Articles

- BLOG / Articles / View

- Articles

Market Sentiment Tracker: Let's Talk about oil demand in 2026

By Osama on December 2, 2025 in Market Sentiment

Every week I write about the global economy covering Europe, China and the U.S. I write about the numbers coming in from each of these and whether they had a bearish or bullish tilt. But this week, I thought to do something different. One question that is on everyone's mind is what will be the outlook for oil demand in 2026? Estimates galore. But I want to look at it in a systematic manner. Therefore, we are going to investigate the factors, sectors, elements that mainly determine oil demand and see how are they going to fare. From there we will form an opinion regarding oil demand.

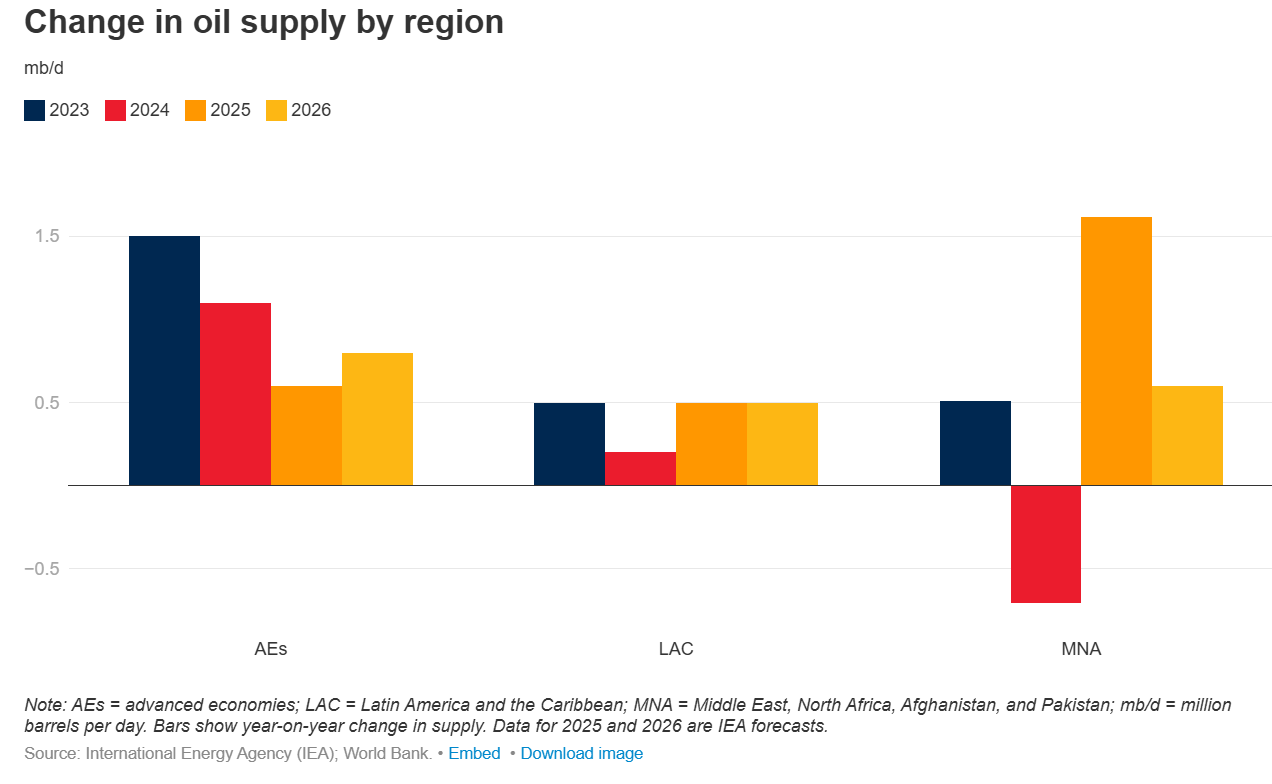

In 2025 global oil demand growth remained modest. According to International Energy Agency (IEA) data, world oil demand rose by roughly 700–740 thousand barrels/day (kb/d) in 2025. The demand growth in 2024 had already slowed: consumption rose by just 0.8% (approximately 830 kb/d) to 193 EJ in energy-terms. Refinery activity rebounded in 2025 after some earlier disruptions. Global refinery runs, which had dipped (in part due to maintenance and outages), are scheduled to rise — the IEA forecasts that refining throughputs will increase toward the end of 2025 and continue into 2026. Global oil supply is also growing faster than demand. The IEA projects supply will increase by about 3.1 million b/d in 2025 and by another 2.5 million b/d in 2026. This implies a likely oversupply situation in 2026, with an implied surplus of roughly 4 million b/d if demand growth remains subdued.

Given that macro backdrop, the outlook for different sectors diverges.

IEA’s Oil Market Report notes that 3Q25 demand growth was led by petrochemical feedstocks (LPG/ethane, naphtha), and that overall oil demand growth in 2025–26 is only ~700 kb/d per year, so feedstocks account for a disproportionate share of the incremental barrels. The medium-term Oil 2025 and Oil 2024 outlooks both show petrochemicals taking over a third of total oil-demand growth to 2030, with feedstock use rising even as road fuels plateau. Combined with ongoing cracker and PDH capacity additions in China, the US and the Middle East, that suggests modest but steady feedstock demand growth into 1H26, even in a sluggish macro.

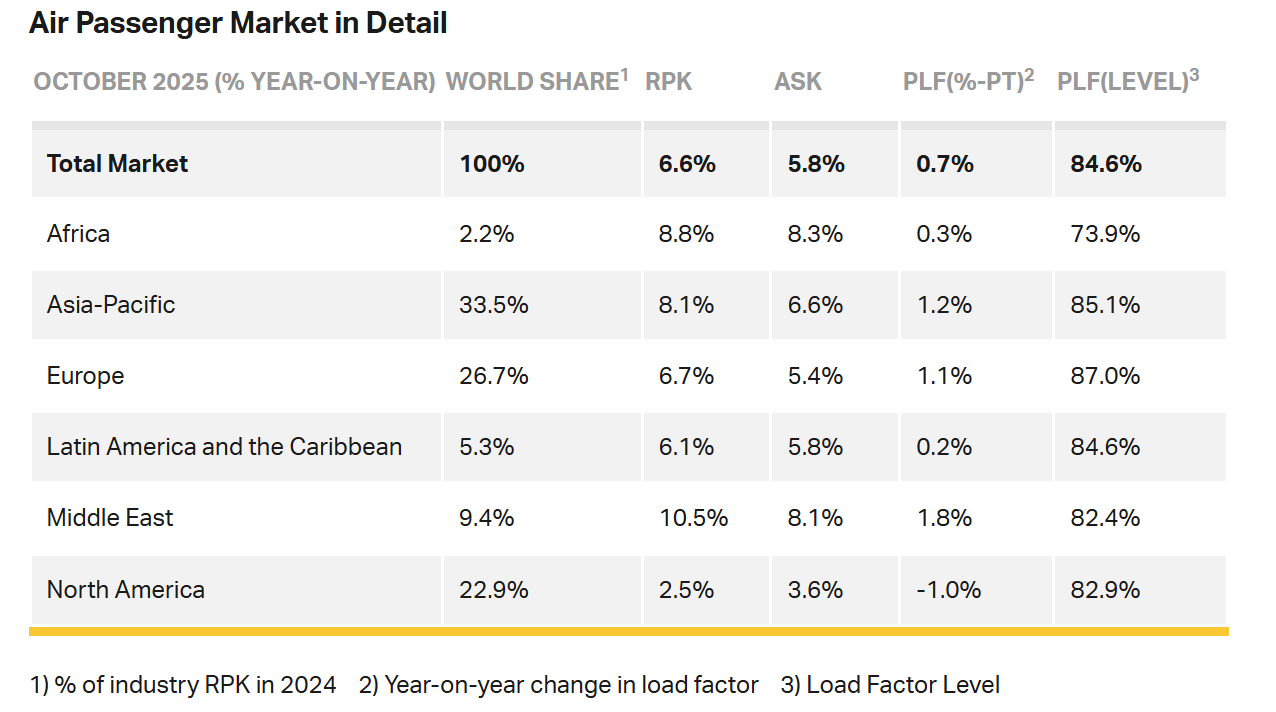

IATA and industry forecasts still have air travel as a growth pocket: global passenger demand and RPKs continued expanding in 2025, with airlines guiding to further traffic gains into 2026. Aviation fuel demand in 2025 continued to recover toward pre-pandemic levels, underscoring the role of emerging markets. At the same time, SAF is <1% of fuel and fleet efficiency gains are gradual, so jet fuel remains a net positive contributor to oil demand in early 2026, but not enough to offset weakness elsewhere. Source: IATA

Source: IATA

The diesel complex looks structurally softer: IEA has flagged gasoil as the “weak point” in the barrel, with 2025 gasoil/diesel demand remaining subdued, and only tepid growth beyond. Data shows diesel demand already under pressure from weak manufacturing and construction in 2025, substitution by LNG trucks, and a broader freight downturn, while U.S. diesel futures hit multi-year lows on demand concerns. Truck OEMs like Volvo are guiding for a weak North American heavy-duty cycle through 2026, which caps freight-related diesel upside, even if marine fuel oil stays somewhat supported by 2025’s longer shipping routes and ‘shadow fleet’ activity.

On road fuels, the big story is EVs and efficiency: IEA’s Oil 2025 sees global demand levelling off around ~105–106 mb/d by late decade, with road transport growth sharply curtailed. EV penetration accelerated further in 2025, continuing to displace incremental oil demand toward 2026. China’s own fuel use for gasoline, jet and gasoil in 2025 showed signs of flattening, with IEA and multiple analysts now talking about an early peak in Chinese gasoline demand as EVs, LNG trucks and high-speed rail bite. Oxford Energy Institute shows that OECD road fuel demand in 2026 is flat/down, non-OECD up a bit, but the global contribution to oil demand growth is very small.

Taking all sectors together, the evidence points to modest but positive global oil-demand growth in 2026. Petrochemicals and aviation continue to provide reliable upside, together adding close to 1 mb/d, but this strength is partly offset by structural weakness in road fuels and diesel-linked freight, which likely subtract 0.3–0.4 mb/d from gross gains. As a result, the most defensible call is that 2026 demand growth lands slightly below but broadly in line with the IEA’s ~700 kb/d baseline. My central estimate is ~650 kb/d of net growth—firm enough to avoid contraction, yet far too soft to tighten a market facing several million barrels per day of incremental supply.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform