Articles

- BLOG / Articles / View

- Articles

Monday Macro View: U.S. frac'ing goes international

By Osama on January 26, 2026 in Market Sentiment

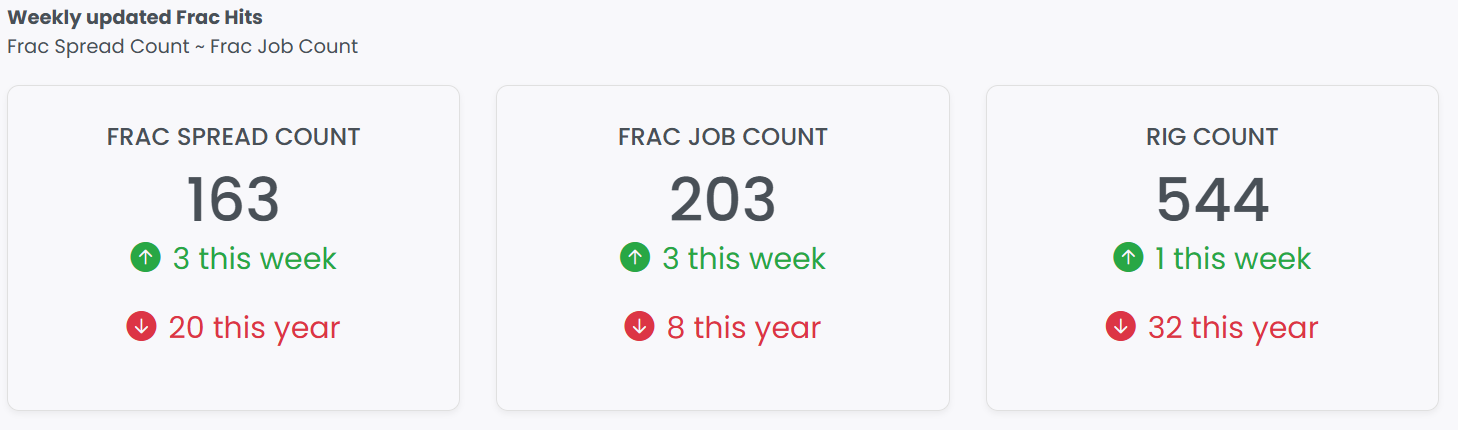

The latest numbers are in. Frac Spread Count (FSC) and Frac Job Count (FJC) both registered gains - again - this week. The FSC increased by 3 on a week on week basis and the FJC also increased by the same number. The FSC is now down by only 20 on a YoY basis while FJC is down by 8. Oil prices continue to rise given rising uncertainty regarding the geopolitical landscape especially in Middle East. If we remain higher for longer than further upward movement in drilling activity can be expected.

There are other interesting developments as well. We have been tracking unconventional activity across multiple geographies, including developments in Mexico and recent work in China. That broader monitoring highlights how uneven progress remains outside North America. Against that backdrop, it is useful to focus on a narrower question: what US shale operators are planning internationally, and how those plans fit within current capital and operational constraints?

In 2025, several US producers have begun deploying horizontal drilling and completion expertise outside the United States. These initiatives remain selective and measured, but they reflect a willingness to test whether techniques honed in US shale can translate into commercial results elsewhere. The projects underway share a common feature: they are structured to limit upfront exposure while preserving upside if early results prove encouraging.

One of the clearest examples is Continental Resources, which in 2025 announced a joint venture with Turkey’s national oil company and TransAtlantic Petroleum to evaluate unconventional resources in the Diyarbakir and Thrace basins. Initial resource estimates published by Turkish Petroleum point to sizeable oil and gas potential, but Continental’s approach remains exploratory. Capital commitments are modest relative to its US portfolio, and the focus is on delineation rather than rapid development. The broader implication is that international shale is being treated as an inventory option.

EOG Resources has taken a similar stance in the Middle East. In early 2025, the company entered into an agreement with Bapco Energies to evaluate a gas prospect in Bahrain, with EOG acting as operator. Management emphasized that previous horizontal tests delivered positive results, but activity remains contingent on further approvals and technical appraisal. Gas-weighted projects like Bahrain are notable, as international demand centers and pricing structures differ materially from US markets, shaping both development pace and return expectations.

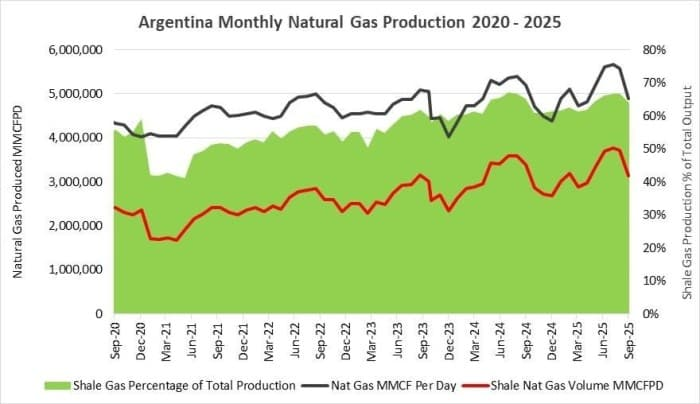

Latin America continues to attract sustained attention, particularly in Argentina’s Vaca Muerta. Chevron has maintained steady capital deployment there through 2025, applying factory-style drilling while adapting to local cost and regulatory conditions. Production growth has been tangible, but execution costs remain higher than in the Permian, and project economics rely heavily on fiscal stability. For US operators, Vaca Muerta represents a more advanced case of international shale development, albeit one that has required patience and long-term commitment.

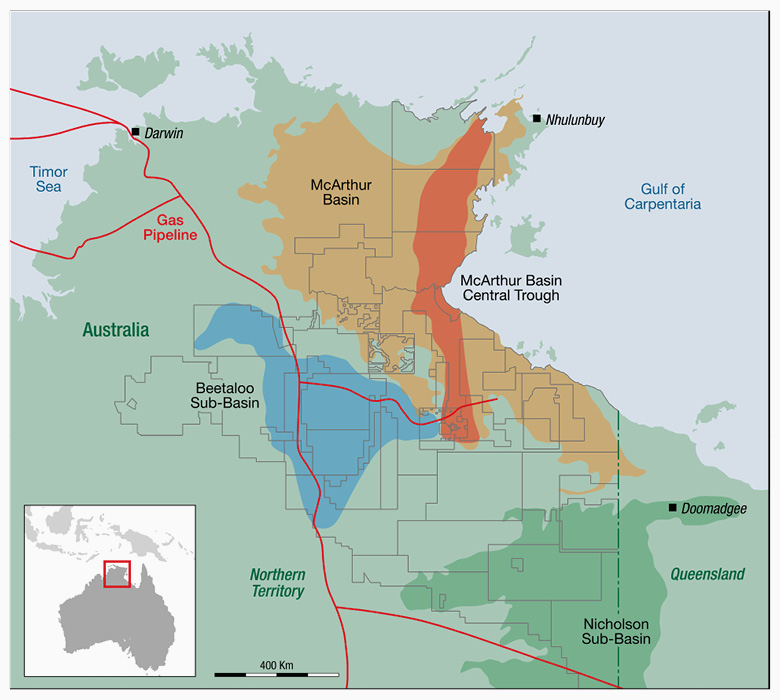

Elsewhere, US-linked shale expertise is being tested in earlier-stage settings. Tamboran Resources has advanced pilot gas drilling in Australia’s Beetaloo basin, supported by US service companies and capital. Murphy Oil and APA continue to operate internationally across Asia, Africa, and South America, though their equity performance in 2025 underscores persistent investor skepticism toward overseas exposure.

That skepticism reflects structural realities. International unconventional projects lack the dense service infrastructure, standardized contracting, and rapid cycle times that underpin US shale efficiency. Regulatory timelines, local content requirements, and logistics can slow learning curves and inflate costs. As a result, even technically successful wells do not guarantee competitive full-cycle returns.

From an industry perspective, the key variable to watch is not whether individual international wells are technically successful, but whether operators choose to commit repeat capital after initial appraisal. That suggests management teams view these efforts as strategic probes rather than parallel growth platforms. For Primary Vision, this distinction matters. Pilot activity abroad may generate incremental frac'ing demand, but it is unlikely to alter global completion intensity or equipment utilization in a sustained way unless operators demonstrate confidence through multi-year drilling programs. Until then, international shale remains an extension of technical capability, not a driver of structural change in upstream activity patterns.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform