Market Sentiment Tracker: As 2026 Approaches, Three Major Economies Face Very Different Questions

By

Osama

on December 9, 2025

in

Market Sentiment

As we head into 2026, it feels like the right moment to pause and look at where the world’s major economies are actually heading, rather than where headlines or forecasts say they should be. The past few years have produced unusual combinations of shocks—pandemic recovery, inflation cycles, geopolitical realignment, and uneven global demand—and many of the assumptions that guided earlier economic cycles no longer hold cleanly. This article is an attempt to make sense of that landscape in a clear, data-driven way. The goal is not to issue predictions, but to outline the forces shaping the United States, Europe, and China as they enter a year defined less by crisis and more by structural adjustment.

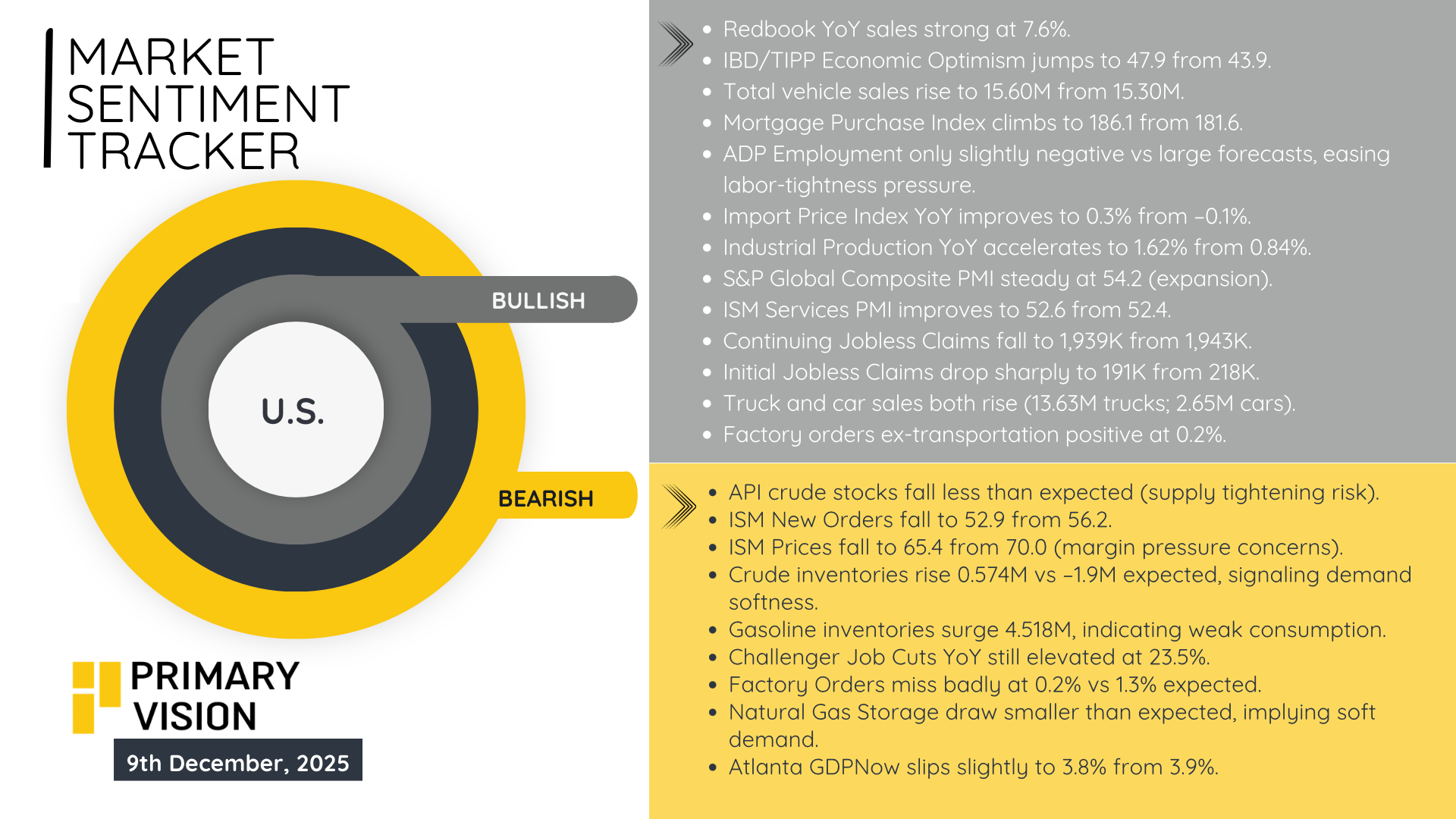

For the United States, recent data suggests steadiness across consumption, labour markets, and industrial production, which may carry into 2026. Vehicle sales have risen, consumer sentiment held up, and inflation (while elevated) shows signs of moderation — a combination that supports private demand without forcing aggressive rate tightening. At the same time, investment and manufacturing output remain relatively healthy, suggesting that real economic activity may grow at a steady — if unspectacular — pace. That said, after years of monetary tightening and renewed fiscal pressure on debt service, any slowdown in wage growth or consumer credit could quickly erode momentum. Real household spending and housing remain key vulnerabilities. In aggregate, the U.S. economy seems positioned for “soft-landing-style” growth: neither a boom nor a bust, but a prolonged mid-cycle muddle where policy rates, inflation expectations, and global demand swings determine the direction.

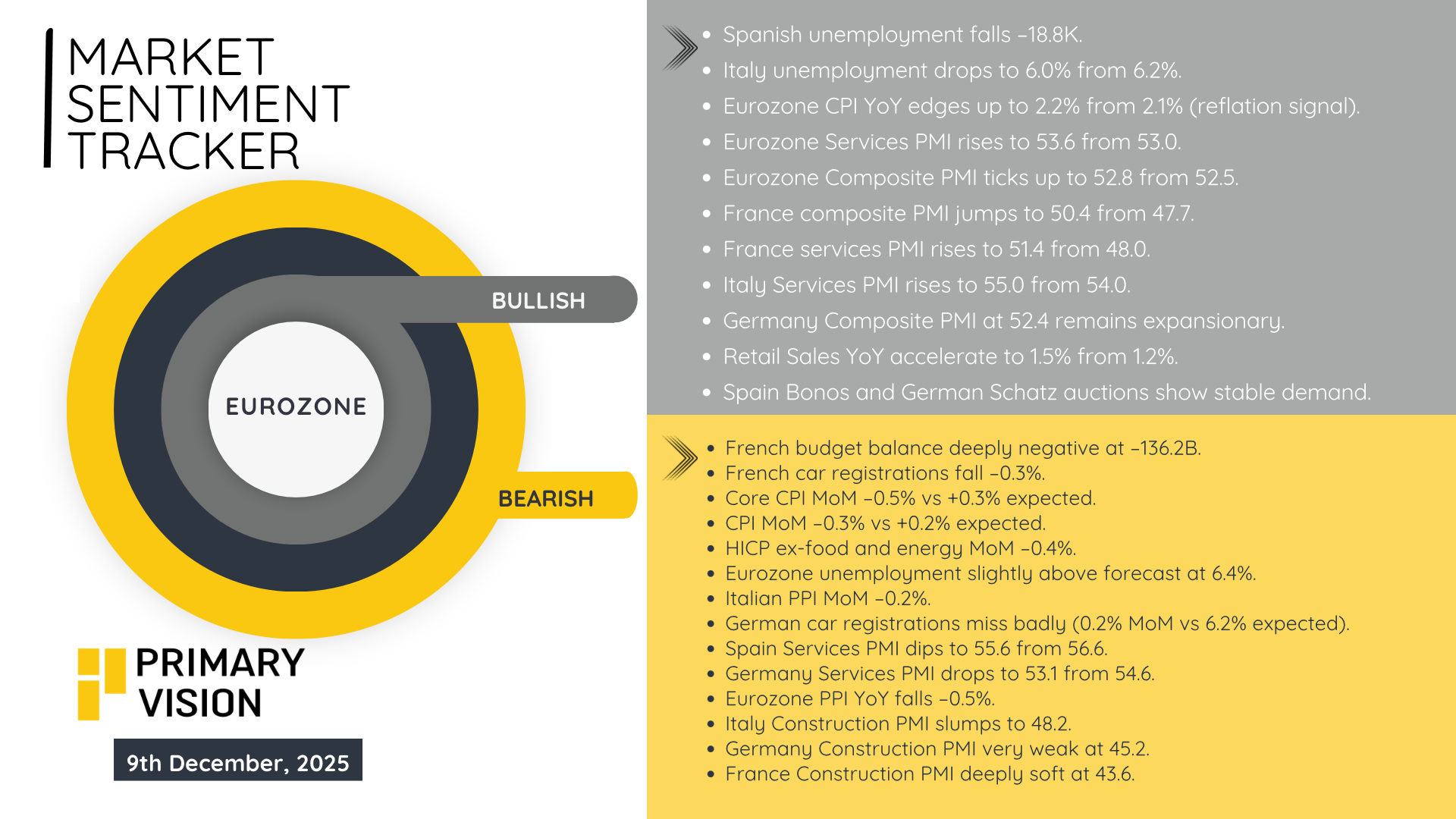

Europe enters 2026 with a fragile mix of moderate consumption recovery, structural industrial weaknesses, and tight inflation/fiscal constraints. According to forecasts, real GDP growth for major economies like Germany is projected at around 1.2 % in 2026, while euro-area inflation is expected to hover close to 2 %. Lower energy prices reduce headline inflation and ease pressure on real incomes, supporting household spending and some rebound in construction or public investment. Yet export-oriented sectors — especially heavy industry and manufacturing — remain under pressure from global demand softness and lingering trade tensions, limiting their ability to lead a strong recovery. At the same time, public debt levels and demographic headwinds constrain aggressive fiscal or pension reforms. Europe’s structural challenge in 2026 is modest growth under constraints: domestic demand alone may sustain low-to-mid growth, but the lack of export rebound and limited productivity gains raise questions about long-term competitiveness and the ability to absorb future shocks.

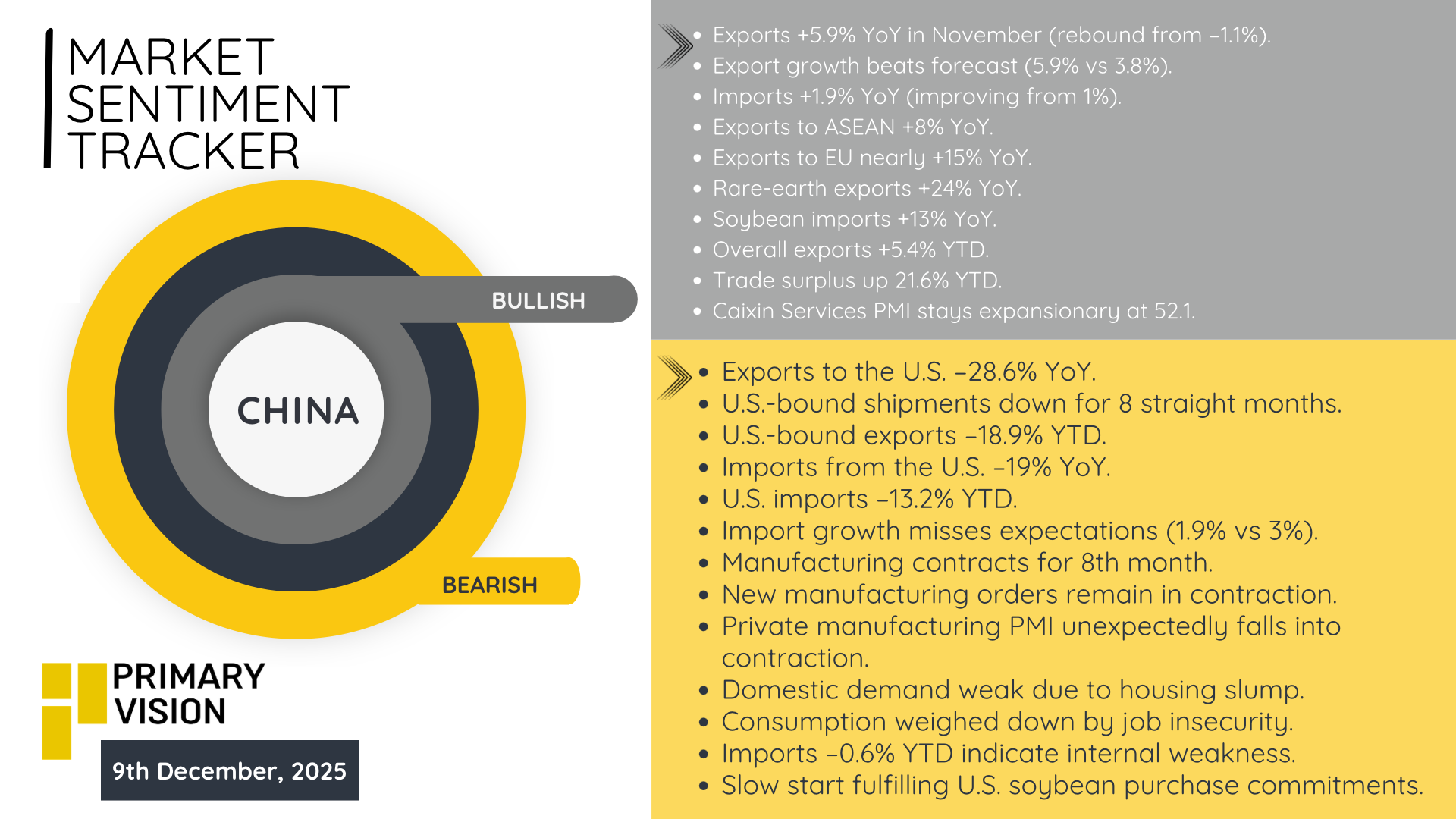

China’s 2026 outlook reveals deep structural trade-offs as the economy transitions from its traditional growth engines toward a more fragile, consumption- and manufacturing-driven model under global pressure. In 2025, Chinese exports rebounded strongly — up 5.9 % year-on-year in November — and total trade surplus surpassed US$1 trillion over the first 11 months. Exports remain robust in global markets outside the United States, supported by strong demand for goods such as EVs, batteries, and green-tech equipment, and rising rare-earth shipments. Despite this, domestic demand remains weak: consumption and real estate investment are subdued, household savings remain high, and industrial overcapacity looms large. As a result, 2026 is likely to see growth rates moderate — many forecasts expect a drop from around 5 % to roughly 4.4 – 4.5 % unless policy stimulus is ramped up. The broader implication is that China’s growth may increasingly rely on state-led industrial and export-oriented strategies, rather than broad-based domestic demand — a shift with significant global supply-chain, trade, and investment ramifications.

Looking across the three regions, it becomes clear that 2026 is not shaping up to be a year defined by a single global narrative. Each economy is carrying its own mix of strengths, constraints and unresolved questions, and none of those paths line up neatly.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform