Articles

- BLOG / Articles / View

- Articles

Monday Macro View: US shale adjusts to lower oil prices by cutting costs

By Osama on December 22, 2025 in Market Sentiment

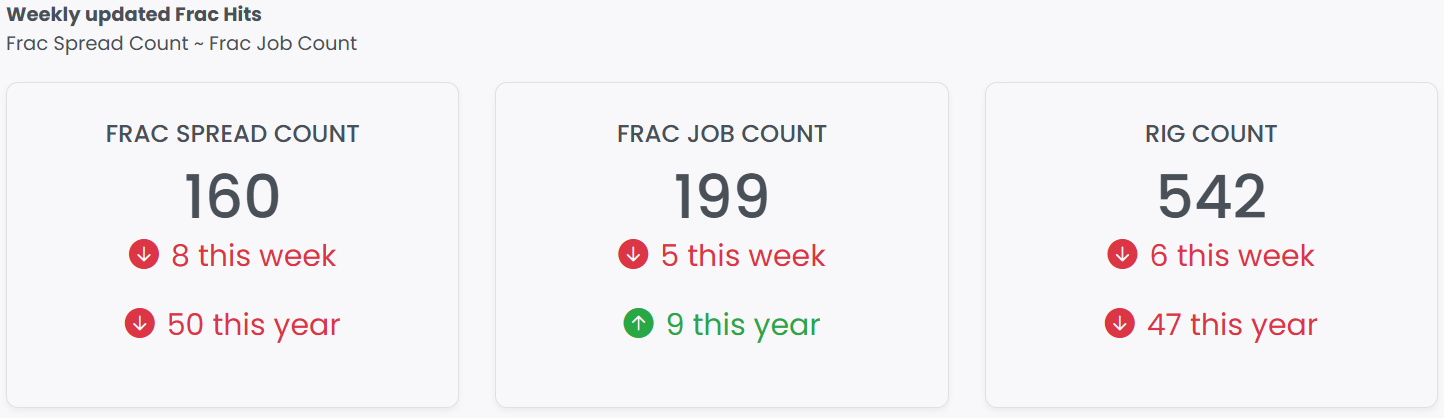

Welcome back to the Monday Macro View. We open this week with Primary Vision’s latest snapshot of U.S. completion activity. The Frac Spread Count currently sits at 160, down 8 on the week and 50 lower year-over-year, while the Frac Job Count stands at 199, down 5 this week but up 9 jobs on a YoY basis. Rig count continues to grind lower at 542, down 6 on the week and 47 versus last year. The headline takeaway remains consistent with recent months: fewer active assets, but steady execution intensity across the system.

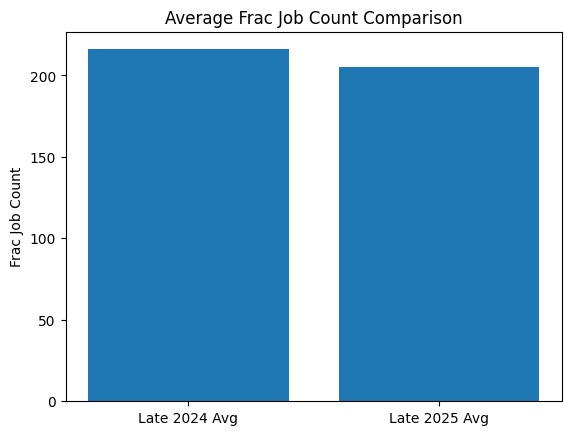

What makes this setup interesting is the behavior of the Frac Job Count. Despite a materially lower FSC, FJC is running higher year-over-year, pointing to rising utilization per spread. Looking at the weekly data, average FJC levels in late 2024 were approximately 216, versus roughly 205 over the comparable weeks in 2025—a decline of about 5%. That moderation is real, but it is modest relative to the decline in spreads, reinforcing the view that operators and service providers are extracting more work from a smaller, more modern fleet rather than pulling back meaningfully on completions.

Source: Weekly Report, Primary Vision

Recent commentary in the broader market has emphasized declining shale productivity and the idea that U.S. operators are running into natural limits after years of faster drilling, tighter spacing, and longer laterals. However, Primary Vision data points to a different conclusion on where the system is heading. Rather than a loss of capability, what we are seeing is a reconfiguration of horsepower, fleets, and workflows that is materially increasing utilization per frac spread. Horsepower deployment per active spread has roughly doubled compared to pre-2020 configurations, while legacy, lower-intensity equipment continues to be shed from the system. The result is fewer spreads doing substantially more work.

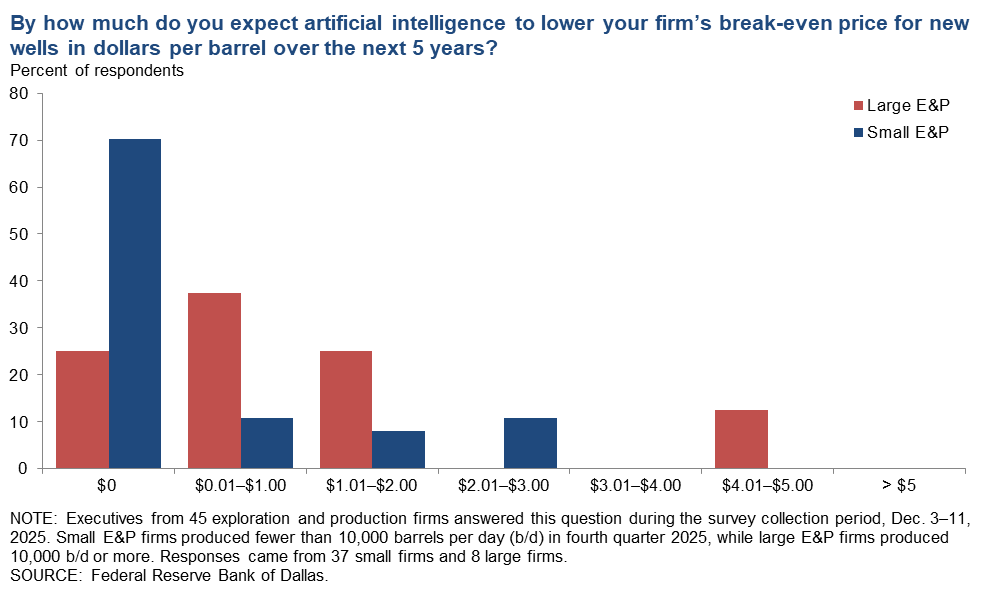

Importantly, these gains are not just mechanical. The Dallas Fed Energy Survey reinforces this shift, with most large E&P executives expecting AI to help lower breakeven prices for new wells over the coming years. Nearly 60% of oilfield services firms expect AI to extend equipment life, while close to 80% do not expect AI to replace personnel, underscoring that adoption is focused on efficiency rather than headcount reduction. From real-time optimization to predictive maintenance, AI tools are increasingly embedded in execution, not deployed as pilots at the margins.

Against this backdrop, pricing is the real stress test. Oil prices are down more than 20% year-over-year, yet the system continues to generate cash. Our breakeven series shows how and the Dallas Fed energy survey corroborates the calculations: Exxon’s portfolio-weighted breakeven is now around $40–42/bbl, roughly $10–15/bbl lower than five years ago. Despite the price decline, the four majors generated over $21 billion in combined net income in Q3, highlighting how structurally lower costs and higher efficiency are cushioning earnings even in a softer price environment. Capital allocation decisions reinforce this view. JAPEX’s $1.3 billion acquisition in the DJ Basin is emblematic of how international capital is approaching U.S. shale today. This is not a bet on rapid rig or spread growth. It is a long-cycle investment in a mature basin where value will be created through disciplined development, modern completion designs, and rising recovery per well over time. For the service market, this implies steady, high-intensity demand rather than cyclical expansion.

As we look into 2026, the structural dynamics of the oil and gas industry are increasingly shaped by technological maturation and market pressure rather than cyclical volume expansion. Independent forecasts now suggest that WTI and Brent prices may trend in the low-to-mid-$50s through 2026, underscoring persistent downside risk relative to corporate expectations. In this environment, capital discipline and digital transformation will be primary operational levers: AI, digital twins, predictive analytics, and IoT-enabled optimization are moving from pilot to enterprise-wide adoption, embedding real-time decision systems into drilling, completions, predictive maintenance, and midstream logistics. Meanwhile, on the upstream side, shale output growth is possible—supported by operators with scale and Permian strength. Collectively, these factors suggest 2026 will be a year where efficiency and digital capability, not sheer activity levels, determine competitive advantage, pressure service pricing floors, and reorient cash returns toward optimized asset performance rather than expansion.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform