of demand support would diminish. It is worth noting that China's NOCs have already moved up their peak oil demand projections, with CNPC now suggesting demand could peak as early as 2025 at 15.4 million barrels per day.

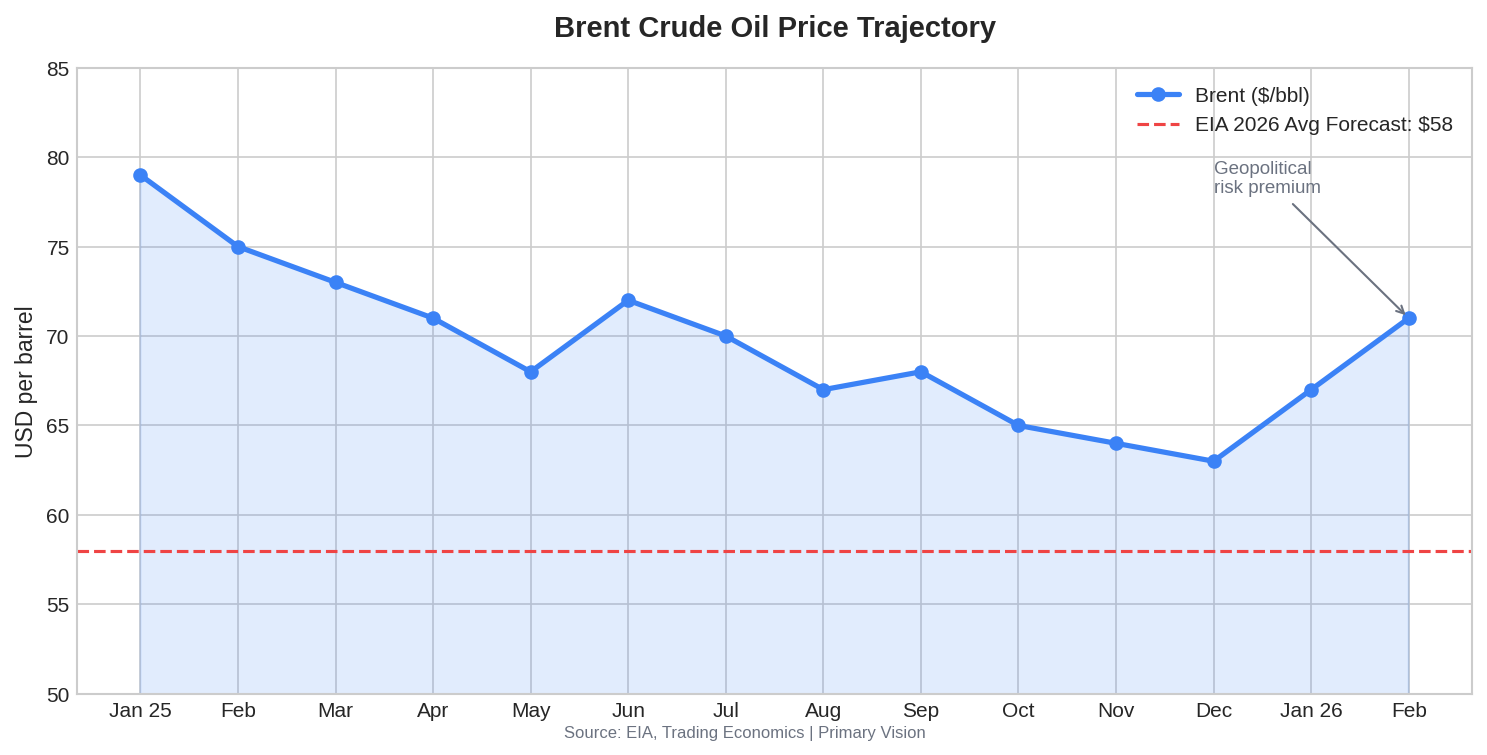

Then there is the geopolitical dimension, which has been adding a risk premium to prices in recent weeks. Brent has climbed to around $70-72 per barrel, up from the low-$60s, largely on U.S.-Iran tensions. Negotiations continue, but uncertainty remains. Beyond Iran, Ukrainian drone strikes on Russian refineries have contributed to what some analysts describe as the most significant fuel crisis in Russia since the 1990s, with the IEA expecting suppressed Russian refining capacity through mid-2026. Meanwhile, China has stepped in to purchase Russian crude that India is increasingly passing on under U.S. pressure—deliveries to Chinese ports rose to 2.09 million barrels per day in the first half of February, up from 1.39 million in December. These shifting flows matter because they reshape the global supply picture in ways that can be difficult to fully anticipate.

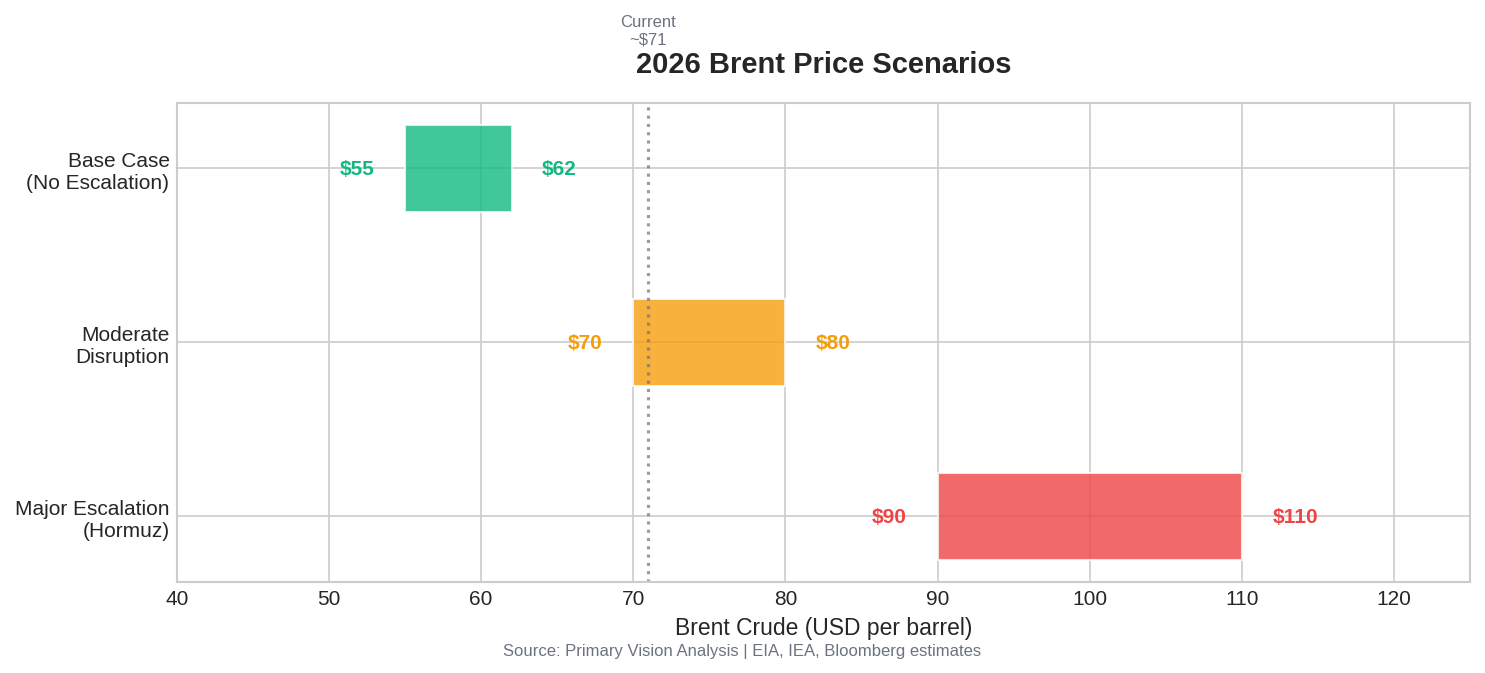

Thinking through scenarios, the range of potential outcomes is fairly wide. In a base case with no major escalation, continued oversupply, and China maintaining its stockpiling pace, Brent would likely settle in the $55-62 range through the year—broadly consistent with EIA projections. If sanctions tighten further or a supply disruption removes 1-2 million barrels per day from the market, prices could move into the $70-80 range, though strategic reserve releases might offset some of the impact. A major escalation involving the Strait of Hormuz—a scenario we have explored in previous articles—would be a different situation entirely, with prices potentially reaching $90-110 or higher. For U.S. shale operators, the environment remains challenging but workable. At $55-60 WTI, efficient operators in core acreage can still generate reasonable returns, though activity at the margins will feel more pressure. The stronger early-year momentum in completion activity may reflect an effort to capture current pricing before potential softness later in the year. China's stockpiling behavior—opaque as it is—could prove to be one of the more consequential variables for second-half pricing. It is certainly worth watching.

For U.S. shale operators, the environment remains challenging but workable. At $55-60 WTI, efficient operators in core acreage can still generate reasonable returns, though activity at the margins will feel more pressure. The stronger early-year momentum in completion activity may reflect an effort to capture current pricing before potential softness later in the year. China's stockpiling behavior—opaque as it is—could prove to be one of the more consequential variables for second-half pricing. It is certainly worth watching.

Tags: