Market Sentiment Tracker: One Strait, Every Wallet

By

Osama

on March 11, 2026

in

Market Sentiment

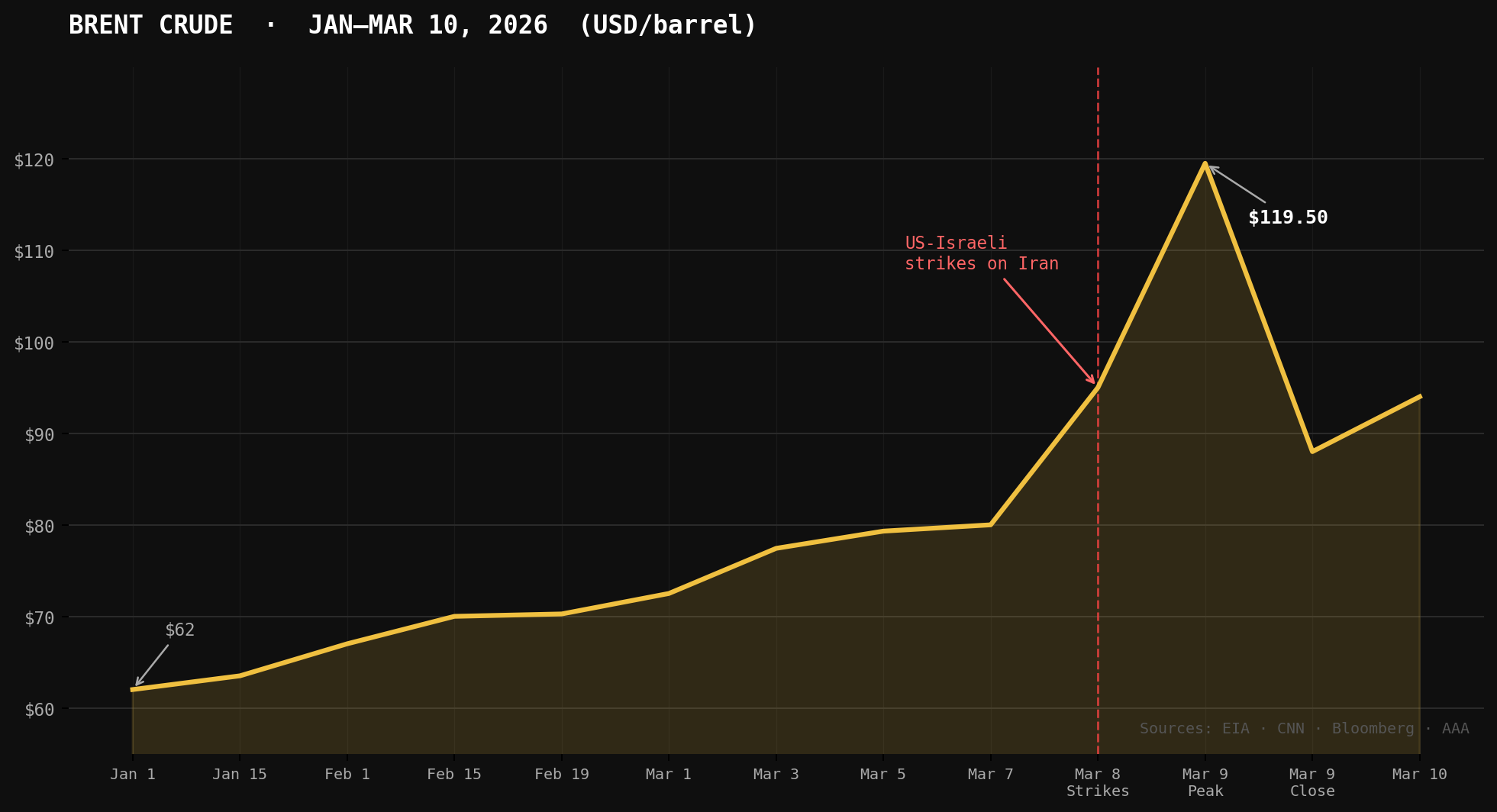

On February 28, 2026, the United States and Israel launched coordinated strikes on Iran under Operation Epic Fury, killing its supreme leader and triggering a chain of events that every household on earth will eventually pay for. Iran didn't need a naval blockade to shut down the Strait of Hormuz — a handful of drone strikes near the waterway was enough, and insurers did the rest. The strait moves roughly a fifth of the world's traded oil and significant LNG volumes every single day. When it goes dark, the cost lands everywhere.

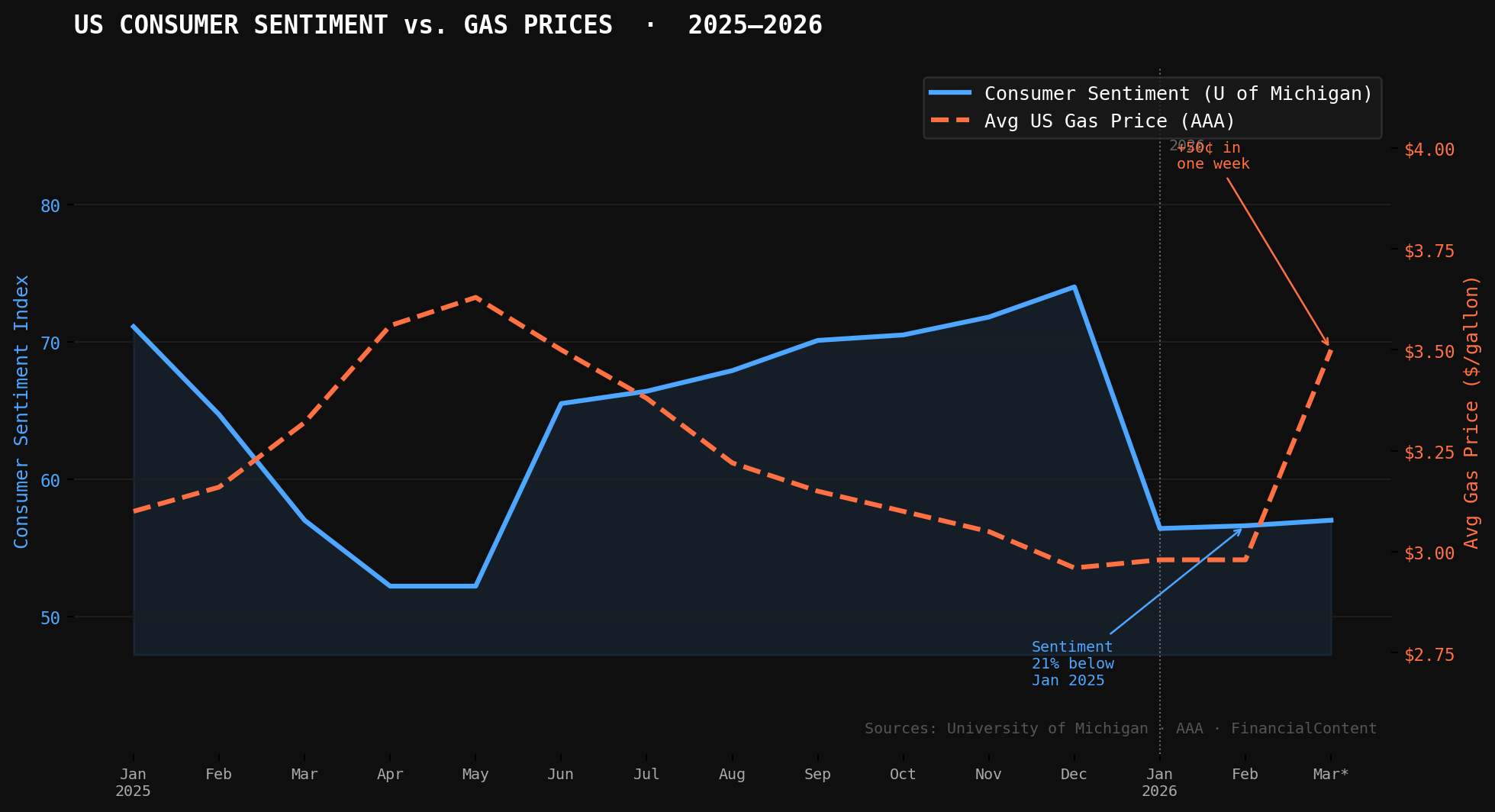

Brent crude had been drifting upward through the first quarter — $62 in early January, $80 by late February — a market quietly pricing in the possibility of war. Then on March 9, Brent peaked near $119.50 and US gasoline jumped 10% in a single week. It hit at the worst possible moment. The University of Michigan sentiment index was already down to 56.6 in February — roughly 20% below where it sat in January 2025 — and about half of working households were already expecting their income to flatline this year. The energy shock didn't find a resilient consumer. It found an exhausted one.

Payrolls had added just 130,000 jobs in January, unemployment was holding at 4.3%, and the personal savings rate had already slipped to 3.6% in December — its lowest since 2022. People were spending more than they were making. Then private employers cut 86,000 jobs in February. A 90% oil price surge doesn't land softly on top of that. The K-shaped dynamic — where asset owners hold steady while everyone else pulls back — doesn't gradually widen in this environment. It snaps.

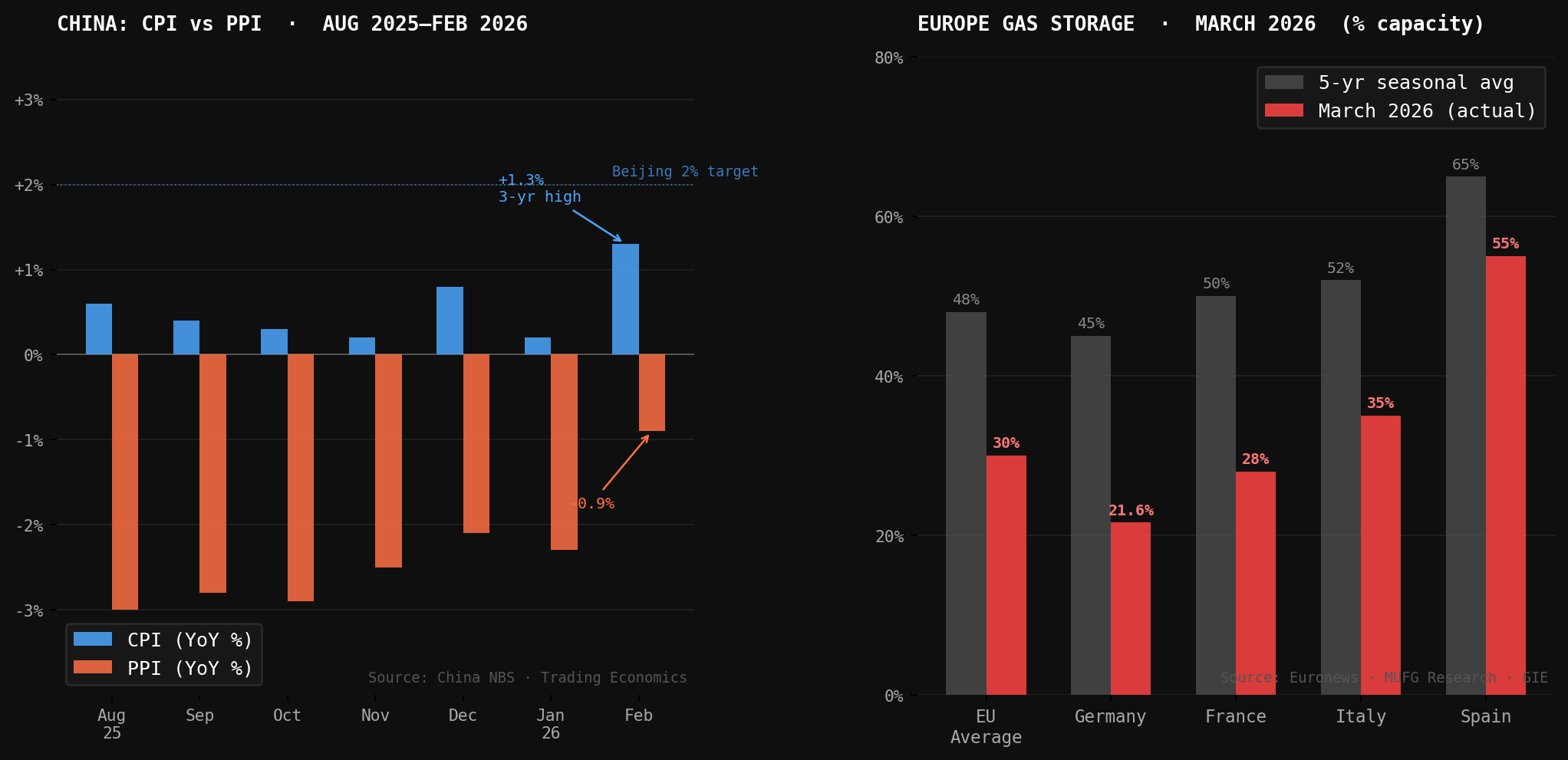

Europe walked into this with far less cushion than 2022. Gas storage was sitting at roughly 30% capacity — well below the 54% seasonal average — when the Dutch TTF benchmark surged 38–40% in a single trading session. QatarEnergy shut down the world's largest LNG facility and declared force majeure on exports. Insurers pulled coverage for Hormuz transits entirely. European gas prices rose 70% in a week, and at least one LNG tanker bound for France turned around mid-voyage toward Asia — a sign of just how fierce the scramble for remaining cargoes has become. Germany sits at 21.6% storage, France at 28%. Reuters puts the EU's full LNG refill bill for the coming injection season at potentially $40 billion.

China is playing a different hand. Tehran announced it would allow only Chinese vessels through the strait — rewarding Beijing's quiet support since the strikes began — giving Chinese refiners a supply edge that no other major importer currently has. But the domestic picture is still fragile. China's CPI hit a three-year high of +1.3% in February, edging toward Beijing's 2% target, while PPI stayed in deflation at -0.9%. Factory pricing still soft. Domestic demand still unconvincing. A sustained oil shock compresses industrial margins and reignites import costs at exactly the moment China needs neither. The preferential access through Hormuz is real, but it doesn't shield Beijing from what $120 oil does to the rest of the world it sells into.

Sustained high oil prices push inflation higher, tighten financial conditions, and move fragile economies toward recession in weeks — not quarters. The US consumer was already drawing down savings into a softening jobs market. Europe was heading into refill season with near-empty tanks and its largest LNG supplier offline. China's recovery was fragile before the first drone flew. One strait. Every wallet.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform