Articles

- BLOG / Articles / View

- Articles

Is America Ready to Fuel the World's NGL Hunger?

By Osama on April 2, 2026 in Market Sentiment

Natural Gas Liquids do not dominate energy headlines the way oil and LNG do, but they sit at the intersection of U.S. upstream activity, petrochemical feedstocks, and global energy trade — and right now, the world is scrambling for every barrel America can produce.

A brief explainer for context. NGLs — ethane, propane, butane, and natural gasoline — are extracted from the natural gas stream during processing. Ethane goes primarily to chemical plants to make plastics. Propane heats homes, dries crops, and increasingly gets loaded onto ships and exported to Asia and Europe. They are a byproduct of the same completions activity tracked weekly by our FSC and FJC data — more frac activity, more associated gas, more NGLs.

The global demand picture has been building structurally for years. Global LPG consumption stood at 427 million tonnes in 2024, with forecasts pointing to 528 million tonnes by 2035, driven overwhelmingly by Asia-Pacific petrochemical demand and residential use across developing economies. The U.S. has cemented itself as the world's swing supplier — the incremental exporter of NGLs for growing global demand, a role that has now become acutely consequential. The Middle East, which supplies nearly 30% of global LPG exports, has been effectively cut off from markets following the U.S.-Israel conflict with Iran and the de facto closure of the Strait of Hormuz. India alone — with domestic output covering only 40% of its LPG demand — has seen its supply chain thrown into acute crisis, with panic buying and fuel rationing spreading across the economy. The world is not just hungry for U.S. NGLs. It is desperate.

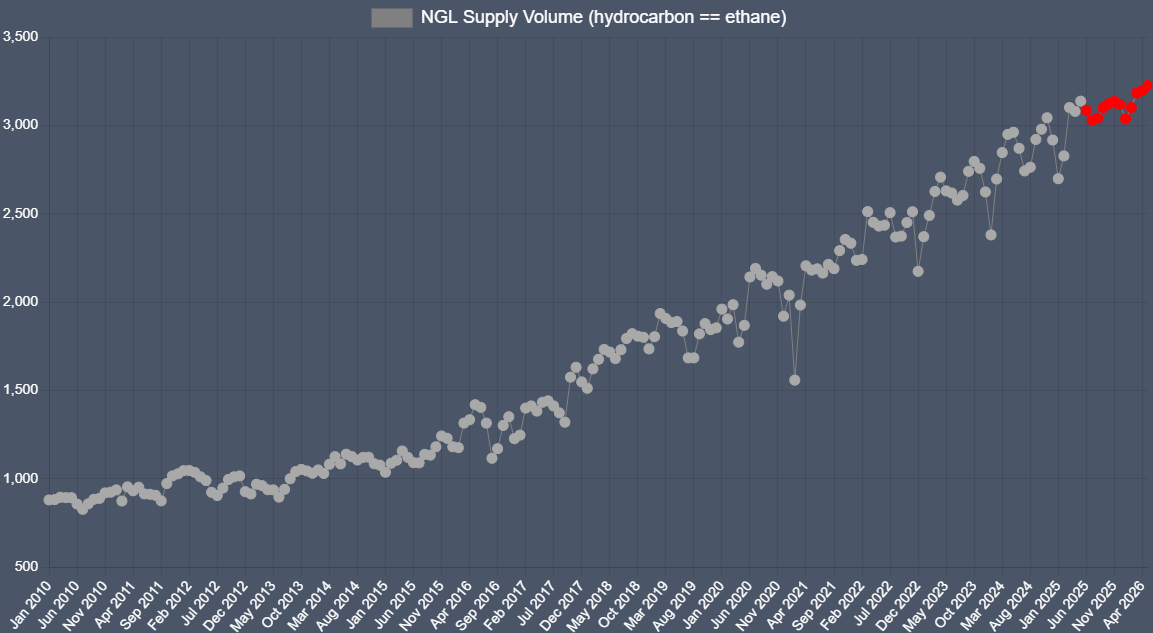

Against that backdrop, our proprietary data tells a precise story. On ethane, supply and demand are running in close balance, with forecasts pointing to approximately 3,200 Mbbl/d by May 2026. U.S. petrochemical crackers have been steadily absorbing rising supply and no visible stress is present. One sensitivity worth monitoring: when natural gas prices rise sharply, producers can choose to leave ethane in the gas stream rather than extract it as a chemical feedstock — a practice known as ethane rejection. Whether that dynamic materializes in the current price environment remains to be seen, but petrochemical consumers will be watching closely.

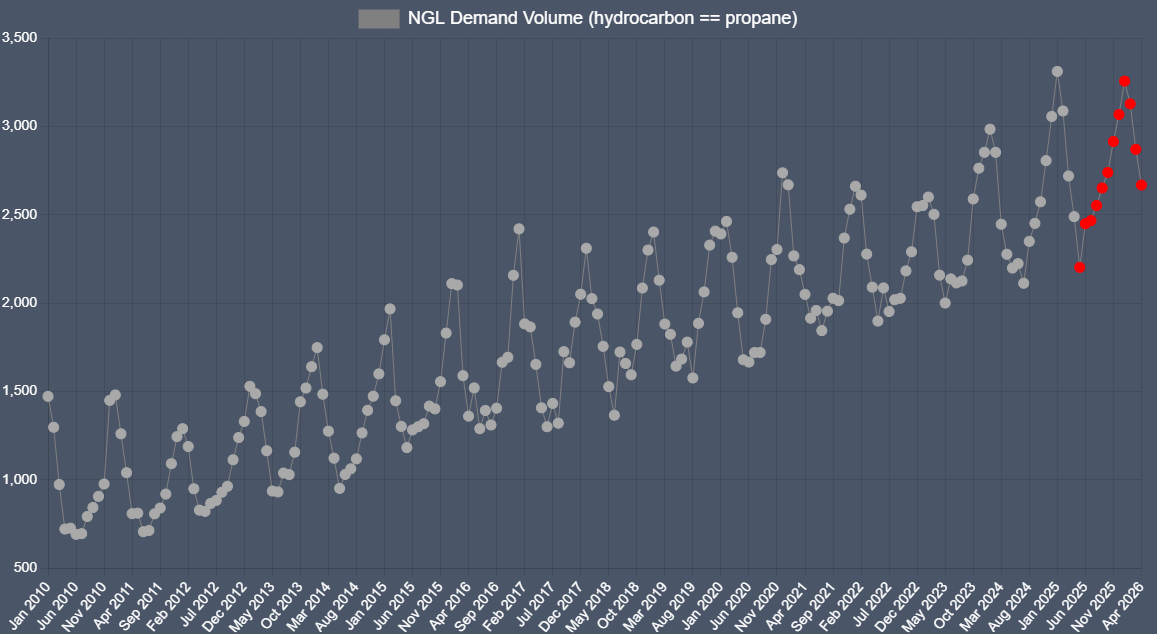

Propane is where the tension is already visible in our data. Our NGL demand monitor shows propane demand spiked hard in late 2025 into January 2026, consistent with strong winter heating demand combined with export pull. The forecast shows demand moderating through spring — normal seasonal behavior — while supply drifts slightly from a peak of around 2,780 Mbbl/d toward 2,749 by May. In an ordinary year, that convergence is unremarkable. This is not an ordinary year. The prompt Far East Index propane contract has increased 58% since February 28, while the European propane benchmark has surged 60% over the same period. The northwest Europe propane benchmark hit a four-year high, with a single-session gain that exceeded anything seen even during COVID-19. U.S. propane has risen 22% in the same window, primarily tracking crude — but the global market is pricing in something far more severe.

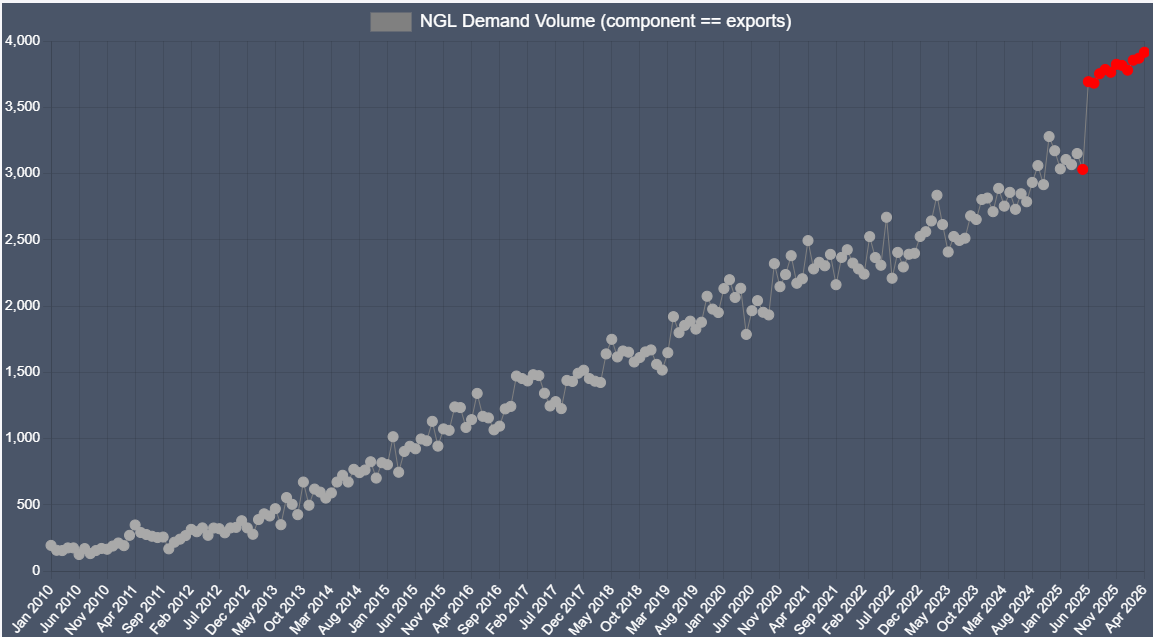

The export data is where our numbers sharpen into a real story. Our NGL export demand monitor shows aggregate U.S. NGL export volumes forecast to reach 3,915 Mbbl/d by April 2026 — the highest level in our dataset. That is not a seasonal bump. U.S. propane exports were already expected to grow approximately 9% in 2025 compared to 2024, following 30% growth the prior year, and the Middle East disruption has now poured fuel on that fire. Targa Resources declared force majeure on LPG loadings from its Galena Park terminal in March following mechanical failures, further tightening an already strained global market — a stark illustration of how little slack exists in the loading infrastructure. The three largest U.S. LPG terminals are exporting near or above their nameplate capacity. The demand is there. The infrastructure is being tested.

The dynamic worth watching into the second quarter is the relationship between that export demand trajectory and the upstream activity picture our completions data reveals. NGL supply growth is tied directly to frac activity, and our FSC and FJC data shows year-on-year softness in key producing regions. Supply is still growing, but record export demand and a moderating completions base are converging. Global ethane demand is projected to increase by 800,000 bbls/d between 2025 and 2030, while propane demand is expected to grow by another 350,000 bbls/d over the same window — long before upstream activity has any hope of catching up. How that resolves — through price response, accelerated upstream investment, or infrastructure rationing — is the NGL question that matters most heading into the back half of 2026.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform