Articles

- BLOG / Articles / View

- Articles

Nabors Industries’ Perspective in Q4 2025: KEY Takeaways

By Avik on March 13, 2026 in Articles

Industry Outlook

We have already discussed Nabors Industries' (NBR) Q4 2025 financial performance in our recent article. Here is an outline of its strategies and outlook. Oil prices trended lower in 2H25 amid global oversupply, tariff uncertainty, and geopolitical tensions. The EIA showed that future pricing will depend on OPEC and non-OPEC output, inventory builds, and demand growth concentrated in Asia.

Internationally, NBR is positioned to benefit from regional production growth and is evaluating a potential return to Venezuela, where five rigs remain idle. In the U.S., Lower 48 operators are focused on maintaining production but remain ready to adjust activity if returns weaken. In natural gas, fundamentals are strengthening. LNG and domestic demand are rising, gas-directed rig counts are up, and further drilling upside is possible.

SANAD Update

NBR’s SANAD JV deployed its 14th newbuild rig in Q4, with five more set for 2026. It will bring the fleet to 19, and a 20th is expected in early 2027. Two of three suspended rigs are returning to work under existing contracts. However, three low-earning legacy rigs were not renewed and are being evaluated for redeployment. Broader Eastern Hemisphere momentum is building, with nearly 20 additional rig opportunities under review across current operating markets.

NA Outlook and Balance Sheet Strength

According to NBR’s management, the largest Lower 48 operators expect activity to remain broadly stable through 2026. Two companies anticipate modest declines, while most others see flat to slightly higher rig counts. Management expects FY2026 EBITDA to match FY2025, with operational gains offsetting the Quail disposition (During Q3, Nabors sold Quail Tools for $625 million) and supporting further debt reduction. Net debt has fallen by more than $550 million, reducing interest expense and supporting free cash flow.

Rig Count and Financial Forecast

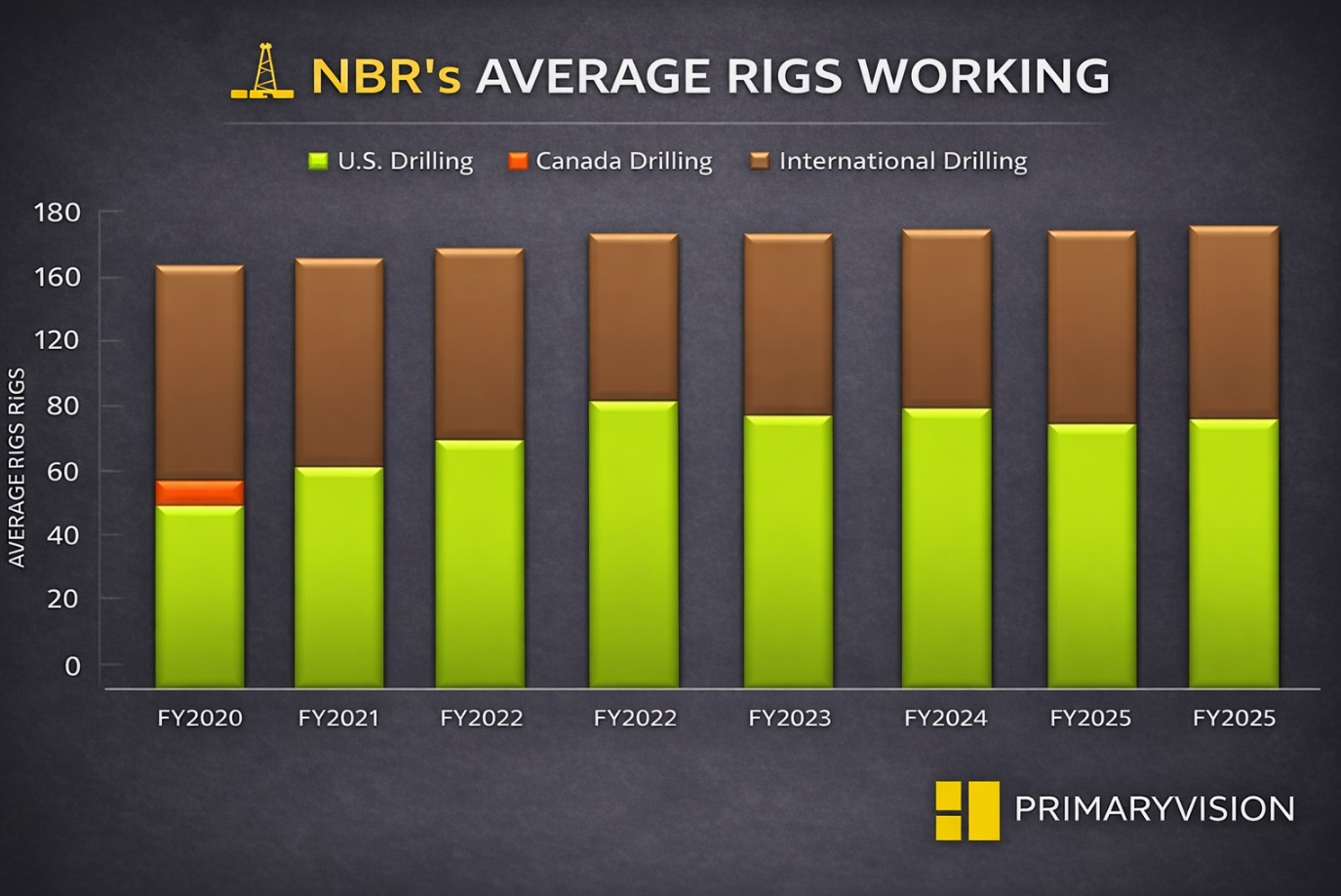

NBR’s onshore count is expected to rise sequentially to 64–65 rigs in the near term before stabilizing in the 61–64 range for FY2026. Its daily margins can decline by 1%, reflecting margin compression from scope changes and lower activity.

International rig count is set to expand to 96–98 rigs, exiting the year at 101. Among these will be five Saudi newbuilds, two reinstated suspended rigs, and two redeployments in Argentina, with daily margins targeted to rise 5% to about $18,500. Overall, FY2026 EBITDA is expected to grow 6%–8%, led by international and Drilling Solutions growth, with no contribution assumed from potential Venezuela reactivations.

Credit Rating Improves

Nabors issued $700 million of 7.5% notes due 2032 to retire near-term maturities and later redeemed $379 million of 2028 notes, extending its maturity runway to mid-2029 with only $250 million due. These actions strengthened the balance sheet and led two credit rating agencies to upgrade parts of its debt structure.

Relative Valuation

NBR is currently trading at an EV/EBITDA multiple of 3.9x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is slightly higher. The current multiple is also lower than its five-year average EV/EBITDA multiple of 5.8x.

NBR's forward EV/EBITDA multiple expansion versus the current EV/EBITDA is less steep than its peers because the company's EBITDA is expected to decrease less sharply than its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple compared to its peers. The stock's EV/EBITDA multiple is lower than its peers' (NINE, PUMP, and ACDC) average of 5.3x. So, the stock is undervalued compared to its peers.

Final Commentary

Oil markets remain pressured by oversupply and geopolitical uncertainty, but NBR is positioned to benefit from international growth and strengthening natural gas demand. SANAD continues to expand with newbuild deployments and reinstated rigs, supporting rising Eastern Hemisphere momentum. In North America, activity is expected to remain broadly stable, with 2026 EBITDA projected to match or grow modestly versus 2025 despite the Quail divestiture.

International rig count is set to increase meaningfully, driving margin expansion and underpinning 6–8% EBITDA growth in 2026. Balance sheet actions have extended maturities, reduced net debt by over $550 million, and improved credit ratings, reinforcing financial flexibility. The stock is undervalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform