Monday Macro View: Iran-U.S. War: When Do Higher Oil Prices Actually Drive Drilling?

By

Osama

on March 2, 2026

in

Market Sentiment

Oil prices surged more than 7% Monday as unprecedented joint US and Israeli strikes on Iran escalated tensions across the Middle East, with WTI climbing toward $72 per barrel, the highest in over eight months. The immediate question facing shale operators is whether sustained higher prices will trigger a ramp in completion activity, or whether this becomes another brief geopolitical spike that fades before capital budgets get pulled forward.

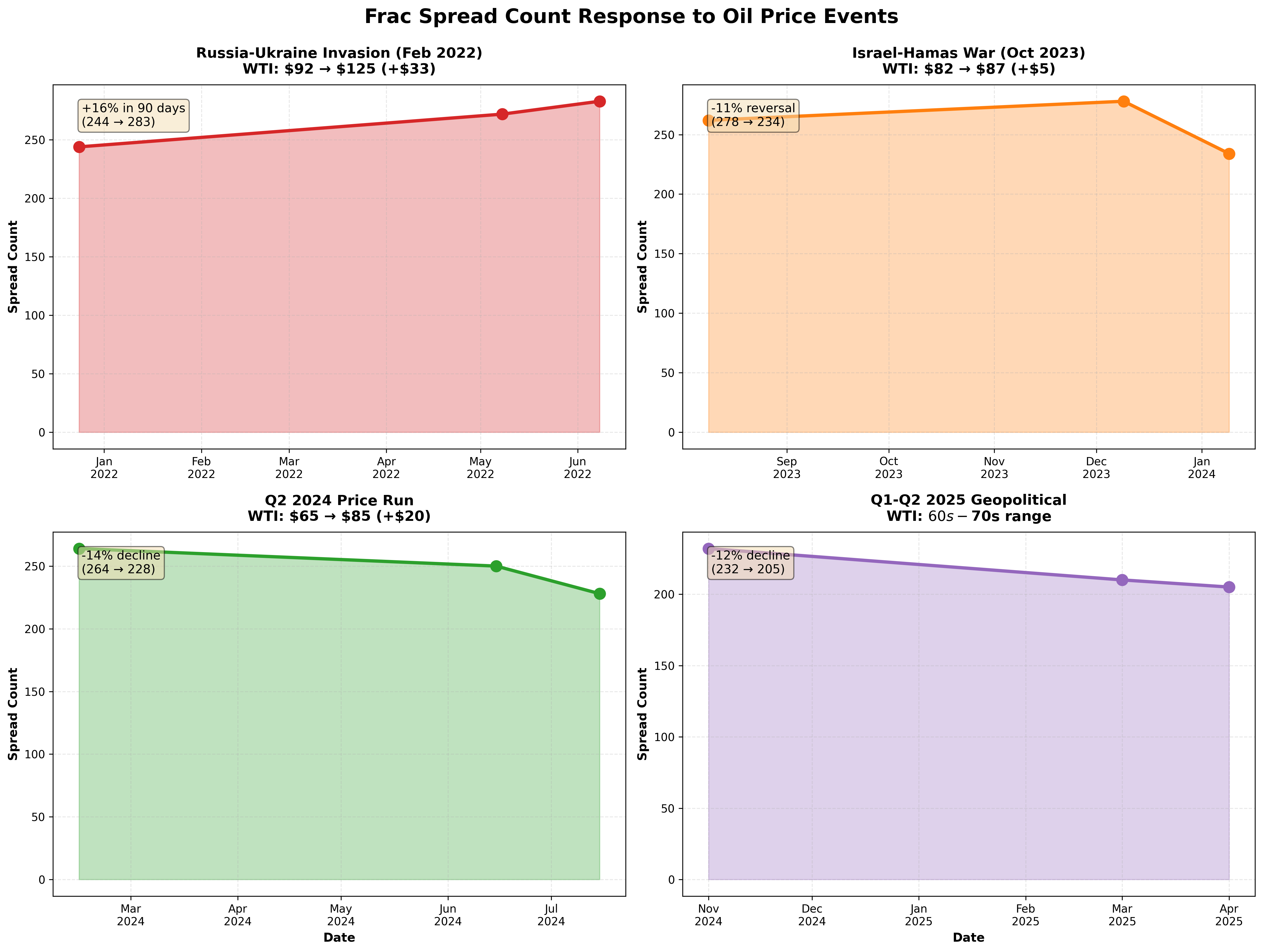

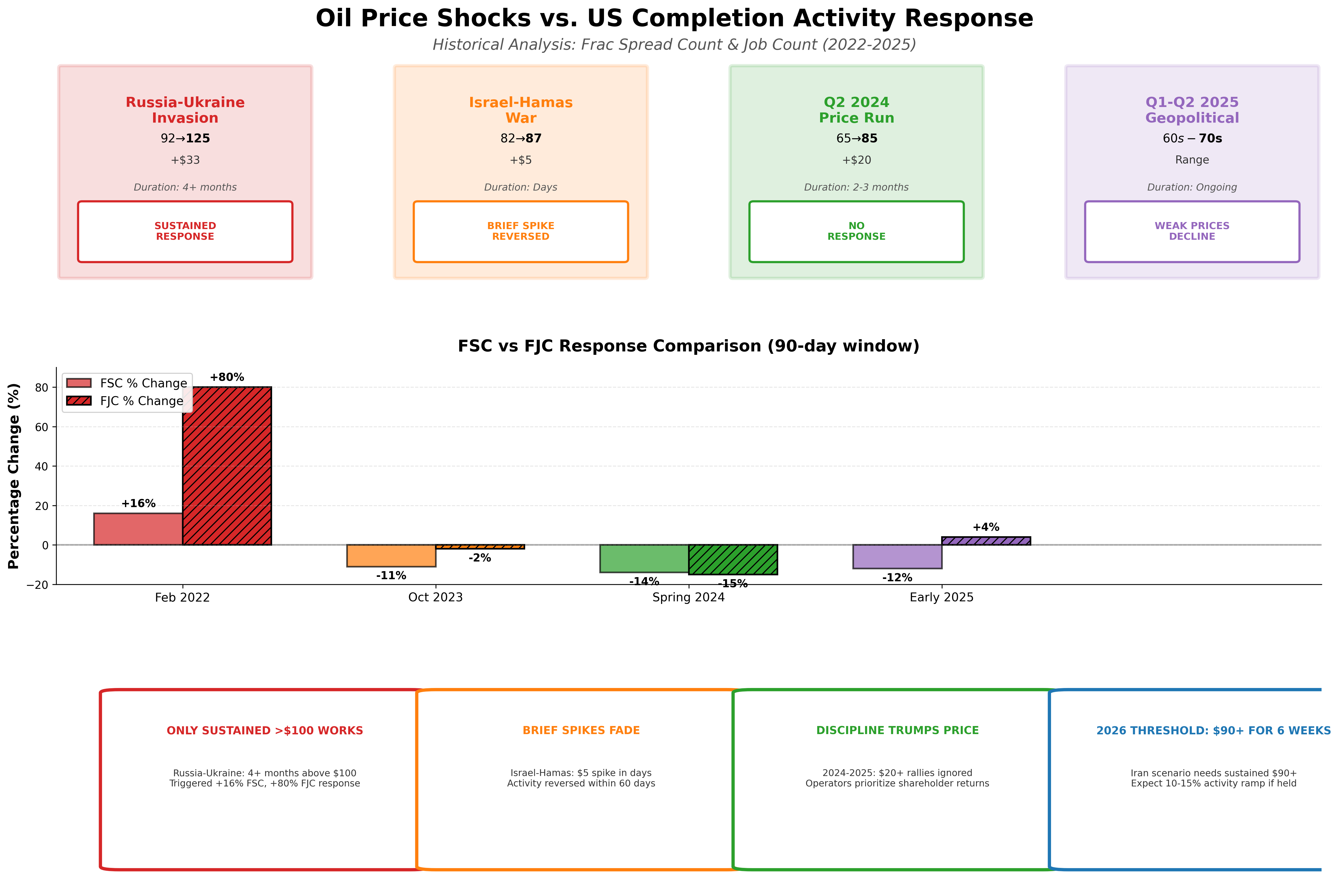

Historical data from Primary Vision shows the answer depends entirely on duration. When Russia invaded Ukraine in February 2022 and WTI surged from $92 to $125 per barrel, frac spreads climbed 16% over the following 90 days, rising from 244 in late December 2021 to 283 by early June 2022. That response reflected four consecutive months of oil trading above $100, giving operators confidence that marginal inventory would pencil. The Israel-Hamas conflict in October 2023 produced a different outcome. WTI spiked 6% from $82 to $87 but faded within days. Spreads ticked up 6% in the immediate 60-day window before collapsing 11% to 234 by January 2024 as prices rolled over. The 2024 spring rally from $65 to $85 generated zero activity response, with spreads declining 14% from 264 in mid-February to 228 by mid-July as operators maintained capital discipline. The pattern holds: sustained prices above $90 for six weeks trigger a 10-15% ramp in spread count within 90 days. Brief spikes fade without mobilizing capital.

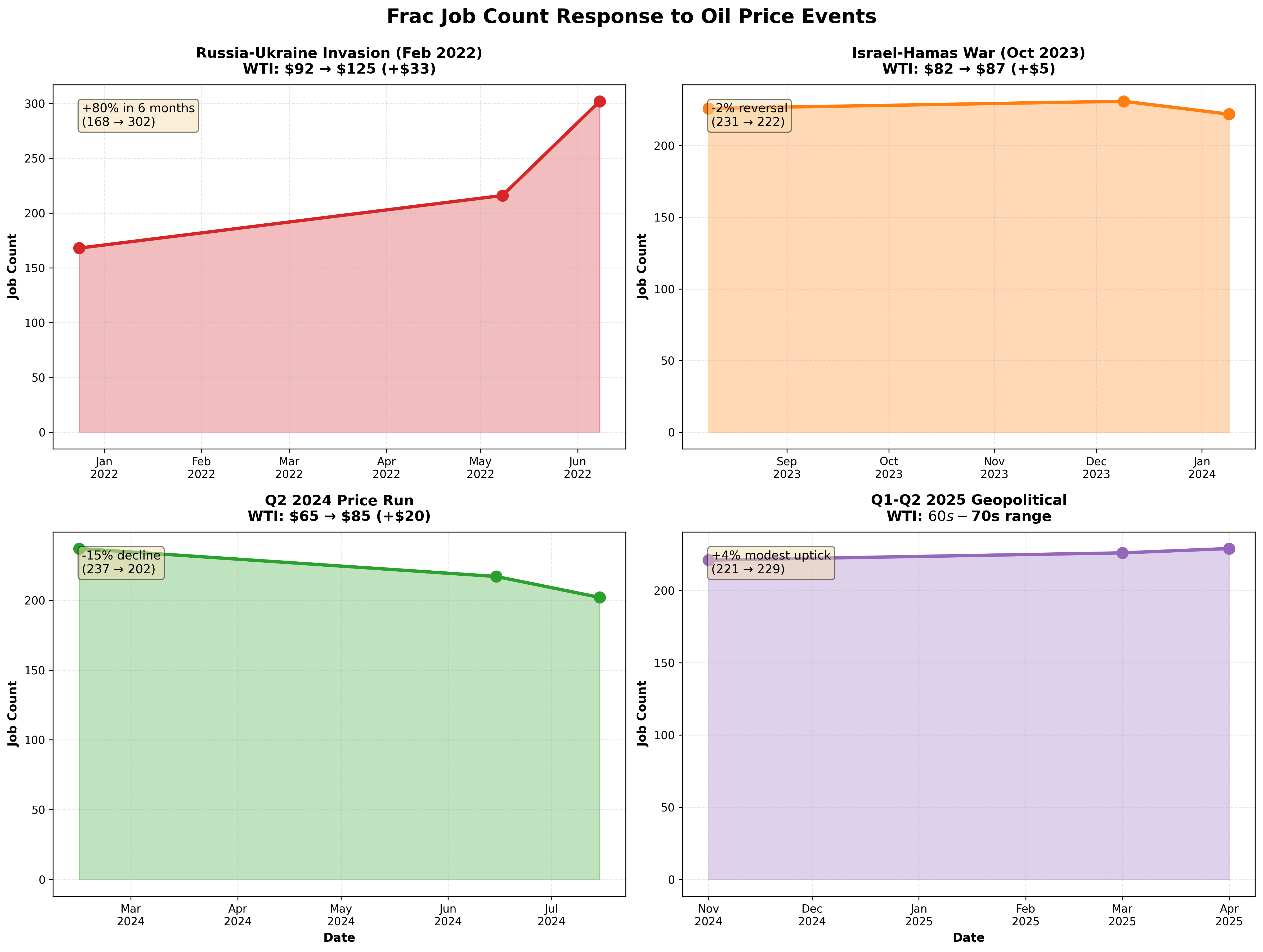

Running the same analysis on frac job count reveals an even more pronounced response pattern. When Russia invaded Ukraine in February 2022 and WTI surged from $92 to $125, job count exploded 80% over six months, climbing from 168 in late December 2021 to 302 by early June 2022. That outsized response relative to the 16% spread count increase shows operators maximized utilization of existing fleets before committing capital to add new spreads. The Israel-Hamas spike in October 2023 produced no meaningful job count response, with activity flat at 226-231 jobs through December before slipping back to 222 by January 2024 as prices faded. The 2024 spring rally actually coincided with declining job count, dropping 15% from 237 in mid-February to 202 by mid-July despite WTI climbing from $65 to $85. Job count has since stabilized in the low-220s range through early 2025, ticking up modestly to 229 by April before the current reading of 210. The pattern reinforces the same conclusion: operators gear up aggressively when prices sustain above $90 for multiple months, but ignore transient spikes regardless of magnitude. Job count responds faster and harder than spread count because utilization can flex immediately without fleet additions.

The conflict escalated dramatically over the weekend. Iranian drones struck Saudi Aramco's Ras Tanura refinery early Monday, triggering a small controlled fire at one of the world's largest export terminals. Iran's Revolutionary Guard announced a closure of the Strait of Hormuz on Saturday, broadcasting warnings that no vessels would be permitted transit. Shipping data shows at least 150 tankers anchored in open Gulf waters beyond the strait, with commercial traffic largely paused. The U.S. military responded by sinking nine Iranian naval vessels and destroying naval headquarters in Chabahar, targeting Iran's capacity to enforce the blockade. Some tankers are still moving through the waterway despite threats, though flow remains severely disrupted.

The immediate supply risk centers on whether this closure extends beyond days into weeks, cutting off roughly 20 percent of global oil. Markets had already priced in geopolitical risk premiums ahead of Saturday's strikes, with WTI climbing 15-20 percent from $62 in mid-February to current levels near $72. The latest frac spread count hit 167 this week, up seven from last week, while job count climbed to 210, up eight. These are the first meaningful increases since early Q4 2025, suggesting US shale is positioning for bonus economics if prices sustain.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform