Articles

Long Read: Is the Strait of Hormuz Losing its Importance?

By Osama on February 19, 2026 in Free Articles

.png)

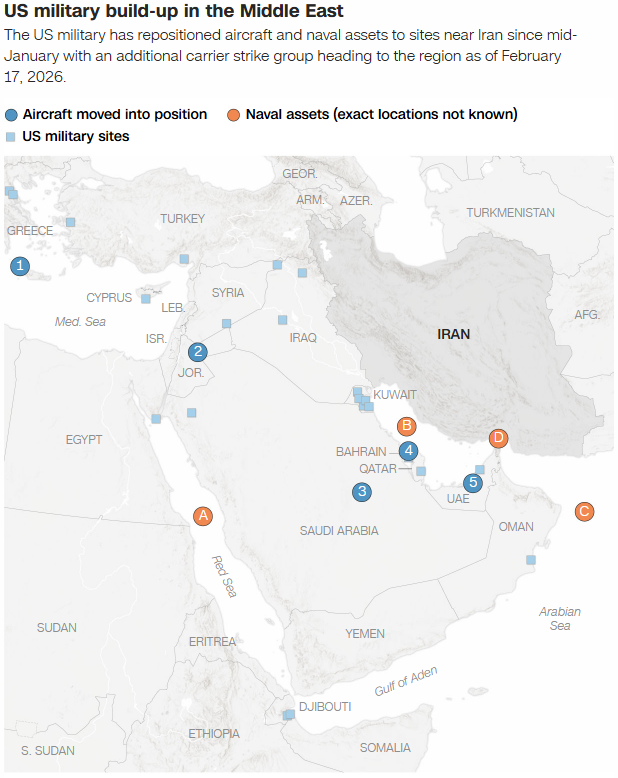

On February 17, as Iranian and American negotiators sat across from Omani mediators inside a residence in Geneva — conducting indirect nuclear talks for the second time in two weeks — Iran's Islamic Revolutionary Guard Corps simultaneously announced live-fire military drills in the Strait of Hormuz and a temporary partial closure of the waterway. The symbolism was unmistakable: diplomacy and coercion being deployed in parallel, from the same government, on the same afternoon.

The backdrop to these talks is a military buildup that has few recent parallels. According to CNN, open-source flight tracking data shows over 250 US cargo flights into the region in recent weeks, with C-17s and C-5s dropping equipment at bases across Jordan, Bahrain, and Saudi Arabia. Two carrier strike groups — the USS Abraham Lincoln, already positioned roughly 700km from the Iranian coast, and the USS Gerald Ford, en route — are now in or approaching the theater. Satellite imagery has confirmed F-15E Strike Eagles at Jordan's Muwaffaq Salti Air Base, refueling tankers repositioned from the UK, and near-constant drone surveillance over the Persian Gulf. Several military units that were scheduled to rotate out have had their orders extended. Officers, per multiple sources, are planning for "weeks-long operations." President Trump has been direct: "If they're not successful, it's going to be a very bad day for Iran."

So the talks continue, with a third round presumably coming, while both sides simultaneously signal military readiness. It is within this context that the question of the Strait of Hormuz becomes worth examining seriously — not as a rhetorical flashpoint, but as an actual instrument of economic leverage.

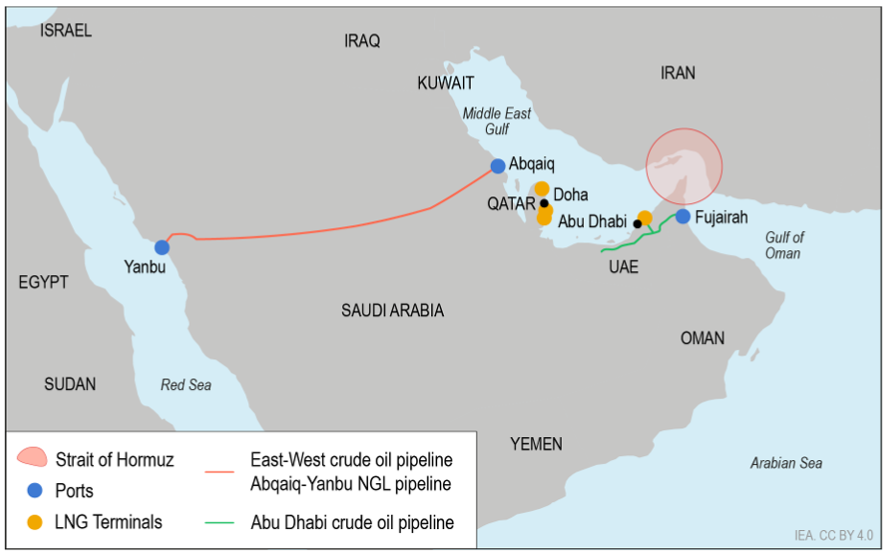

The Strait of Hormuz, at its narrowest roughly 29 nautical miles wide, is where the Persian Gulf meets the Gulf of Oman. Around 20 million barrels of oil per day — approximately 20% of global petroleum liquids consumption — transit it. Additionally, around 22% of global LNG trade flows through the strait, primarily from Qatar. Iran controls the northern bank. The IRGC's latest drills, named "Smart Control of the Strait of Hormuz," were explicitly designed to test readiness to regulate maritime traffic through the channel.

Iran has threatened to close the strait many times over several decades. It has never done so completely. The reason is partly practical: around 90% of Iran's own crude exports leave from Kharg Island, deep inside the Gulf, meaning any prolonged closure would be a significant act of self-harm. Secretary of State Marco Rubio put it plainly during the June 2025 tensions: "It's economic suicide for them if they do it." That remains true today.

But even a partial or temporary disruption carries real consequences. Alternative pipeline capacity around the strait is limited. Saudi Arabia's East-West Petroline has a capacity of around 5 million barrels per day, and the UAE's Habshan-Fujairah pipeline adds roughly 1.5 million bpd. Combined, that is perhaps 6.5 to 8 million barrels per day of bypass capacity against 20 million in daily flows — and only Saudi Arabia and the UAE have these alternatives. Iraq, Kuwait, Qatar, and Bahrain have no meaningful bypass routes at all. Analysts at the IEA put total available alternative pipeline capacity at 3.5 to 5.5 million barrels per day, a fraction of what transits the strait. Rerouting tankers around the Cape of Good Hope adds roughly two weeks of transit time, pushing up freight costs and insurance premiums — some of which have historically increased tenfold during periods of elevated conflict risk.

So the case for disruption being severe is real and well-documented. Any meaningful closure, even a short one, would likely send Brent crude significantly higher. That brings us to the structural question worth examining honestly: has the global oil market become more resilient to a Hormuz disruption than conventional wisdom suggests?

Several developments over the past few years point in that direction, though not uniformly.

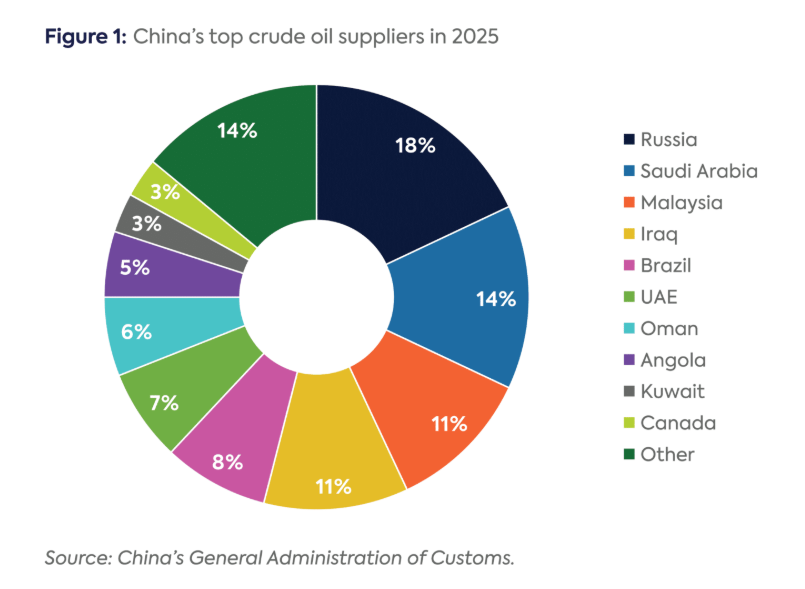

The most significant is China's inventory position. China is both the world's largest oil importer and the largest single buyer of crude transiting the Strait of Hormuz — Chinese, Indian, Japanese, and South Korean buyers together account for roughly 69% of all Hormuz crude flows. China's response to the disruption potential is not to protest it but to prepare for it. Between January and August 2025, according to the US Energy Information Administration, China added roughly 900,000 barrels per day to its oil inventories — functioning essentially as a massive off-market demand absorber. By December 2025, Kpler monitoring estimated China's total strategic and commercial reserves had exceeded 1.5 billion barrels, representing approximately 121 days of import coverage. A Columbia University SIPA analysis published in 2026 concluded that China's oil stockpiles should enable it to "weather any multi-month interruption of its imports."

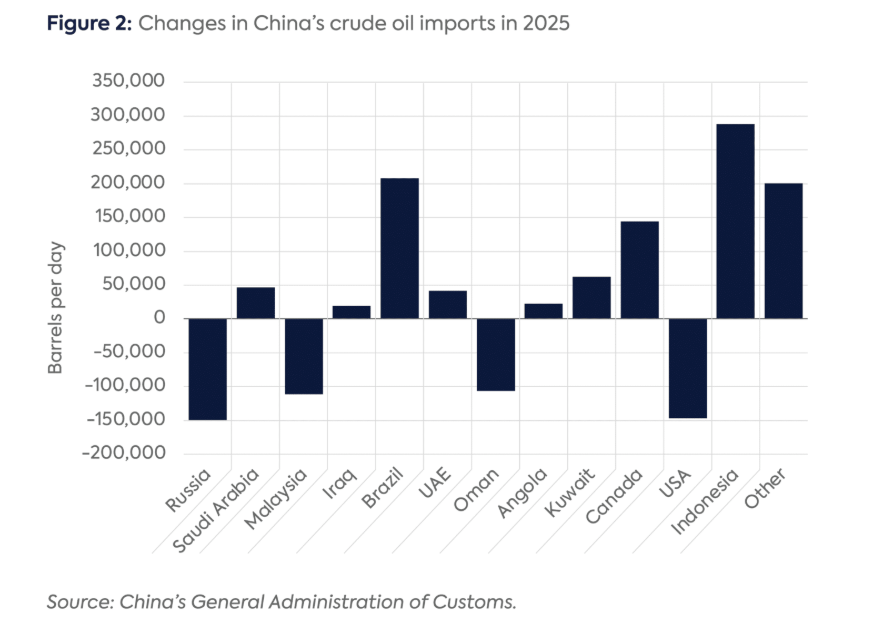

Beyond inventory, China has meaningfully diversified its supply origins. Brazil has emerged as a major supplier: China now absorbs roughly 40% of Brazil's total crude exports, with imports from Brazil rising 60% year-on-year in Q2 2025 alone. Canadian imports have also surged to record levels in 2025 as trade tensions pushed China toward Western Hemisphere alternatives. Neither Brazil nor Canada require transit through the strait. This supply diversification is not incidental — it reflects a deliberate Chinese energy security strategy formalized in a new Energy Law enacted in January 2025.

Meanwhile, the United States has changed its own position in global oil markets fundamentally. The EIA's Short-Term Energy Outlook confirmed US crude production averaged a record 13.6 million barrels per day in 2025 — the highest in the country's history. US imports from Persian Gulf countries through the strait amount to roughly 0.5 million barrels per day, or about 2% of domestic petroleum consumption. The direct supply exposure of the US to a Hormuz disruption is, at this point, quite limited. Rubio's comment about economic suicide for Iran was not idle bluster — it reflected a genuine asymmetry in vulnerability that has widened considerably over the past decade.

There is also a global supply overhang dynamic that contextualizes any price shock. And yet, the counterargument deserves equal space.

The 1.5 billion barrels China holds in reserves covers it. Japan, South Korea, and India — which together account for a significant share of remaining Hormuz crude flows — are not similarly positioned. India in particular has been expanding its refining capacity to process Gulf heavy crude, and its alternatives are more limited. A prolonged closure would not hit all consumers equally. The countries most exposed are precisely those with the least flexibility.

More fundamentally, the physical infrastructure gap remains. If 20 million barrels per day normally transit the strait and bypass capacity peaks at perhaps 8 million, there is simply no mechanism to route the balance elsewhere quickly. At 20 million barrels per day of lost flow, combined global strategic reserves across the US, Europe, and Asia would be drawn down within roughly two months. The question then becomes whether a disruption would last that long — and historically, the political and economic pressure to resolve such a crisis has been overwhelming.

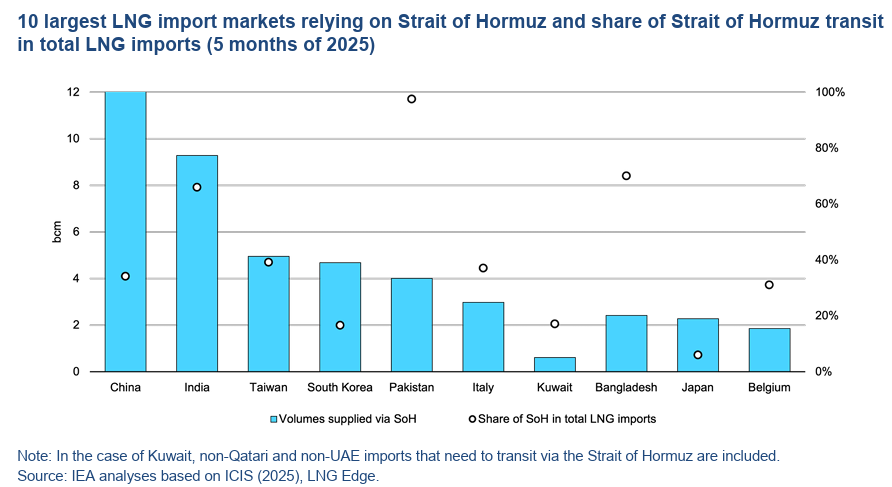

The LNG dimension is often underappreciated in this debate. Qatar ships approximately 20% of global LNG supply through the strait. Unlike crude oil, LNG cannot simply be rerouted — it requires specialized terminals and long-term contracts. A disruption to Qatari LNG flows would hit European and Asian gas markets in ways that have no short-term buffer equivalent to crude oil reserves.

Source: IEA, Straits of Hormuz, Fact Sheet

What seems fair to conclude is that the Strait of Hormuz retains genuine strategic leverage, but that the specific magnitude of a disruption's impact has become more nuanced and unevenly distributed than the headline figure of "20% of global oil" implies. The largest single consumer exposed to a disruption — China — has spent the past two years building the most substantial insurance against it. The largest producer in the world — the United States — is now largely insulated from the direct supply side of the equation. The most vulnerable parties are mid-sized Asian importers and European LNG buyers.

The sentiments markets would react immediately and sharply. The physical fundamentals would begin to diverge from that sentiment within weeks, as the depth of available reserves, diversified supply flows, and spare production capacity outside the Gulf get priced in. How wide that gap between sentiment and fundamentals would be — and how long it would persist — is genuinely uncertain, and probably the central question for energy markets if this crisis deepens.

For now, both sides appear to prefer the threat of disruption to the disruption itself. That calculus could change. But as of today, the Iran-US crisis is still at the stage where the waterway's symbolic power considerably exceeds its operational one.

Tags: