Monday Macro View: Can U.S. Shale Maintain Momentum in 2026?

By

Osama

on February 23, 2026

in

Market Sentiment

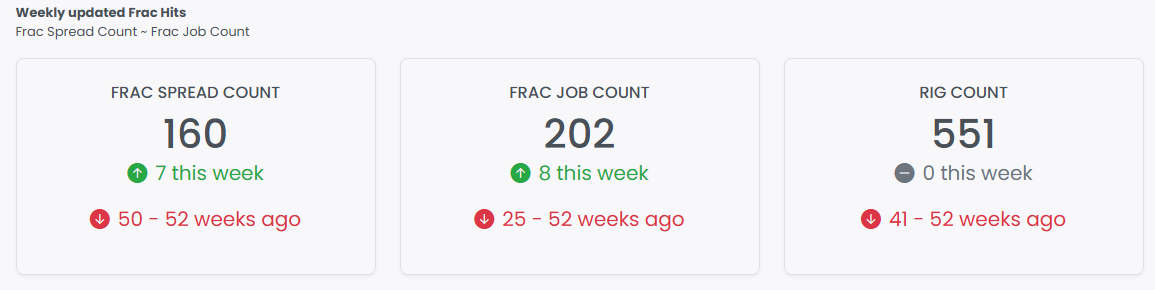

Our Frac Spread Count (FSC) and Frac Job Count (FJC) continues to recover with the former posting a gain of 7 on a WoW basis while the latter increasing by 8.

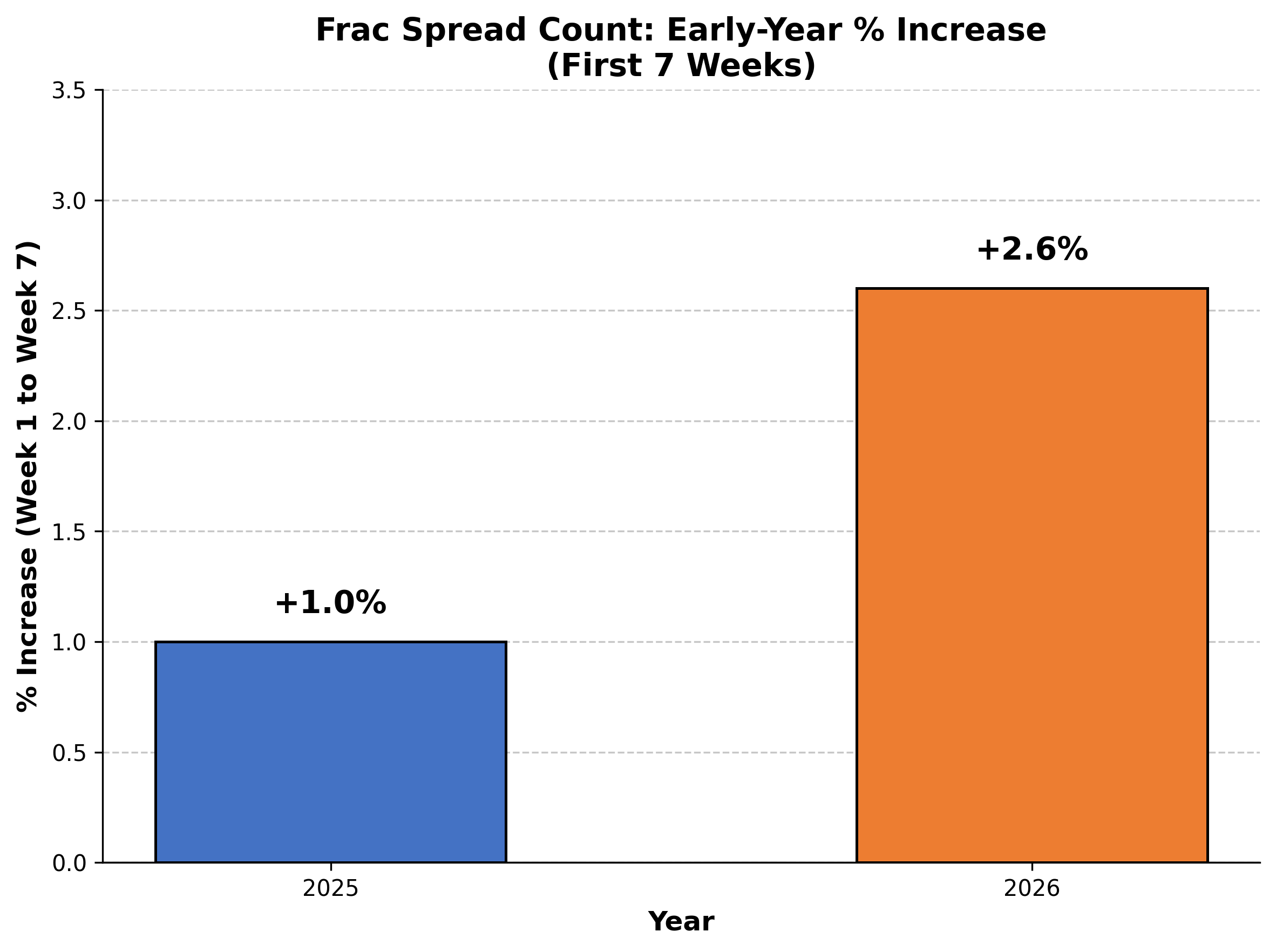

If we compare the behavior of Frac Spread Count in early 2025 vs 2026, an interesting pattern emerges. Despite operating at significantly lower absolute levels (averaging 155 vs 194 spreads), the early-year momentum in 2026 has been notably stronger. From the first week to the seventh week, FSC increased by +2.6% in 2026 compared to just +1.0% in 2025 — more than double the pace. This suggests that while operators are running fewer completion crews overall, they are ramping up activity more aggressively in 2026 relative to their starting point. Whether this reflects a catch-up from a slower holiday period, improved well economics, or operators front-loading completions ahead of anticipated price weakness remains to be seen.

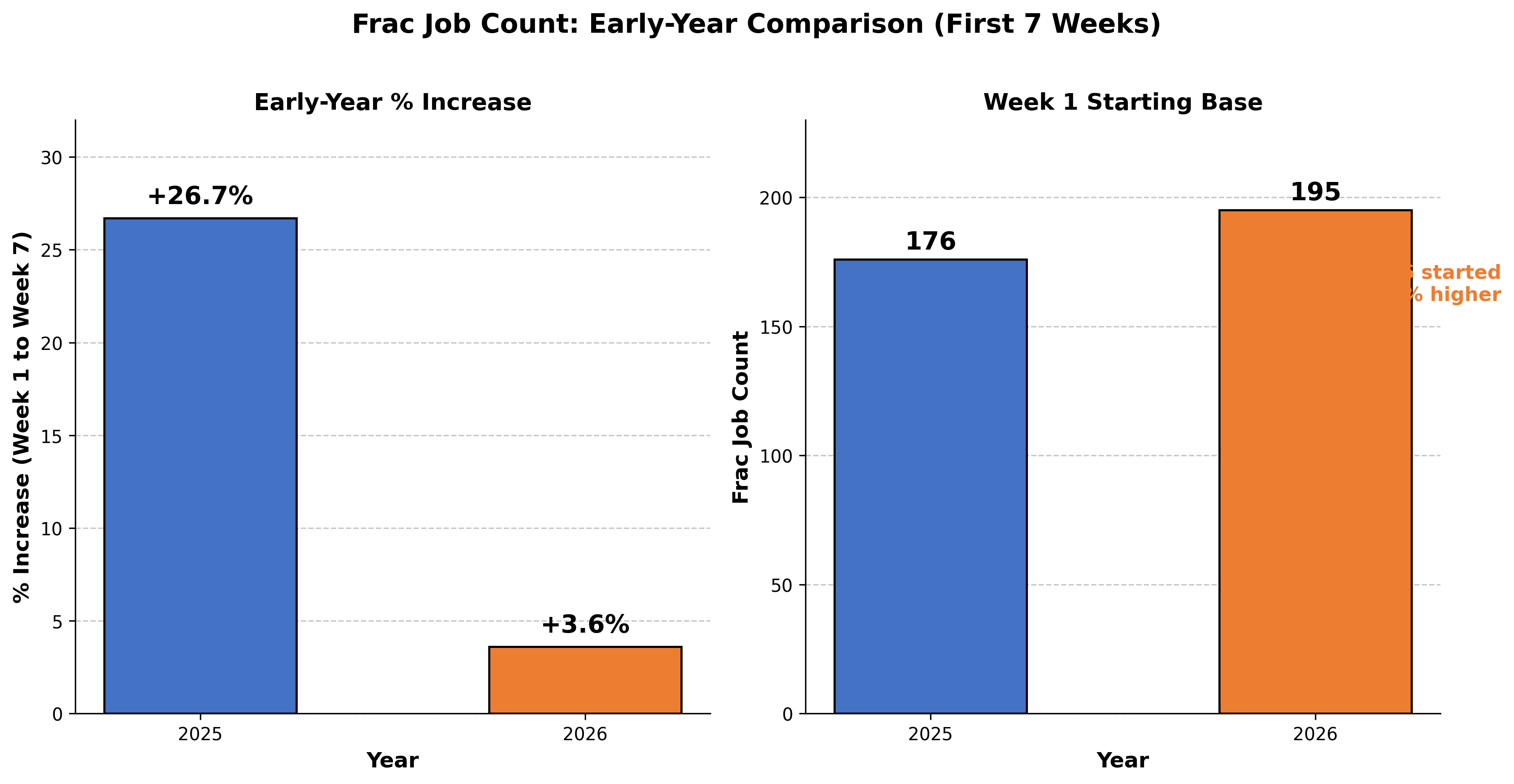

If we compare Frac Job Count in early 2025 vs 2026, the story is quite different from Frac Spread Count. While FSC has dropped 20% year-over-year, Frac Job Count has remained remarkably stable — averaging 201 jobs in 2025 vs 195 in 2026, a decline of just 3%. The early-year momentum tells an interesting tale: 2025 saw a sharp +26.7% ramp-up from Week 1 to Week 7, whereas 2026 shows a more modest +3.6% increase over the same period. However, this is largely because 2026 started from a higher base (195 vs 176 jobs in Week 1). The key takeaway? Operators are completing nearly the same number of frac jobs with significantly fewer active spreads, pointing to a notable improvement in crew utilization and efficiency in 2026.

The broader context here is that US shale remains the most responsive production base in global oil markets, and weeks like this reinforce why. The Permian continues to anchor the count, but we're watching Haynesville closely as AI-driven natural gas demand reshapes power market fundamentals. Data center buildouts are creating durable, baseload gas demand that didn't exist at scale five years ago, and that structural shift benefits US gas-directed drilling in ways the market hasn't fully priced.

On the operations side, automation and data integration are quietly compounding efficiency gains across the sector. Recent commentary highlights how operators are squeezing more from existing assets through smarter facility-level decision-making—fewer nuisance alarms, faster response times, reduced non-productive hours. These aren't headline-grabbing innovations, but they accumulate into meaningful cost advantages over time. US operators have spent a decade optimizing lateral lengths and stage spacing; the next leg of efficiency gains will come from surface operations and real-time data integration.

The power demand angle deserves attention. Big Tech's nuclear ambitions are real, but they're a 2030s solution to a 2025 problem. In the interim, natural gas is the bridge fuel that actually exists, and hyperscaler load growth is outpacing new generation capacity. This is bullish for Haynesville and Appalachian producers who can access power-adjacent markets, and it creates a demand floor that insulates gas-directed activity from the volatility we saw in prior cycles.

Internationally, Chevron's continued push into Venezuelan heavy crude reflects IOC pragmatism about where barrels are available—but it also underscores how much of the world's incremental production flexibility resides in US shale. Venezuelan volumes are politically constrained and infrastructure-limited; US tight oil scales with price signals and capital availability. That asymmetry isn't going away, and it keeps US producers structurally advantaged in a market where OPEC+ continues to manage supply with a heavy hand.

The bottom line: this week's activity uptick is consistent with a US shale sector that continues to deliver. Efficiency gains are real, demand tailwinds from power markets are building, and operators are leaning into completion programs with confidence. We remain constructive on US growth through 2026.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform