Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Permian makes a comeback

By Osama on January 19, 2026 in Market Sentiment

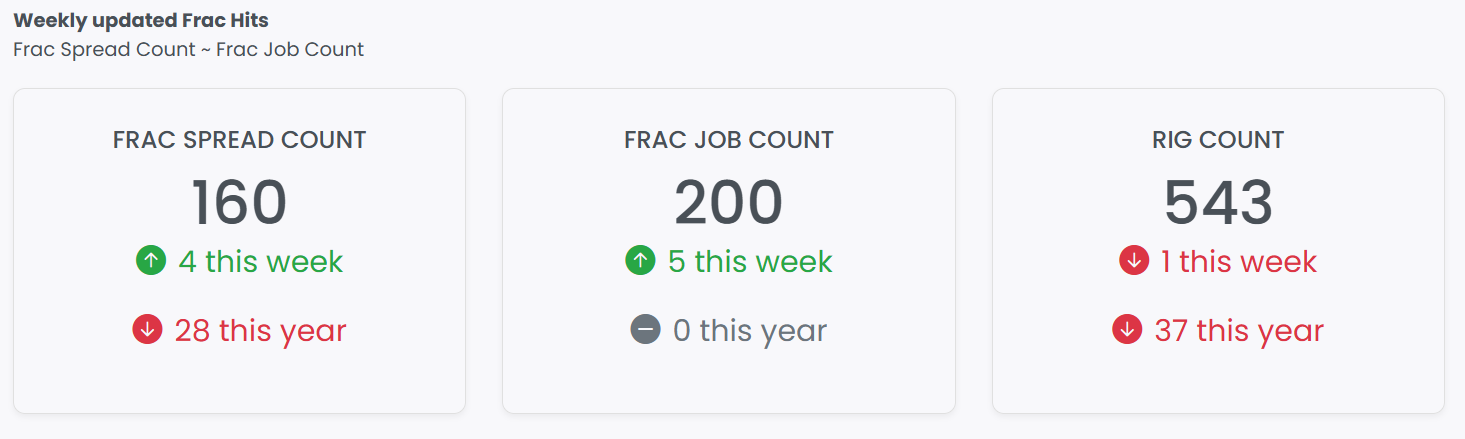

Primary Vision’s latest frac activity data shows a steady improvement in completion-side momentum as the industry moves into mid-January. The Frac Spread Count (FSC) rose to 160, up four spreads on the week, while the Frac Job Count (FJC) increased by five jobs to 200. Both indicators continue to trend higher after a soft finish to last year. On a year-over-year basis, FJC is now back to the same level it was this time last year, while FSC remains modestly lower, down 28 spreads year-over-year. Taken together, the data suggests that while absolute frac capacity has not fully recovered, utilization of that capacity is improving, pointing to a more active completion environment without a material expansion in idle equipment.

At the basin level, recent gains are being led by a noticeable pickup in Permian activity, consistent with operators prioritizing inventory that offers scale, infrastructure access, and comparatively resilient economics. At the same time, activity in the Williston Basin has also been building. This improvement is notable given broader market concerns around marginal basins and highlights the differentiated behavior between drilling sentiment and completion execution. We will be publishing a more detailed shale-level breakdown of FSC and FJC trends, including basin-specific dynamics and operator mix, in an upcoming note for enterprise subscribers.

Broader market developments over the past week underscore how capital allocation decisions are increasingly focused on scale, integration, and long-duration resource positions rather than short-term price signals alone. Mitsubishi Corporation’s agreement to acquire Aethon Energy’s Haynesville shale gas business for $5.2 billion represents a significant step by an international major into the U.S. shale gas value chain. The assets, producing approximately 2.1 Bcf/d, are strategically located near Gulf Coast LNG infrastructure, reinforcing the Haynesville’s role as a cornerstone supply basin for global gas markets. Consolidation narratives are also re-emerging in oil-weighted plays. Reports that Coterra Energy and Devon Energy are in discussions around a potential all-stock Permian-focused merger point to a renewed emphasis on scale efficiencies, inventory depth, and capital discipline. While no agreement is assured, the size of the companies involved suggests that operators see value in combining high-quality acreage positions rather than competing independently for incremental growth. This type of consolidation typically aligns with stable to improving completion activity, as larger combined entities seek to optimize development cadence rather than meaningfully cut back.

At the same time, Harold Hamm’s comments about potentially pausing drilling in the Bakken due to shrinking margins highlight the sensitivity of drilling economics to declining oil prices and rising costs have gathered a lot attention. However, it is important to distinguish between drilling decisions and completion activity already in the pipeline. Primary Vision’s data indicates that activity in the Williston Basin, which includes the Bakken, is not only holding up but has shown signs of incremental growth on the completion side.

In Williston, frac spread counts remain largely steady, easing only by a low single-digit percentage into late year, underscoring stable capacity. Frac job counts tell a different story. Activity was clearly depressed at the start of 2025, sitting at its cyclical low, before rebounding sharply through the middle of the year. From those early lows, frac jobs have increased by more than 100 percent, marking a strong recovery. Importantly, this rebound has transitioned into stability, with job counts holding within a narrow single-digit percentage range for the past several months. That contrasts with the early-year period, when week-to-week swings regularly exceeded twenty percent. The current pattern points to consistent execution and improved scheduling discipline, with utilization now better aligned to the steady frac spread base.

.png)

From a macro perspective, the combination of rising FJC, stable-to-improving FSC, strategic M&A activity, and selective drilling pullbacks points to a shale sector that continues to adjust and surprise on the upside. Operators appear focused on efficiency, execution, and balance sheet. While near-term price pressures remain a constraint, current frac activity data does not support a narrative of an imminent fall in U.S. shale production.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform