Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Oil Soars past $100, FSC and FJC continue to increase

By Osama on March 9, 2026 in Market Sentiment

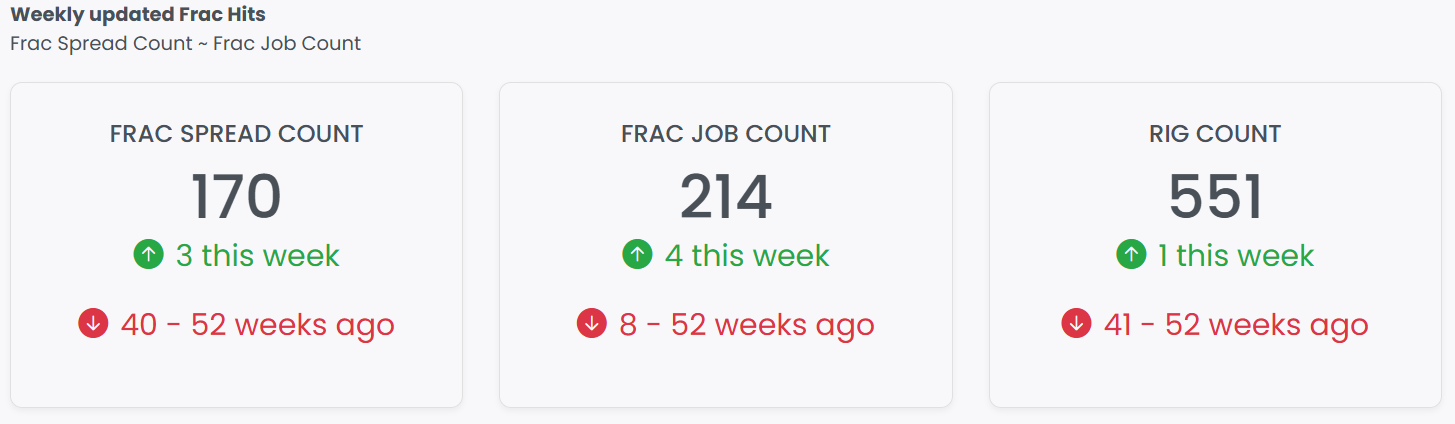

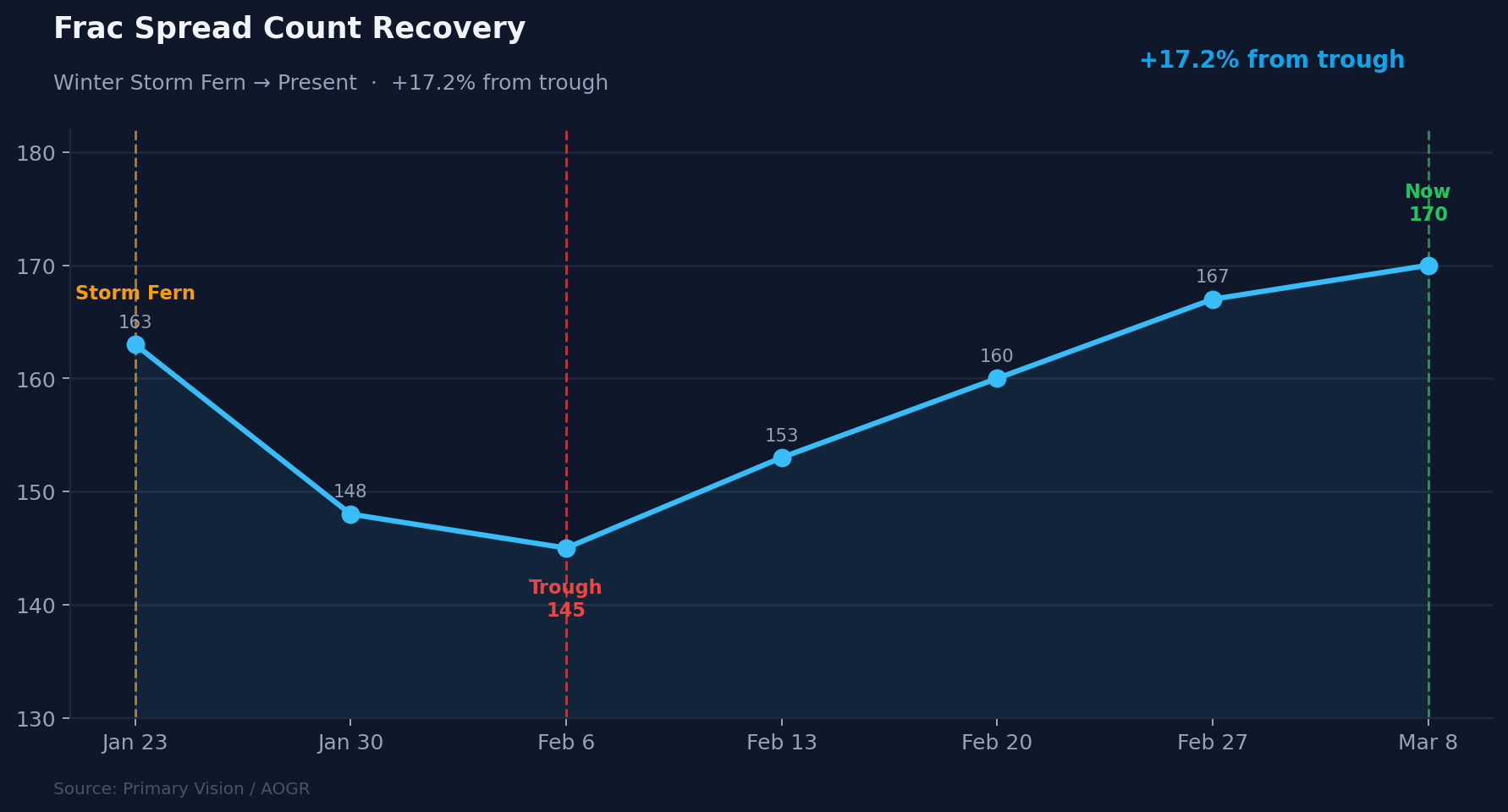

Primary Vision's Frac Spread Count came in at 170 this week, up 3, with the Frac Job Count at 214, up 4. This same week last year the count stood at 203 — but the more relevant comparison right now is the trajectory: from a February trough of 145, the FSC has climbed 25 spreads in under a month, with the FJC showing equally strong recovery momentum. That's a meaningful rebound, and it's landing into a price environment nobody had on their 2026 bingo card. WTI settled at $90.90 on Friday, up 36% from a week ago, with Brent climbing 27% to $92.69 — entirely war-driven. As markets opened on Monday both benchmarks jumped 25% soaring past $100 - hovering around $106.

The question now is whether the price signal sustains long enough to turn a recovery into genuine expansion - something I discussed in detail in the last Monday Macro View. So far we don't see new capital being committed. Shale executives say the patch would need prices stable at elevated levels for a year to warrant boosting production — and most expect a sharp pullback within weeks, before any new rig could even be contracted. If prices hold above $85 through mid-March and beyond, that calculus starts shifting. Sustained high prices are the one thing that pushes FSC and FJC meaningfully higher still. That's the watch.

The more immediate story for North American completions is gas, not oil. Qatar shut down the world's largest LNG facility after Iranian drone strikes, taking roughly 20% of global LNG supply offline, in some cases gas prices are a bigger problem than oil. European TTF surging over 80% in a week means every molecule US producers can liquefy is being bid for urgently — and one might expect that signal to show up in Haynesville and Appalachian completion activity over the next two to three weeks, potentially making gas-directed spreads the more interesting FSC story than oil in the near term. Whether that actually materializes is the thing to watch.

Another question many are asking is whether US shale can step up and replace the lost Middle Eastern barrels. The short answer is no. The IEA estimates shale could add only around 240,000 bpd initially and perhaps 400,000 bpd later in the year — a drop in the ocean against the 20 million bpd that transited Hormuz daily before the war. Shale executives are not rushing to boost drilling anyway — instead using the price spike to lock in future production through hedging and return cash to shareholders. The capital discipline era means $90 oil produces a +3 spread count, not a +20.

Let's not forget what's happening in Venezuela. PDVSA signed new contracts this week to supply crude to US Gulf Coast refineries, with Chevron targeting 300,000 bpd in exports this month alone. Interior Secretary Burgum visited Caracas on March 4 declaring he's "very optimistic" about investment flows, with Shell signing new oil agreements and ExxonMobil — which called Venezuela "uninvestable" just weeks ago — now sending a delegation in March. Chevron hit record production at its Venezuelan joint venture this week and the US says output could rise 30–40% in 2026. With $100 oil and Hormuz effectively closed, the urgency to get Venezuelan heavy crude flowing to US Gulf Coast refineries has never been higher. The long game just got a short-term catalyst.

On the OFS side, the war just complicated the central thesis of 2026. Every major services company — Halliburton, SLB, Patterson-UTI, H&P — had staked their growth narrative on Middle East unconventional expansion: Jafurah, UAE, Kuwait, Oman. That was the margin recovery story meant to offset soft North American pricing. Halliburton's offices and warehouses in Basra were hit by an Iranian drone strike on March 7, with the company reporting a "security incident". The international upcycle isn't cancelled, but its operational risk profile just changed materially in a single week. For a sector where Halliburton's own guidance already called for high-single-digit North American revenue declines in 2026, losing confidence in the Middle East growth engine at the same time is a meaningful double headwind.

The number to watch isn't the spread count. It's how long $85+ oil holds. Four weeks of it and public E&Ps start quietly revising completion guidance upward. Eight weeks and the rig conversations begin.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform