Market Sentiment Tracker: What Should We Be Watching in the U.S. Labor Market in 2026?

By

Osama

on January 13, 2026

in

Market Sentiment

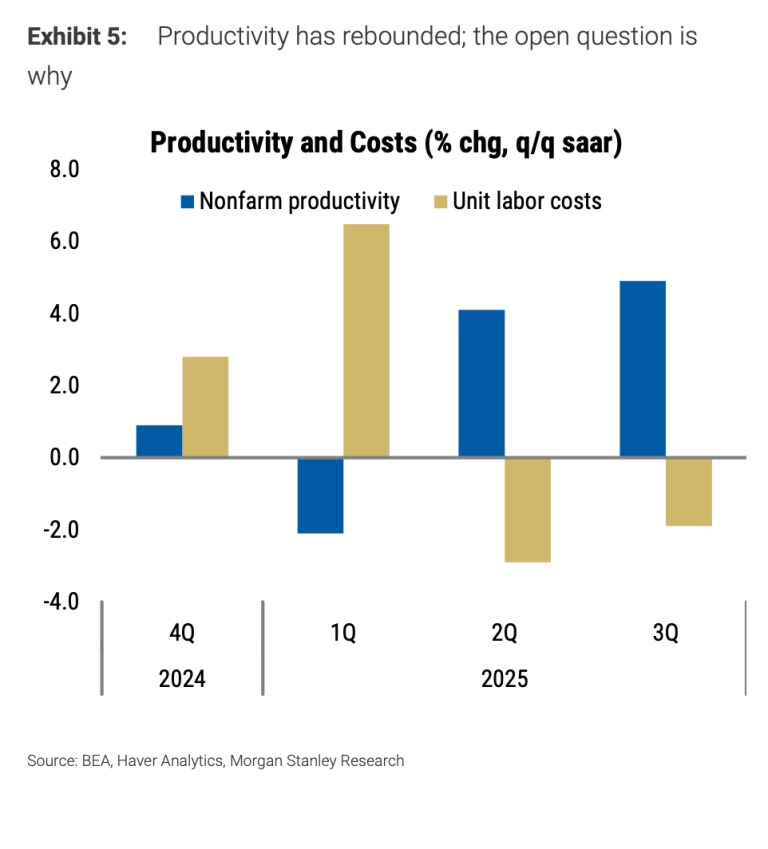

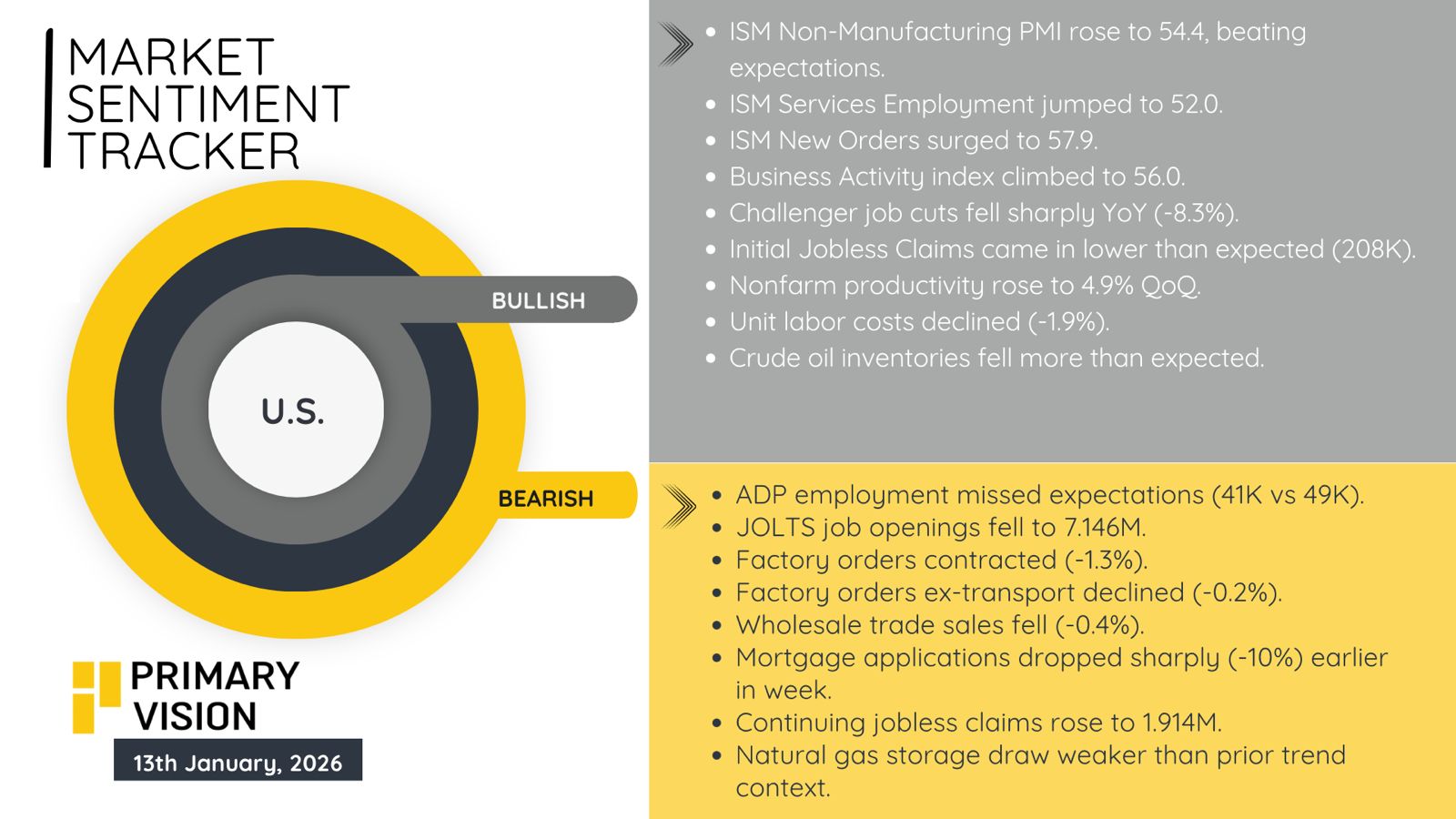

As we begin 2026, it is useful to step back and focus on the U.S. job market, because it explains much of what currently looks confusing in the broader economy. Output growth has been strong, inflation has not reaccelerated, and yet hiring has slowed to levels last seen during crisis periods. These facts are not contradictory, but they do point to a narrow and fragile balance. Recent productivity data sit at the center of this story. In the third quarter, nonfarm productivity rose at an annualized rate of 4.9%, following another strong increase in the prior quarter. Over the past four quarters, average productivity growth was closer to 1.9%. The recent pace is therefore well above what firms and policymakers have come to expect in a mature expansion.

At the same time, job growth has weakened substantially. In December, employers added just 50,000 jobs. For all of 2025, total job gains were approximately 584,000, or about 49,000 per month. In 2024, that monthly average was closer to 168,000. This is the weakest year of job creation since 2020 and one of the slowest outside of recession periods in recent decades. Despite this slowdown, unemployment has not risen. The unemployment rate fell to 4.4% in December after briefly touching 4.5% in November. For most of the past year, it has remained within a narrow range between 4.3% and 4.5%. This tells us that firms are mainly responding to uncertainty by limiting new hiring rather than cutting existing staff.

When firms keep headcount steady but continue producing at high levels, productivity increases. U.S. GDP grew at a 4.3% annual rate in the three months to September, even as monthly job gains hovered near zero. Output continued to expand while employment barely moved. That gap explains much of the recent productivity strength without requiring a major change in technology or business practices. Demand patterns help clarify why output has held up. Consumer spending rose 3.5% in the third quarter, led by services. However, spending power is increasingly concentrated. Households earning more than $150,000 now represent 43% of new car buyers, up from 30% five years ago. Households earning under $75,000 account for about 25%, down from 35%. Aggregate demand remains solid because higher-income households are still spending, even as lower-income demand weakens.

This matters because it limits how durable current growth can be. A consumption base that relies heavily on a smaller segment of households is more sensitive to asset prices and financial conditions. It also does less to support job creation in sectors that rely on broad-based demand. Technology does not yet appear to be the dominant explanation for reduced hiring. Most evidence suggests firms are correcting for excess hiring earlier in the recovery rather than replacing workers at scale. If demand slows or margins tighten, productivity growth could ease quickly.

Going into 2026, the labor market is best read less as a source of momentum and more as a barometer of confidence. With unemployment steady near 4.4% and hiring already compressed, the key question is not how many jobs are being added each month, but whether firms choose to start expanding again. That shift will show up first in hours worked, wage dispersion, and rehiring in cyclically sensitive sectors, not in headline payroll totals. Until those changes appear, slow job growth can coexist with solid output, but it also means the margin for error is thinner. The labor market will not lead the next phase of the cycle; it will reveal it once firms are convinced it has already begun.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform