Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Argentina and Mexico taps into shale

By Osama on April 13, 2026 in Market Sentiment

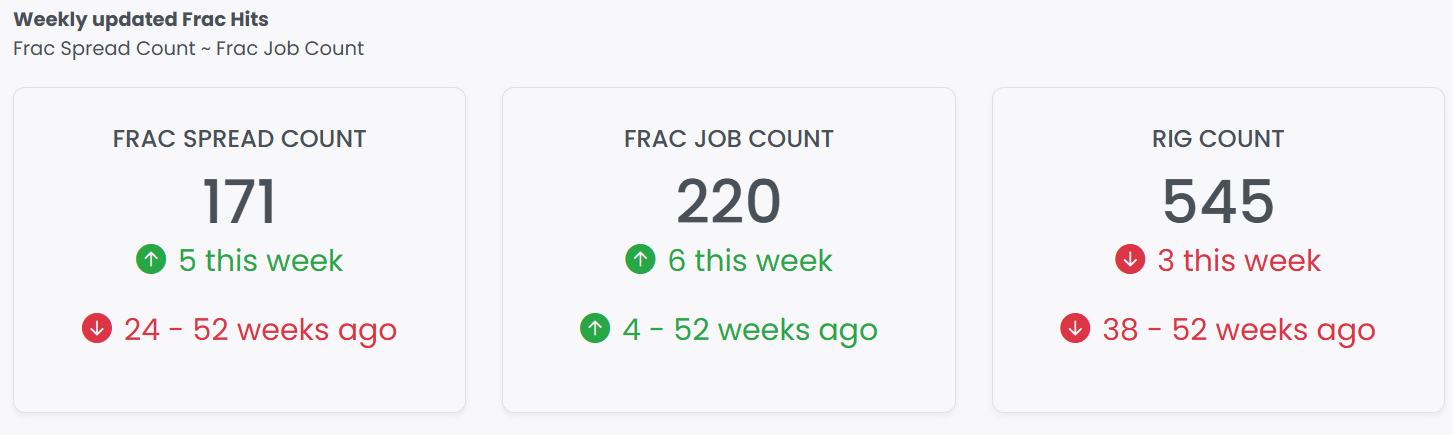

For the week ending April 10, the Frac Spread Count rose to 171, an increase of 5 from the prior week. The Frac Job Count reached 220, up 6 on the week. Both metrics reflect meaningful recovery since the start of the year — FSC has climbed approximately 15.5% from its January low of 148, while FJC has risen roughly 13.3% from its January low of 195. The Rig Count, however, declined by 3 to 545, and remains down 38 over the past 52 weeks. The contrast is notable: while drilling activity continues to soften on an annual basis, completion metrics are trending firmly higher, with FSC up 5 and FJC up 4 compared to 52 weeks ago.

Primary Vision has been monitoring the impact of the ongoing Middle East conflict and elevated oil prices on U.S. shale activity for several months (read our articles: here, here and here), and the weekly data is beginning to validate the bullish position we have maintained. The upward trend in both FSC and FJC since January is consistent with that outlook, and Primary Vision's forward projections — which will be detailed in an upcoming release — point to continued improvement in completion activity through the remainder of the year. This view is also finding broader support: Citigroup estimates that elevated oil prices driven by the Middle East conflict could prompt major shale producers to begin adding drilling rigs in the second half of 2026, with U.S. shale potentially adding around 815,000 barrels per day to global markets through 2028. The roughly 72% surge in crude prices since hostilities commenced has been cited as sufficient incentive for American oil executives to ramp up output. Industry estimates also point to the addition of between 8 and 12 frac fleets before year-end, a scenario that aligns with the momentum visible in Primary Vision's weekly data.

Argentina is emerging as a significant story in global unconventional energy development. Corporate borrowers there are turning to international debt markets not to restructure liabilities, as was common in prior years, but to fund direct investment in energy infrastructure. Goldman Sachs estimates that investment in Argentina's energy sector could reach $60 billion over the next five years, with the majority of that capital expected to come from overseas. Much of this is directed at Vaca Muerta, which holds the world's fourth-largest shale oil reserves and second-largest shale gas reserves. Argentine companies issued $2.1 billion in dollar bonds in the first quarter of 2026 — the busiest opening quarter since 2017 — signaling that capital markets are responding to the basin's development momentum with growing confidence.

Mexico, meanwhile, is taking a cautious but consequential step toward unconventional gas development. President Claudia Sheinbaum has proposed exploring hydraulic fracturing to reduce Mexico's dependence on imported natural gas, which currently accounts for 75% of domestic consumption, with the bulk imported from Texas. PEMEX estimates unconventional gas reserves at 141 billion cubic feet, nearly double the country's conventional reserves, and has outlined plans to reach 8.6 billion cubic feet of production within a decade, incorporating unconventional sources. Primary Vision and Bloomberg previously explored the considerable potential and structural challenges involved in any Mexican fracking program, and this latest proposal suggests the policy debate is moving from theory toward formal evaluation.

Taken together, this week's data and the broader developments across the Americas point to a global unconventional energy sector in measured expansion. In the United States, completion activity indicators are recovering from earlier caution as price signals strengthen. In Argentina, the financial architecture for a major production build-out is being put in place. In Mexico, a government long opposed to hydraulic fracturing is conducting a formal scientific review of its viability. These are distinct processes operating on different timelines, but they share a common driver: the recognition that unconventional resources represent a necessary part of the medium-term energy supply picture, particularly as geopolitical pressure on conventional supply chains remains elevated.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform