Articles

- BLOG / Articles / View

- Articles

Enterprise Subscribers|Monday Macro View: Decoding the Dallas Fed Survey using our Data

By Osama on March 30, 2026 in Market Sentiment

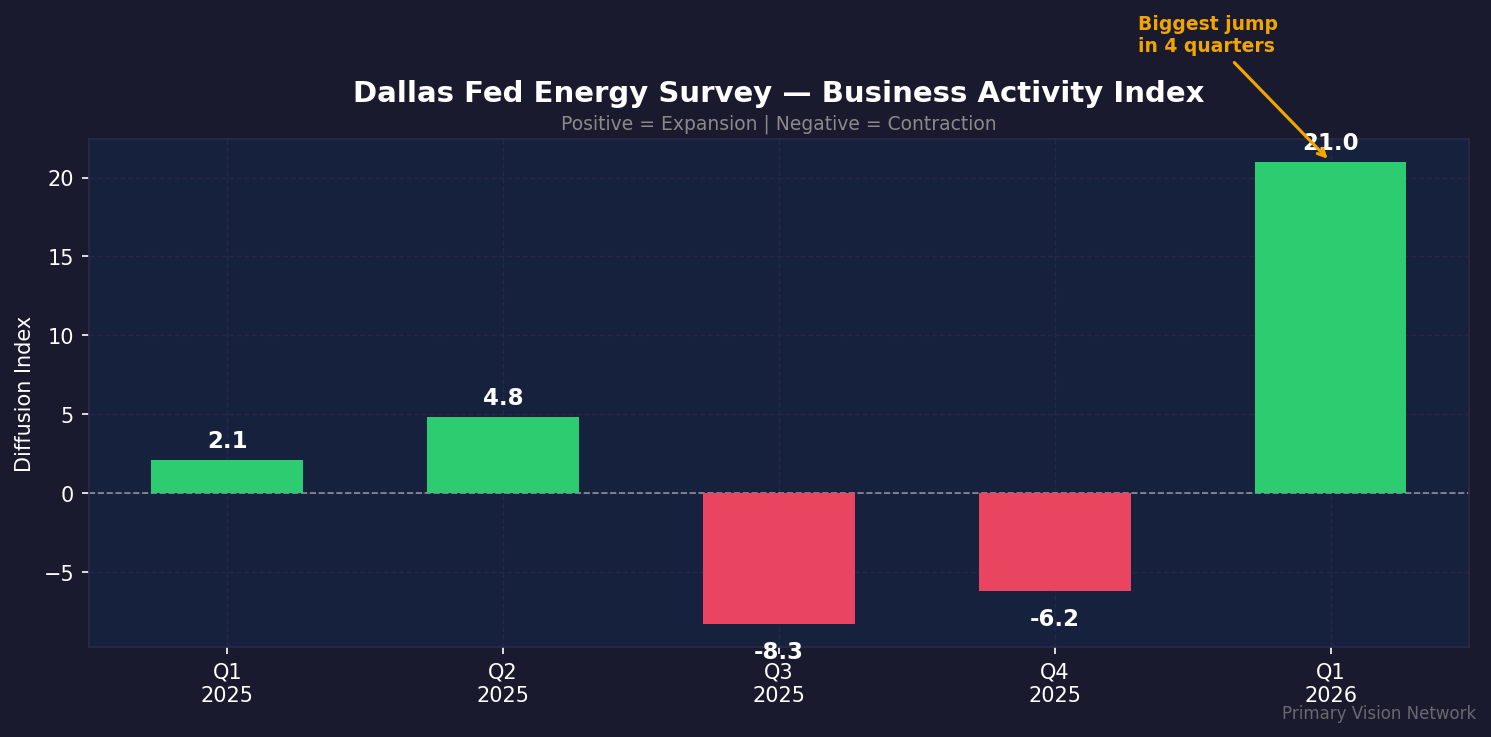

The Q1 2026 Dallas Fed Energy Survey arrived last week with a message that will surprise no one who has been following Primary Vision's completion data closely. The business activity index swung from -6.2 to +21.0, company outlooks flipped from -15.2 to +32.2, and oilfield services equipment utilization jumped from -12.2 to +30.2. For anyone tracking frac spreads and frac job counts through Q1, none of this is shocking. The recovery that Primary Vision's data has been signaling for weeks is now showing up in executive sentiment as well and that alignment between ground-level activity data and boardroom confidence is itself an important signal.

Note: The latest FSC came in at 159, a drop of 5 while FJC registered a similar decline now standing at 204.

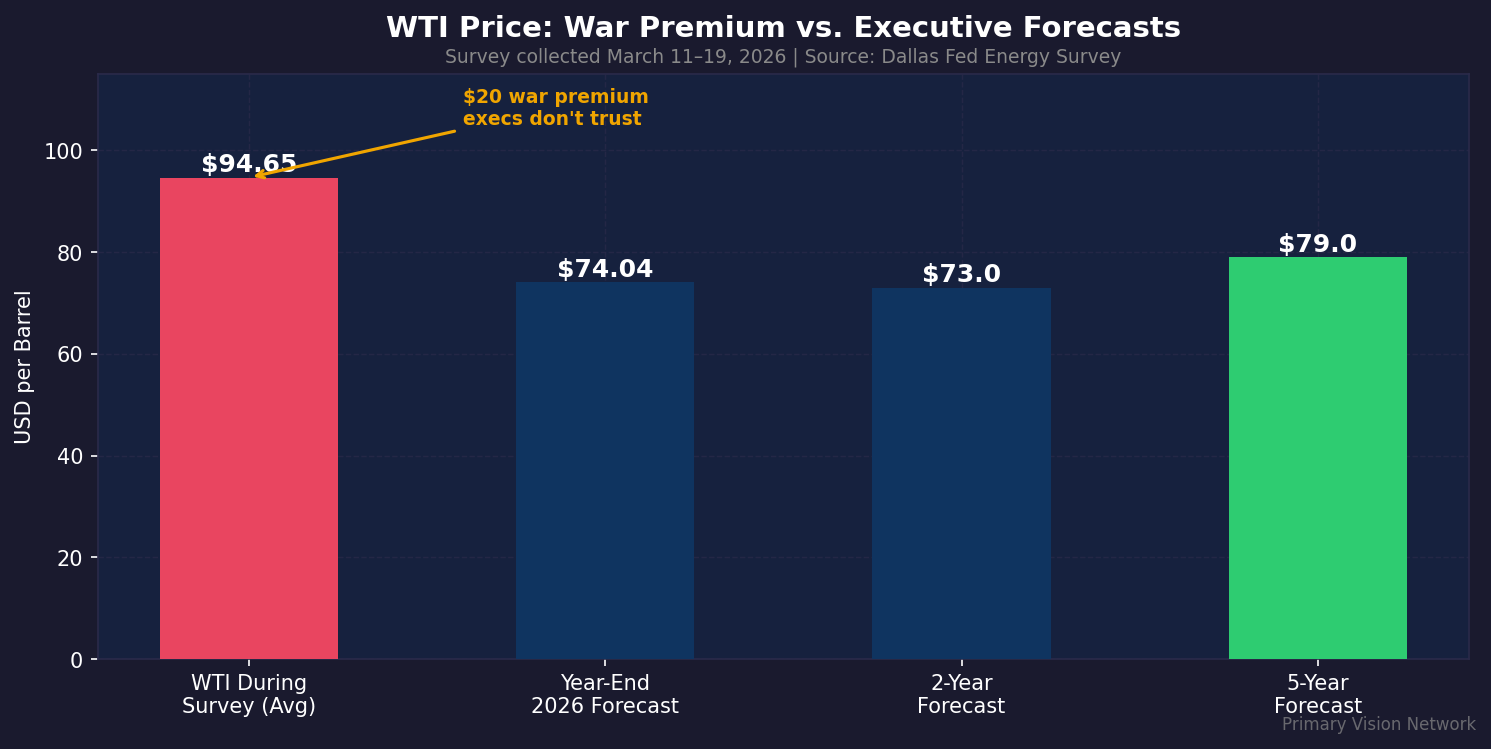

The macro backdrop driving all of this is impossible to ignore. WTI averaged $94.65 per barrel during the survey collection window of March 11-19, elevated by the Iran conflict and ongoing Strait of Hormuz disruptions. That price environment injected genuine energy into operator planning conversations. But what makes this moment interesting is the discipline accompanying it. Survey respondents expect WTI at $74 by year-end on average, meaning they are treating a meaningful portion of the current price as a geopolitical premium rather than a new structural floor.

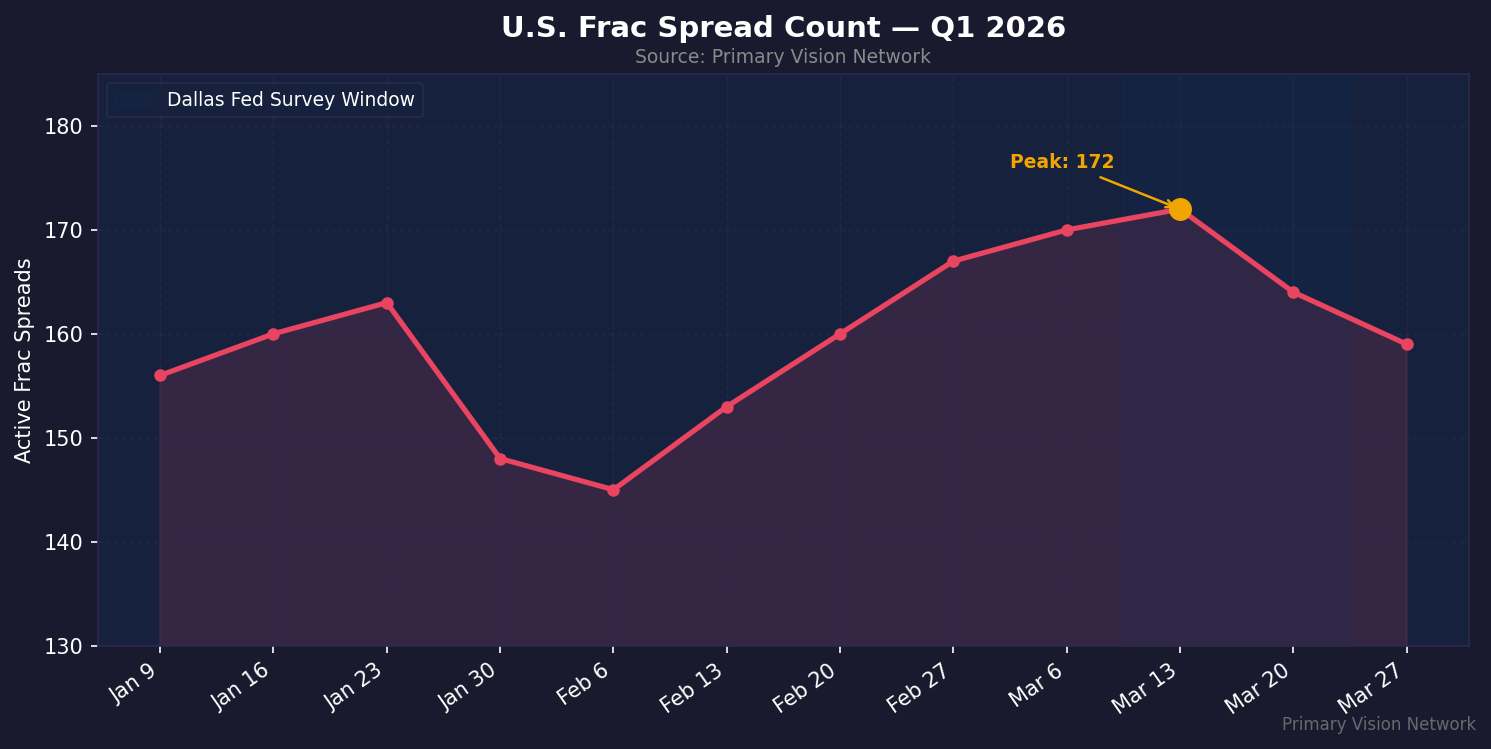

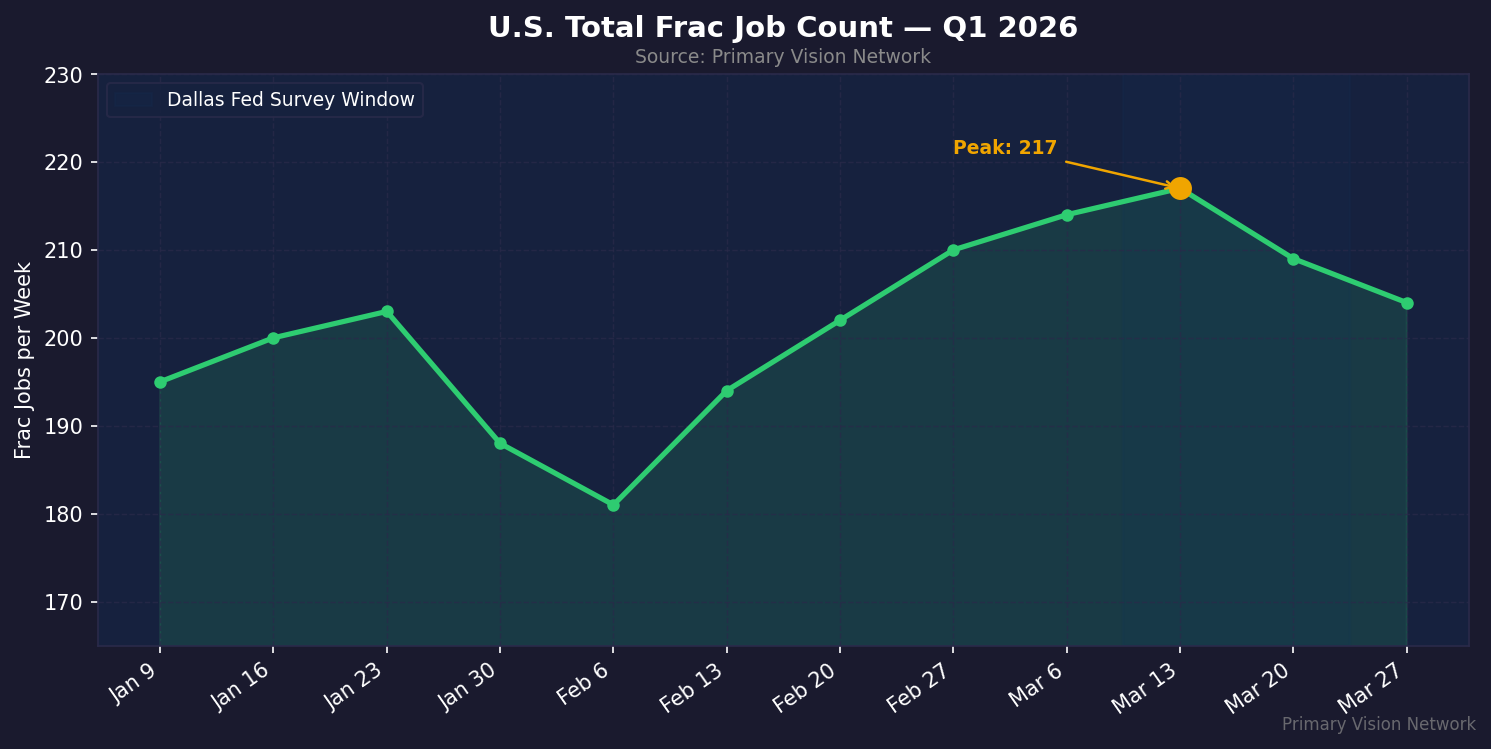

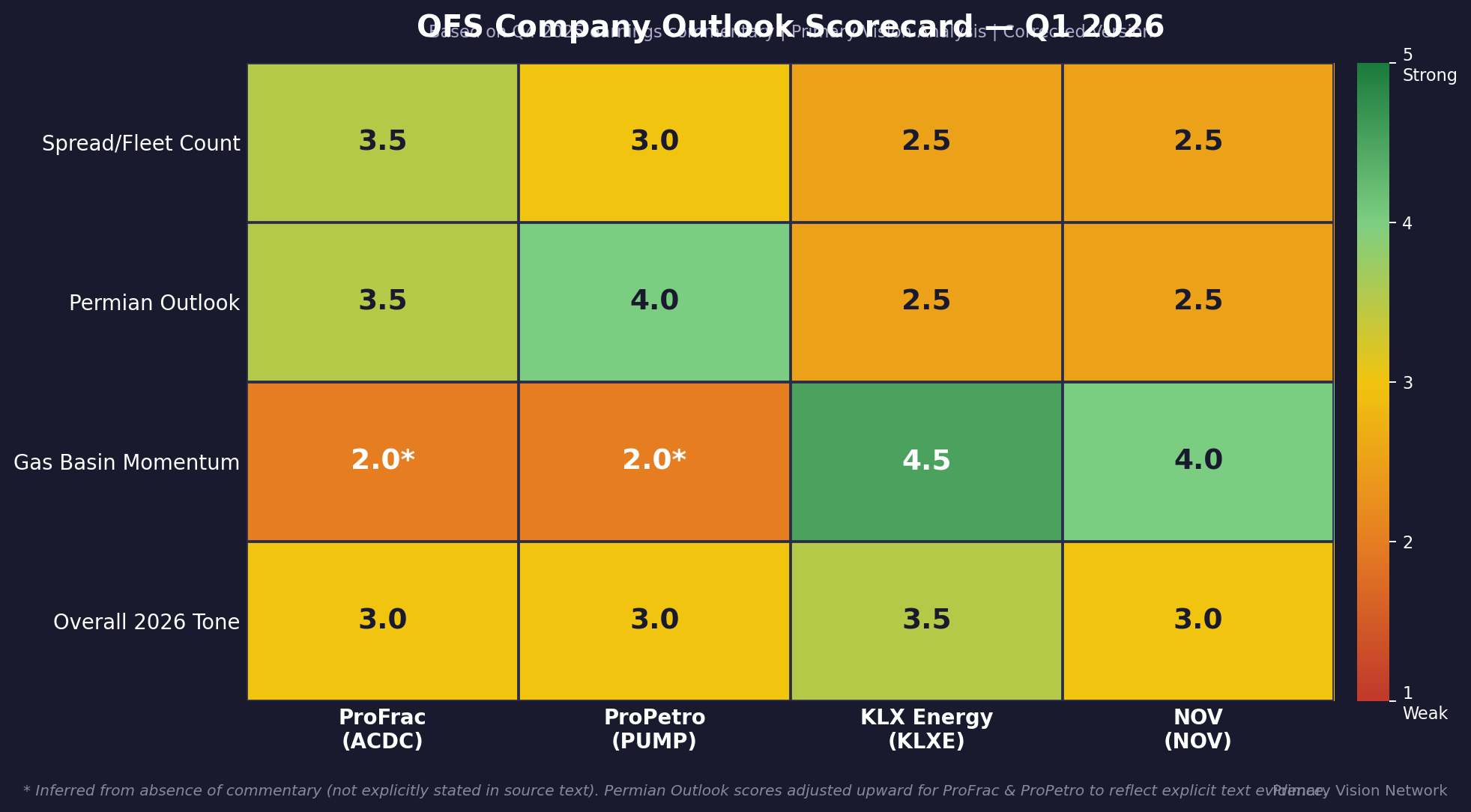

Primary Vision's data shows that the physical recovery was already well underway before the survey was even published. Total frac spread count climbed from around 145 in early February to 172 by the first week of March — a gain of nearly 20% in under six weeks. Frac job count followed the same trajectory, building steadily from 195 in early January to a Q1 peak of 217 by mid-March. The sector reactivated through the quarter, with completion calendars tightening and operators pulling forward DUC completions in response to a constructive price environment. ProFrac's management confirmed this directly, noting that utilization and operational efficiency both improved through Q4 with pricing holding stable. ProPetro similarly reported contracted fleets and disciplined deployment rather than idle capacity sitting on the sidelines.

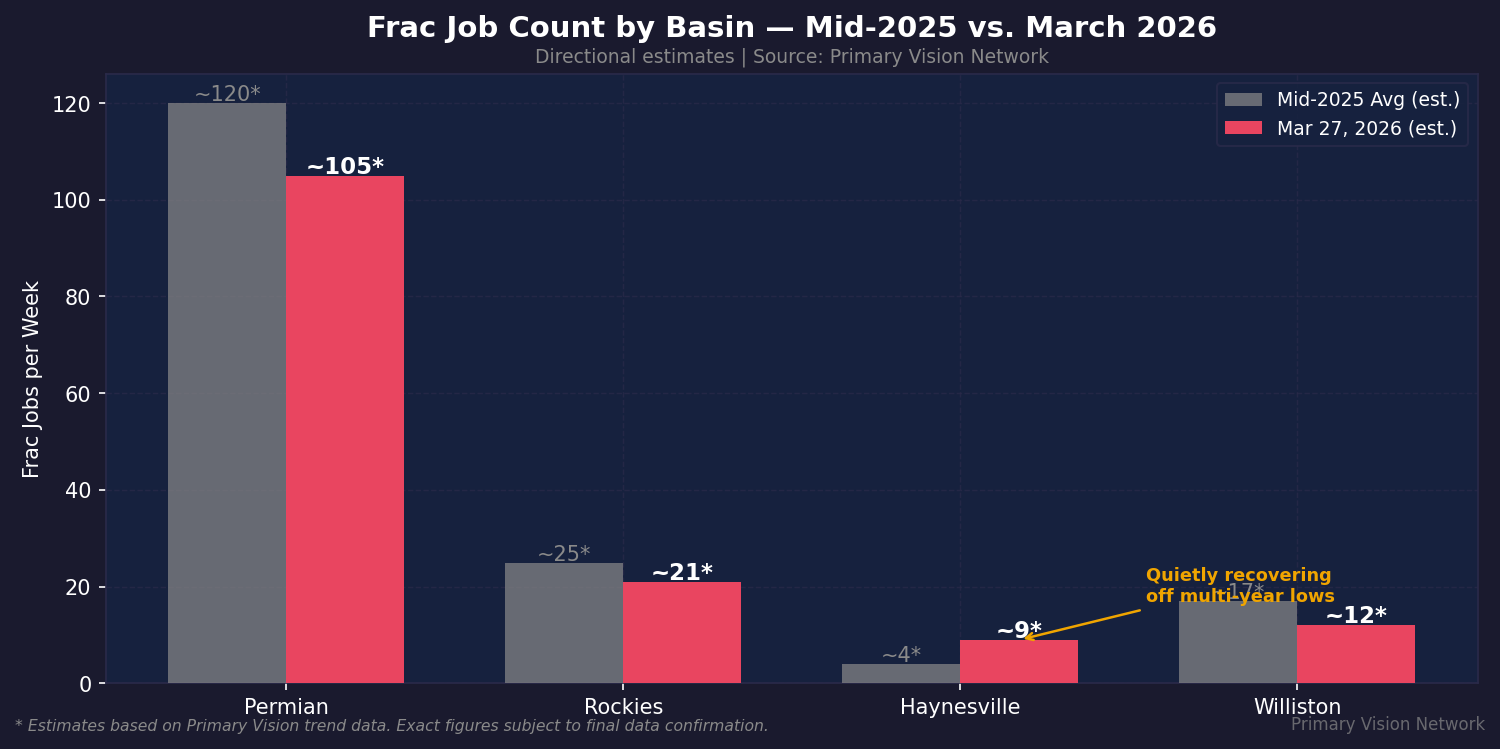

The basin-level picture is where Primary Vision's data adds the most texture to the Dallas Fed narrative. The survey's most striking finding was that 82% of respondents expect the Permian Basin to drive U.S. oil production growth from December 2025 to December 2026 and the frac data supports the Permian's continued dominance as the backbone of domestic completions activity. The basin is running a steady 100-110 frac jobs per week, holding its position as the single largest contributor to the national FJC total by a wide margin. ProPetro's Permian-focused fleet strategy and PUMP's ongoing investment in Tier IV DGB refurbishments and automation upgrades reflect an operator base that is optimizing and strengthening its Permian position for the cycle ahead rather than pulling back from it.

Perhaps the most underappreciated story in both the survey data and Primary Vision's basin-level trends is what is happening in gas. The Dallas Fed survey, shaped heavily by the oil price shock psychology of the survey period, gave relatively little attention to gas-directed activity. But Primary Vision's data shows Haynesville frac job count recovering meaningfully from the multi-year lows of late 2025, with the basin trending back toward 8-9 jobs per week and showing clear directional momentum. This aligns precisely with what KLX Energy Services reported — gas-directed basins were the standout performers in Q1, with dry gas revenue rising both sequentially and year-over-year in the Northeast Mid-Con. NOV similarly flagged stronger gas basins as a meaningful offset to softer oil-directed markets. With LNG export demand growing, data center power consumption rising, and natural gas fundamentals quietly strengthening, Haynesville's recovery deserves more attention than it is currently receiving in the broader industry conversation.

The Rockies are contributing steady, reliable volume at 20-22 jobs per week not accelerating dramatically but providing consistent baseline activity that supports the national count.

What the Dallas Fed survey and Primary Vision's data are together confirming is that 2026 is shaping up as a year of disciplined, broadening recovery. The Permian holds its ground as the dominant basin. Gas is emerging as a genuine second growth engine. Operators are running tighter completion schedules, OFS companies are seeing utilization improve, and the cost discipline built through a difficult 2025 is carrying forward into a more constructive environment. The executives surveyed by the Dallas Fed are feeling better because the underlying activity data justifies feeling better. Primary Vision's data was there first and the survey just caught up.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform