Outlook and Key Projects: Into 1Q 2026, BP expects upstream production to remain broadly flat versus Q4, while downstream results soften seasonally, with lower customer volumes and weaker refining margins partly offset by reduced turnaround activity. For full-year 2026, underlying upstream production is expected to be broadly flat, with stable oil output offset by lower gas and low-carbon volumes. BP is guiding to $13–13.5 billion of capex, weighted to the first half, alongside $9–10 billion of divestment proceeds, largely back-end loaded and including the Castrol transaction. Structural cost reduction targets were raised to $5.5–6.5 billion by end-2027, underscoring a focus on balance sheet resilience and cash discipline rather than volume-led growth.

In Q4, the company advanced several strategically important projects, including first oil from the Atlantis Drill Center 1 expansion in the Gulf of America, progress on offshore developments in Brazil, and final investment approval for subsea projects in Australia. BP also continued with its Castrol divestment. Management emphasized capital discipline, lower 2026 capex, and structural cost reductions as key priorities as BP balances near-term earnings pressure with longer-term value creation.

The Q4 Results Analyzed

BP reported a net loss of $3.1 billion in Q4, compared with net income of $1.5 billion in Q3. Impairment charges of approximately $4.0 billion, largely within gas and low-carbon energy assets, drove the Q4 loss. Underlying replacement cost profit declined sequentially to $1.5 billion from $2.2 billion, reflecting lower upstream realizations, production mix effects, and reduced refinery utilization due to higher turnaround activity. RC profit reflects BP’s underlying operating earnings, excluding inventory holding gains or losses caused by commodity price movements.

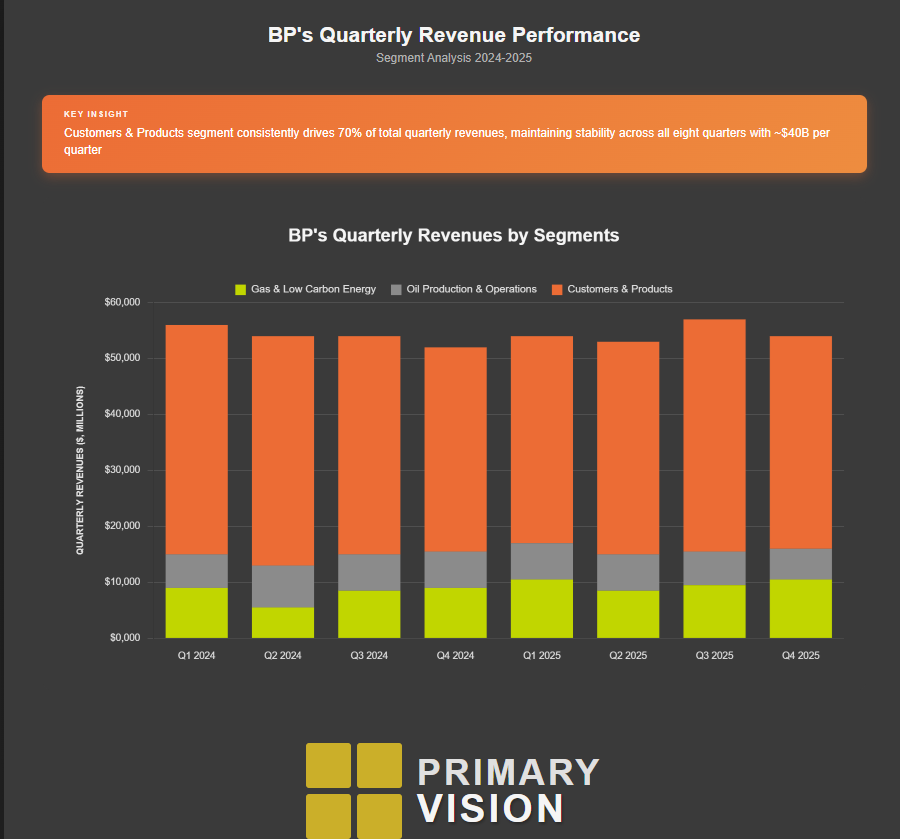

In the Gas & Low Carbon Energy segment, underlying profit declined sequentially, pressured by lower realizations and impairment charges. In Oil Production & Operation, earnings fell as liquids realizations softened. In the Customers & Products segment, which deals in high-volume, downstream and customer-facing activities, results weakened in Q4 due to seasonality.

Cash Flows, Dividend, and Buyback: For FY2025, BP generated approximately $24.5 billion in operating cash flow, down year over year, reflecting weaker underlying earnings and lower commodity realizations despite disciplined cost control.

Long-term debt fell by 1% year over year, while it reduced share buybacks. BP maintained its base dividend through the year but paused buybacks in Q4, signaling a shift in capital allocation priority toward deleveraging and balance sheet resilience amid earnings volatility.

Thanks for reading the BP Take Three, designed to give you three critical takeaways from WFRD's earnings report. Soon, we will present a second update on BP’s earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.