Market Sentiment Tracker: What is behind Global Market Selloff?

By

Osama

on February 4, 2026

in

Market Sentiment

Global markets sold off sharply at the start of February 2026 despite historically loose financial conditions. Asian equities led declines, with South Korea’s KOSPI falling more than 5% in one session, while broader regional indices dropped close to 3%. The most extreme moves were concentrated in metals. Gold fell more than 6% intraday and silver declined nearly 12%, reversing a large portion of January’s gains . Leveraged exposure magnified losses: the 2x silver ETF AGQ fell roughly 60% in a single day after having risen more than 150% year-to-date, with trading volume hitting a record 38 million shares. Oil prices fell over 4%, while the U.S. dollar stabilized after a prolonged decline.

These moves may have deeper factors. For instance, U.S. financial conditions had in fact eased materially, with the Goldman Sachs Financial Conditions Index falling to 98.3, its lowest level since early 2022. Policy rates had been cut by 175 basis points since September 2024, the dollar had weakened roughly 12% over the past year, and investment-grade credit spreads had compressed to levels last seen in the late 1990s. Asset prices had adjusted accordingly, particularly in areas tied to liquidity and leverage.

The selloff was therefore driven less by fundamentals than by positioning. Extremely loose financial conditions encouraged leveraged exposure to assets perceived as beneficiaries of monetary easing, especially precious metals. As prices rose, exposure became increasingly concentrated in futures and leveraged ETFs, making the market fragile to even modest shocks. Once volatility increased, margin requirements were raised and forced selling followed. The collapse in leveraged silver products illustrates how quickly price moves can overshoot when liquidity is abundant but positioning is crowded.

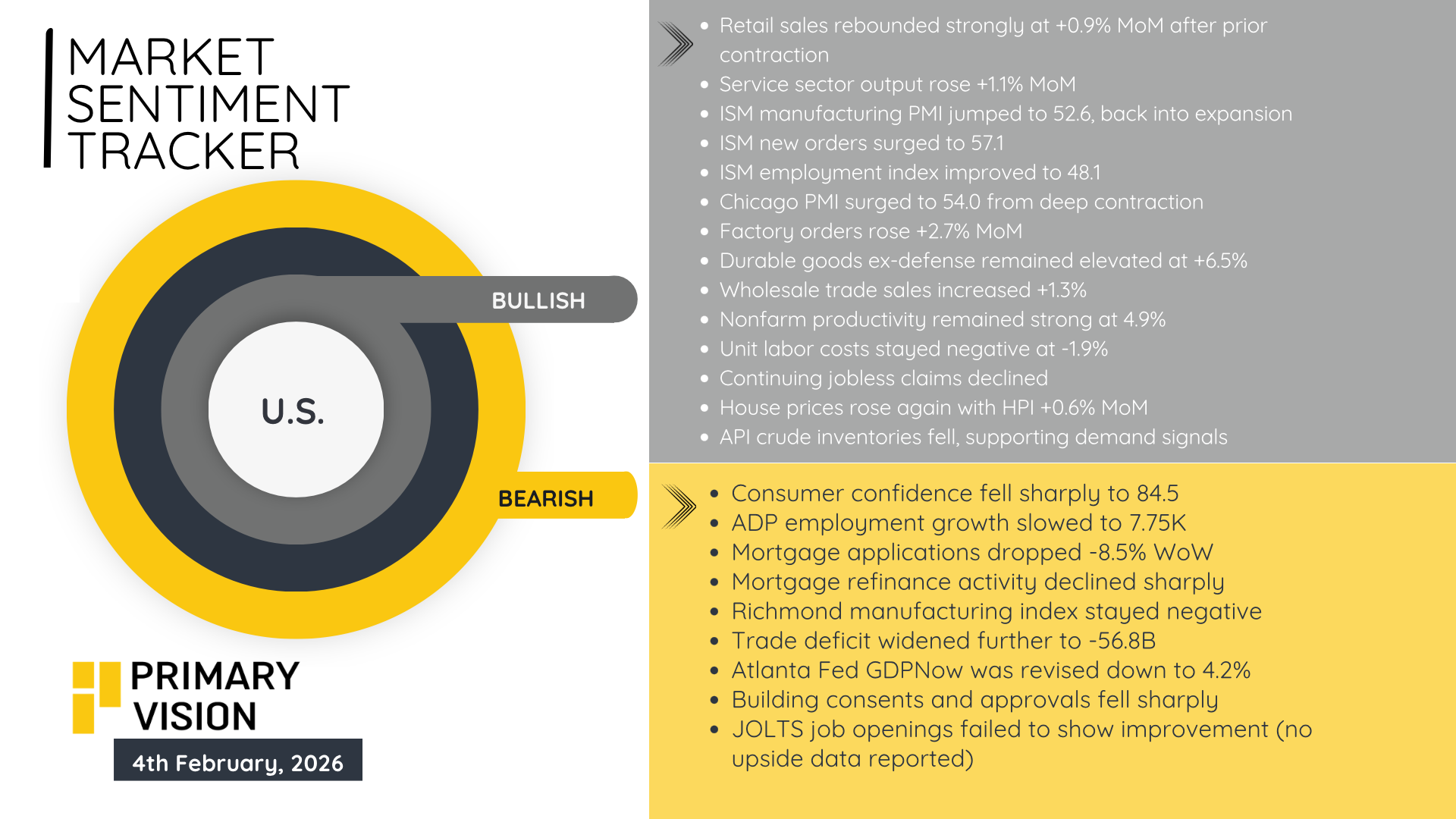

However, overall the U.S. sentiment tracker showed a bullish tilt.

Equities were affected through the same channel. Systematic strategies and risk controls respond to volatility and correlation, not valuation. As metals began to unwind and volatility rose, exposure was reduced across assets simultaneously. This episode reflects a market constrained not by tight money, but by excessive leverage built during a prolonged period of easing.

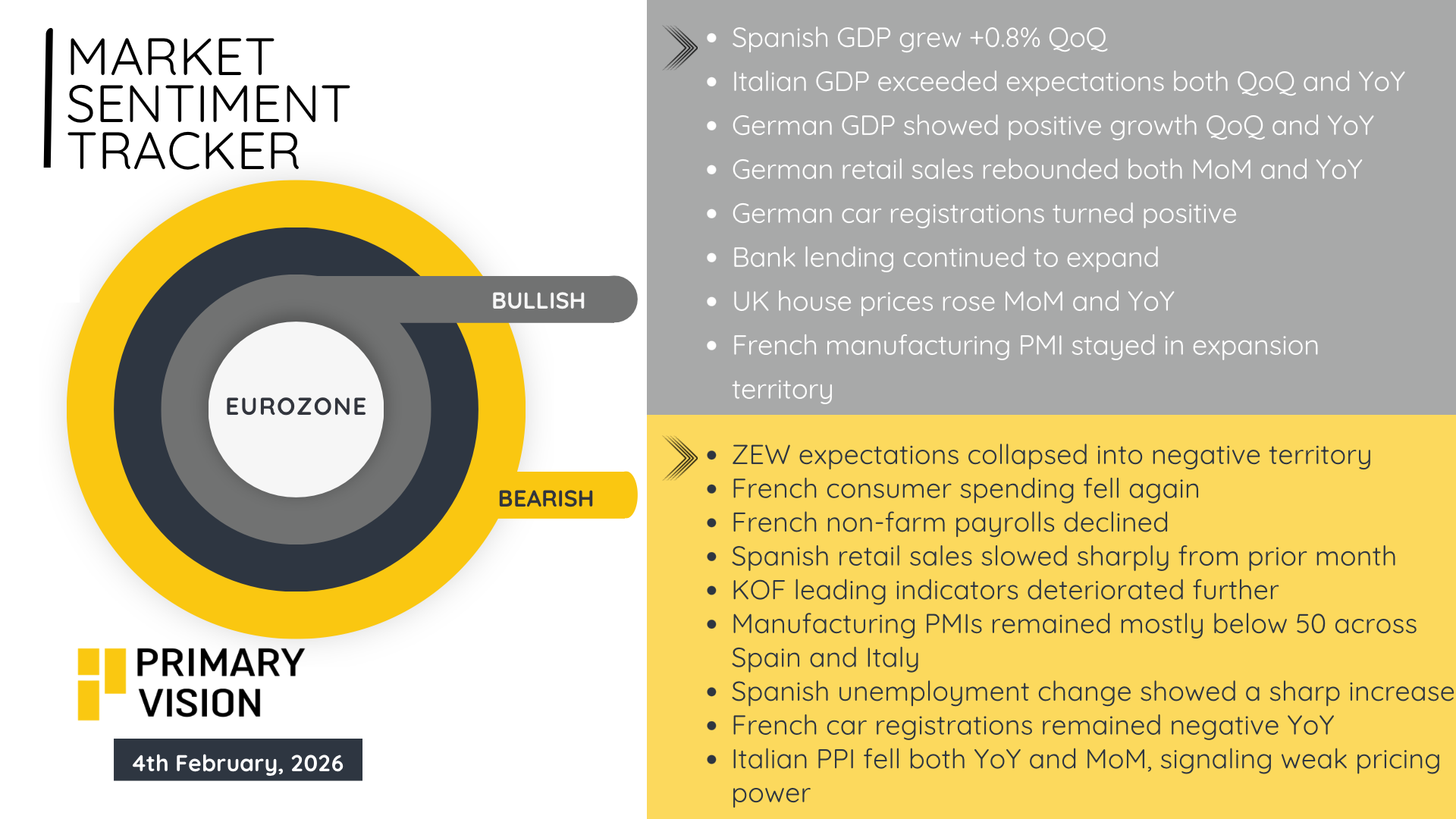

Across the pond, we also saw some positive developments in Eurozone. The recent spat with the U.S., has brought the countries together and a sudden realization of solidarity is underway. This may help alleviate differences that often impact economic issues as well.

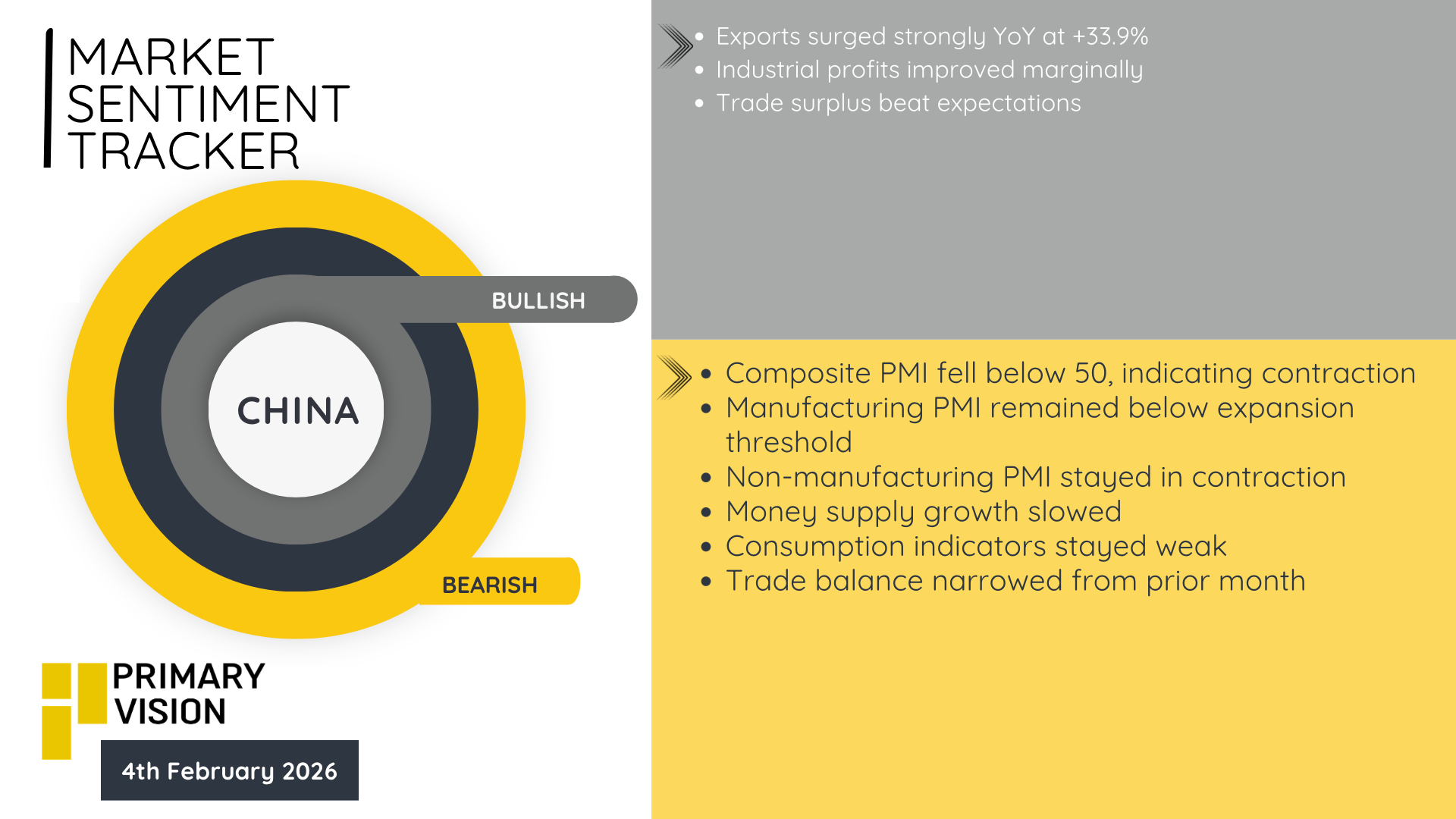

Finally, in China, we saw a clearly bearish tilt. Manufacturing PMI remained the expansion territory while non manufacturing PMI stayed in contraction. Consumption also weakened. But we covered this in our last Market Sentiment Tracker and warned against having an extremely bearish outlook for China.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform