Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Shale Producers Plan to Increase Production

By Osama on November 17, 2025 in Market Sentiment

Welcome to this week's Monday Macro View! Last week was extremely busy with our Breakeven story making rounds and people contacting us to get more information about it. More articles on that topic are underway - keep an eye out. Oil prices remain rangebound. The debate between an expected surge in demand and impending oil glut (many believe it is already here - I tend to differ) will keep prices in check. Geopolitical flashpoints may cause wild swings on the upside.

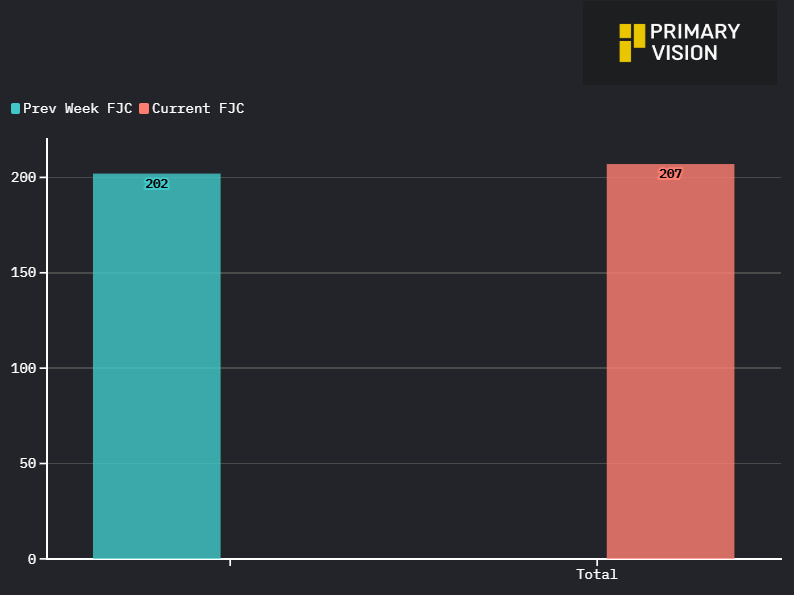

On Friday prices went up by 2% on account of an Ukrainian attack on Russian oil depot. But let's jump into the latest FSC and FJC numbers. The FSC registered an increase of 2 now standing at 175 while the FJC jumped by 5 on a WoW basis making the total at 207. At this point the job count is down only by 8 on a YoY basis.

NOTE: Primary Vision also distributes basin-level Frac Job Count forecasts that you might be interested in. Please contact me at osama@primaryvision.co for more information

Before jumping to other analysis, there is another insight I'd like to share with you. While going through the latest FSC and FJC numbers this week, along with a few other key developments in the oil markets one thing really stood out — the difference between what the EIA calls a “completion” and what we actually count as a frac job. It might sound like a small detail, but it really changes how you read the data. The EIA’s reported completions are often 20–25% higher each month than our Frac Job Count. At first glance, that makes it look like a lot more wells are being finished and brought online, suggesting production should be rising even faster. But when you break down what’s actually being counted, the picture changes.

Every frac job is technically a completion, but not every completion involves frac work. A frac job is what actually brings new production online. That’s the activity that adds fresh barrels. Meanwhile, a lot of what gets logged as a “completion” by the EIA includes things like tubing replacements, packer repairs, or other maintenance work. Those are necessary to keep wells producing, but they don’t increase output; they just maintain it.

That’s the key difference. The EIA numbers blend together true production-boosting work with maintenance activity, while our Frac Job Count filters that out and focuses on the jobs that actually create uplift. Understanding that distinction helps make more sense of why our data — and our view of production momentum often tracks the exact pulse of U.S. oil production.

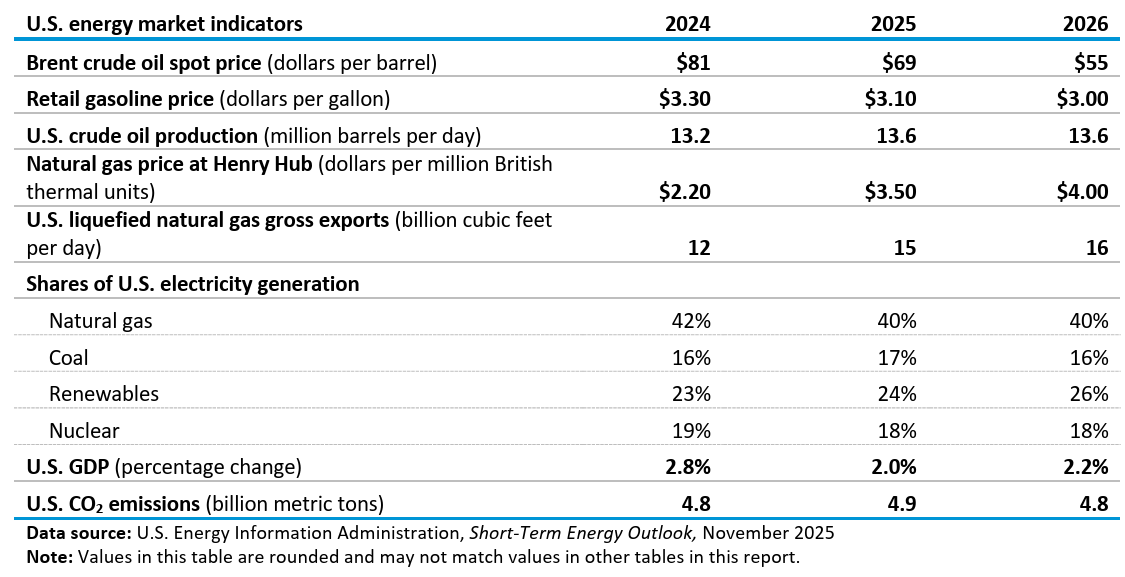

Nevertheless, as per the latest STEO by EIA, the U.S. oil production is expected to reach 13.6 mbpd next year, but the price is expected to decrease $55. This is a very significant point! It says a lot about what we have been saying lately. I will write about this next week in detail.

Now some interesting news coming out of the industry that further cements the strength of U.S. shale industry. This week, several major shale producers signaled plans to raise output, backing up what we’re seeing in our latest FJC and FSC data. Diamondback Energy said it will lift its 2025 oil production to around 495–498 thousand barrels per day, supported by a strong drilling and completion program across the Midland Basin. Coterra Energy also nudged its production guidance higher, targeting roughly 772–782 thousand barrels of oil equivalent per day for 2025, with steady growth expected into 2026. Ovintiv raised its own forecast to about 610–620 thousand barrels of oil equivalent per day, citing strong well performance and efficiency gains. And Exxon Mobil, now the largest operator in the Permian Basin, increased its 2025 output target by another 100,000 barrels of oil equivalent per day to reach about 1.6 million. Despite softer oil prices, these companies are clearly positioning for more activity — more wells, more completions, and more frac jobs — which lines up closely with our projections showing an uptick in field operations through late 2025 and into 2026.

Next week we will look at the plans for 2026 and what can we expect in terms of activity and production coming out of not only the U.S. but also other parts of the world as well. Stay tuned.

Happy Reading!

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform