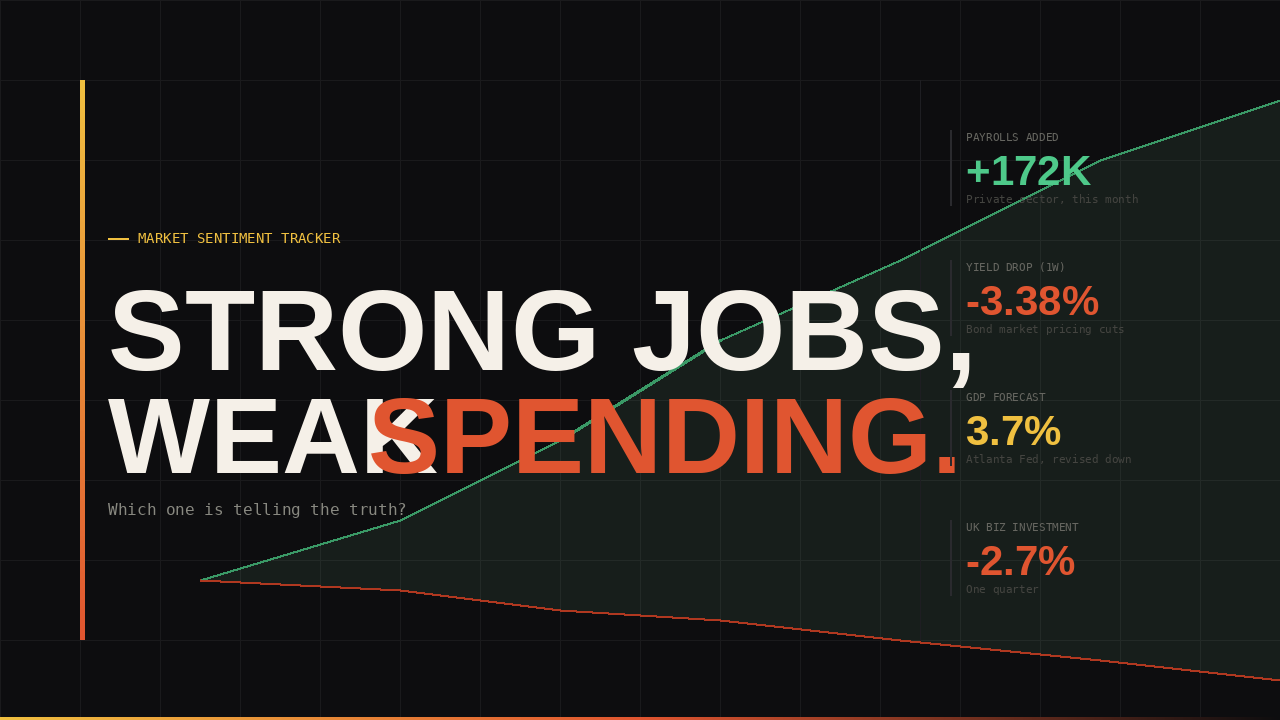

The S&P dropped 1.85% this week (but later recovered) despite payrolls crushing estimates by nearly double. Treasury yields fell 3.38% to 4.06%. That's the puzzle everyone's trying to solve—why are stocks falling when jobs look this good?

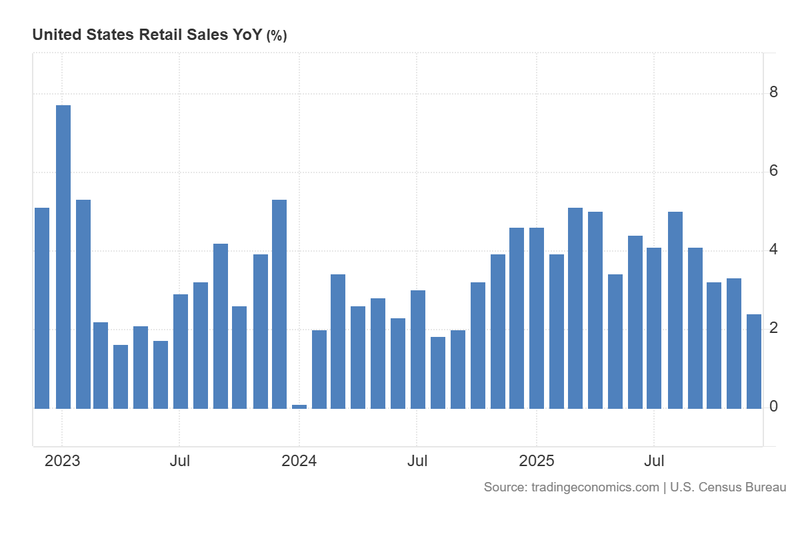

The answer is simpler than it appears: look at what consumers are actually doing, not what the labor market says they should be doing. Retail sales hit zero growth when markets expected 0.4%. Core retail sales also zero. The retail control group went negative. When all three measures flat-line or decline simultaneously, it means that consumers are, if not worried, then at least concerned about what's going on.

The housing data makes this clearer. Existing home sales collapsed 8.4% in a single month. That's not a rate story anymore. Home sales don't drop that hard because yields moved a few basis points. They drop because household balance sheets are under some real stress. People with secure jobs and rising wages don't suddenly stop buying houses unless something fundamental changed in their financial position.

Bond traders aren't buying the optimism. Yields dropped 3.38% in a single week — and bond markets move like that when they're pricing in Fed cuts, which only happens when traders expect the economy to weaken. The Atlanta Fed's GDPNow tracker already revised its forecast down from 4.2% to 3.7%, meaning those strong payroll numbers aren't really showing up in actual output.

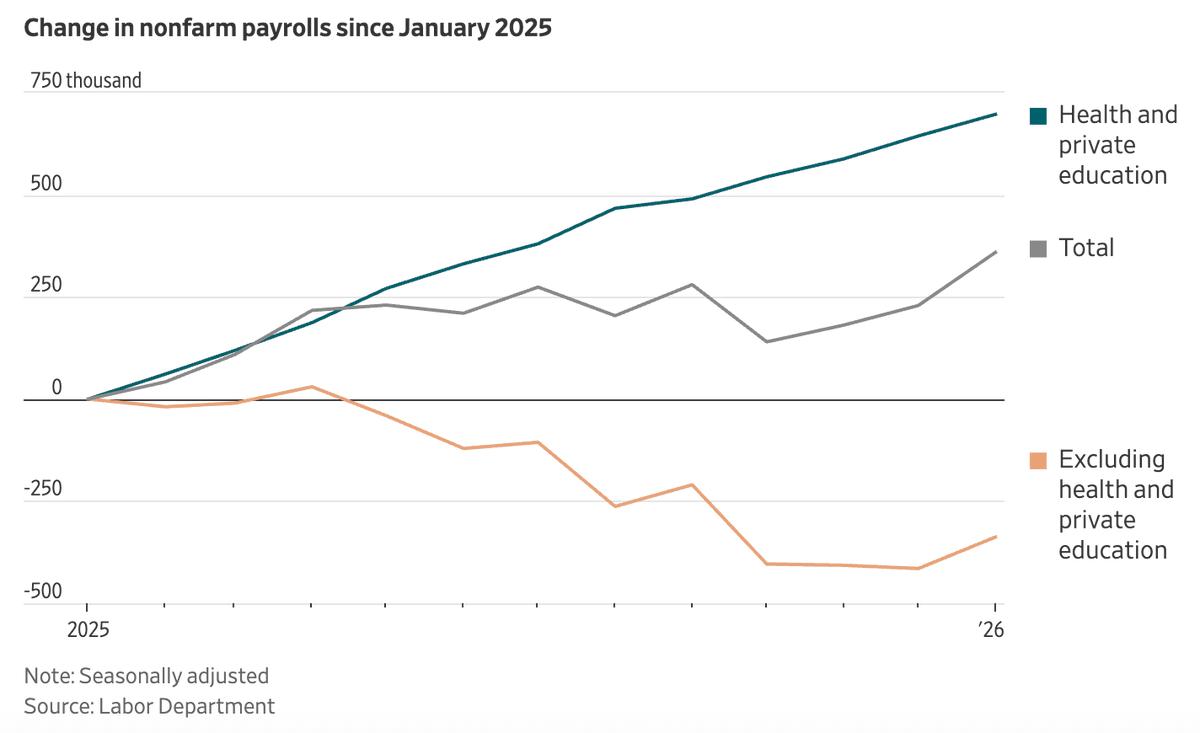

Those payrolls deserve a closer look too. Government jobs fell 42K. Private sector added 172K — sounds solid, until you realize manufacturing accounted for just 5K of that. The rest almost certainly landed in services: retail, hospitality, healthcare. These sectors get revised heavily after the fact and don't tend to put as much money in people's pockets as higher-wage industries. Strong headline, shakier foundation.

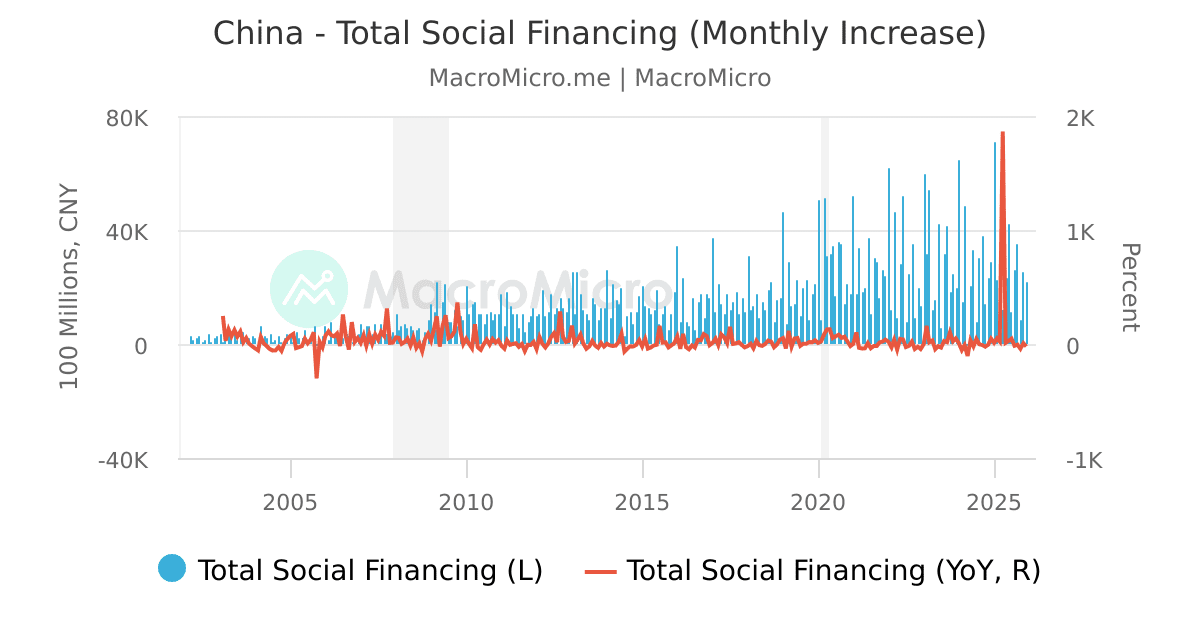

Zoom out to China and the picture gets harder to ignore. Beijing injected7.22 trillion yuan in social financing into the economy even as home prices keep falling around 3.1% year-over-year. A property sector accounting for roughly a quarter of GDP remains broken, and authorities are throwing credit at the problem to stop things from getting worse. When the world's largest manufacturer gets this aggressive about propping up demand, global trade is usually already weaker than the official numbers let on.

The UK adds another layer. Business investment dropped 2.7% in a single quarter — companies don't make cuts like that over temporary jitters. That happens when management sees structurally lower demand ahead. Pair it with broad weakness across UK industrial output, manufacturing, construction, and services and Europe's second-largest economy starts looking like it's in the early stages of something more serious. A few things worth watching closely: jobless claims — even a modest uptick starts eroding the strong labor market story. The next retail sales print — a weak number puts the Fed in an uncomfortable spot given what bond markets are already pricing in. And crude inventories — stockpiles building despite supposedly robust employment would signal that global demand is softening regardless of what the payroll surveys say.

The gap between strong jobs data and weak consumer spending can't stay open forever. Right now the bond market is making a pretty clear bet about which one gives way first.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform