Articles

Market Sentiment Tracker: China met its GDP target. What comes next?

By Osama on January 27, 2026 in Latest News

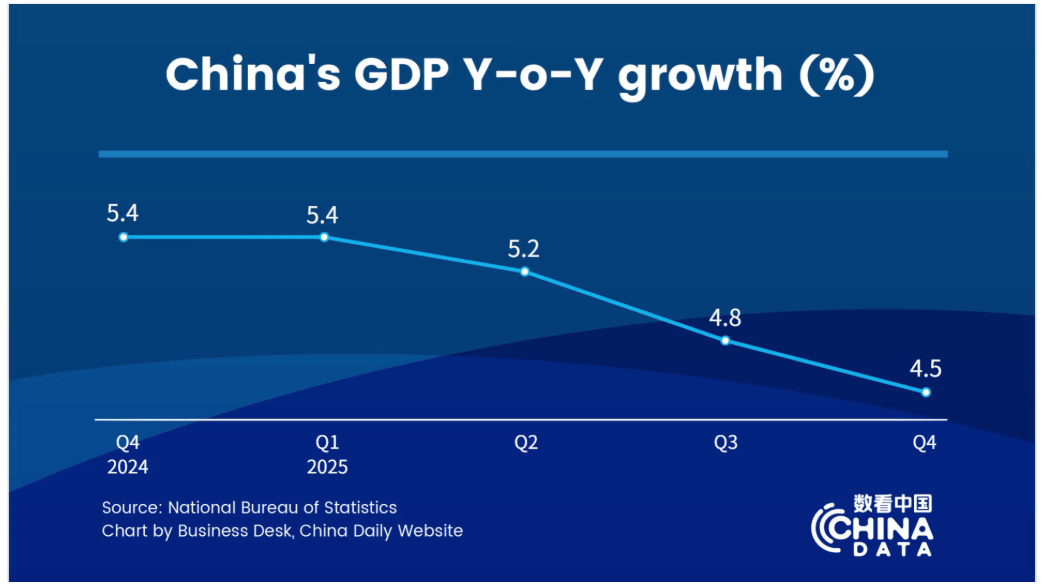

China’s latest national accounts were released against a backdrop of heightened scrutiny, as the economy once again delivered growth in line with official objectives. Full-year GDP expanded by 5.0 percent year on year, while fourth-quarter growth moderated to 4.5 percent. In this article we are going to evaluate the source of these indicators of growth and how it is currently being generated and where pressure is being absorbed.

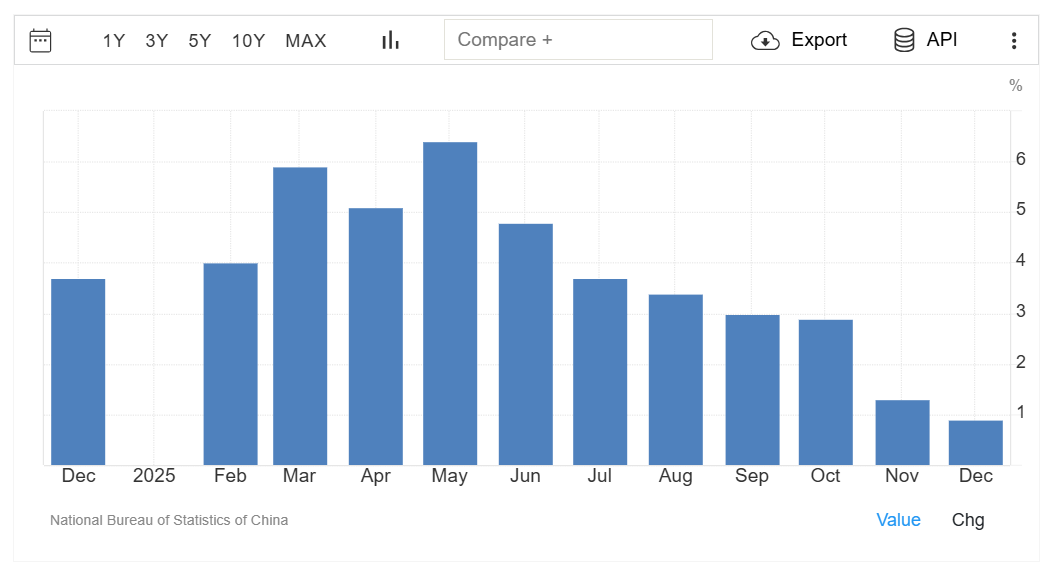

The central fact of the data is that China’s growth is being carried by production and external demand rather than domestic consumption. Industrial output strengthened into year-end, with factory production rising 5.2 percent year on year in December, up from 4.8 percent previously. This acceleration is consistent with the trade numbers. The annual trade surplus reached approximately $1.2 trillion, the largest on record, reflecting continued export strength across machinery, electronics, vehicles, and intermediate goods. This is not marginal activity. It is large-scale, systemically relevant output that anchors GDP mechanically.

%20(1)_qKXXWaz.png)

Energy and commodity flows confirm this industrial footing. Crude oil imports remained elevated through the year, and refinery throughput stayed near recent highs. These indicators track physical operating intensity as compared to the sentiment. They imply that manufacturing plants, logistics networks, and transport systems are running at volumes that if not corroborate this growth claim then also don't support news of generalized slowdown. In an economy of China’s size, sustained energy demand is a more reliable signal of real activity than short-term fluctuations in consumer spending.

By contrast, domestic demand remains weak. Retail sales growth slowed to 0.9 percent year on year toward the end of the year, and household-facing services have yet to regain momentum. This softness is neither hidden nor accidental. It reflects subdued income expectations and a deliberate refusal to reignite consumption through aggressive credit expansion or asset reflation.

Property investment contracted by roughly 17 percent year on year, and new home prices declined about 2.7 percent. These are large declines, and they persist. What matters is not that property is weak, but that it remains weak without triggering broader instability. That outcome indicates that the economy’s growth engine is no longer structurally reliant on housing turnover, land sales, or speculative household leverage. But nonetheless, this is something that warrants a continuous attention.

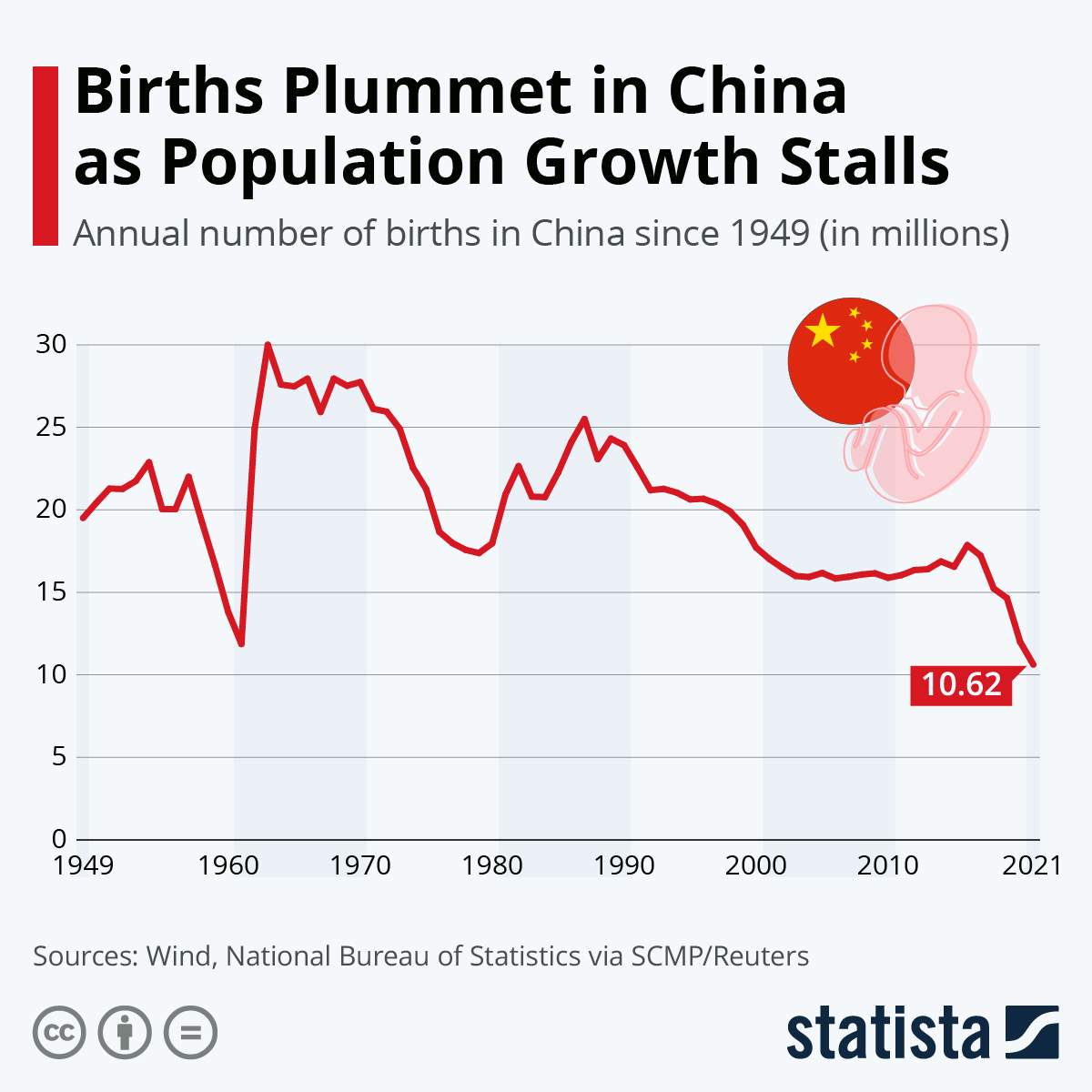

Demographic indicators are also worrisome in regards to prospects of long term growth. Births fell below eight million, and the population declined for a fourth consecutive year. These trends cap the medium-term contribution of consumption growth and make labor-intensive expansion less viable. In response, the economy is leaning into capital intensity, scale, and export competitiveness. The industrial and trade data show this adjustment is already functioning in practice.

Concerns about headline GDP credibility miss the larger point. Even allowing for measurement noise, the direction and composition of activity are confirmed across independent datasets. Output growth, export volumes, energy imports, and industrial production all align. Consumption and property remain weak.

China’s current economic position is therefore not ambiguous. Growth is concentrated, and industrially grounded. The economy is producing more than it is distributing, prioritizing capacity and competitiveness over near-term household comfort. That choice carries social and political trade-offs, but economically it is coherent.

Tags: