Articles

Free Read: Frac Spread Count, Oil prices and Russian Oil

By Osama on February 4, 2026 in Free Articles

As always let's start this week's Free Read with the latest Primary Vision’s Frac Spread Count (FSC) and Frac Job Count (FJC) numbers. The FSC fell by an unusually large 15 spreads week over week, marking one of the steepest weekly declines seen in recent months, while the Frac Job Count also recorded a notable drop, in double digits, making many readers panic as to what is happening in the shale patch. Such a sharp move inevitably raises questions about whether US supply growth is facing a structural slowdown or whether this is a seasonal adjustment. In this week’s Monday Macro View, I explore that question in detail, examining whether the decline reflects a deeper shift in shale economics or a temporary pause that may reverse as spring approaches.

Beyond supply dynamics in the US, oil prices continue to draw support from geopolitical developments that have reintroduced risk premiums into the market. Oil prices have held firm so far in 2026, even as expectations of surplus continue to dominate medium-term forecasts. Several events have contributed to this resilience, including the arrest of Venezuela’s president by US authorities and renewed tensions between the US and Iran, developments that raise risks around crude supply from politically sensitive regions. A direct escalation involving Iran would place roughly 1.5 million barrels per day of Iranian exports at risk and could heighten concerns over oil flows through the Strait of Hormuz, where close to 20 million barrels per day of crude moves daily.

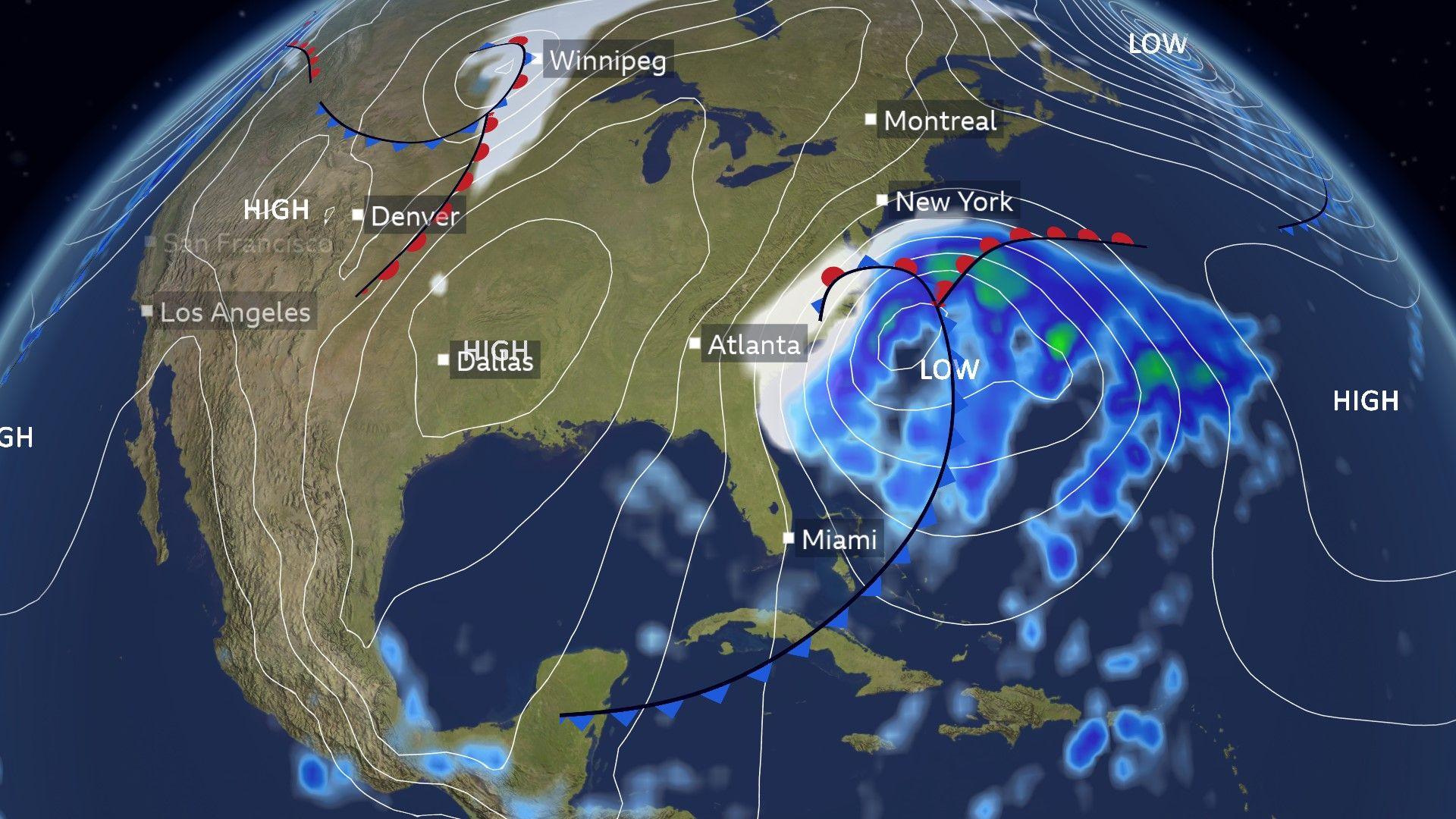

At the same time, severe winter weather across parts of the United States has boosted heating fuel demand while posing localized risks to oil production and refinery operations, reinforcing price support during the peak winter period.

However, the broader picture highlights that bearish factors still exist. Analysts continue to highlight that the scale of expected surplus later in the year implies that oil prices may come under pressure if geopolitical tensions ease and physical disruptions fade. Forward market indicators reflect this caution, with Brent timespreads strengthening in the prompt but remaining vulnerable. Expectations remain that ICE Brent could average around $57 per barrel by late 2026 if surplus conditions assert themselves more fully.

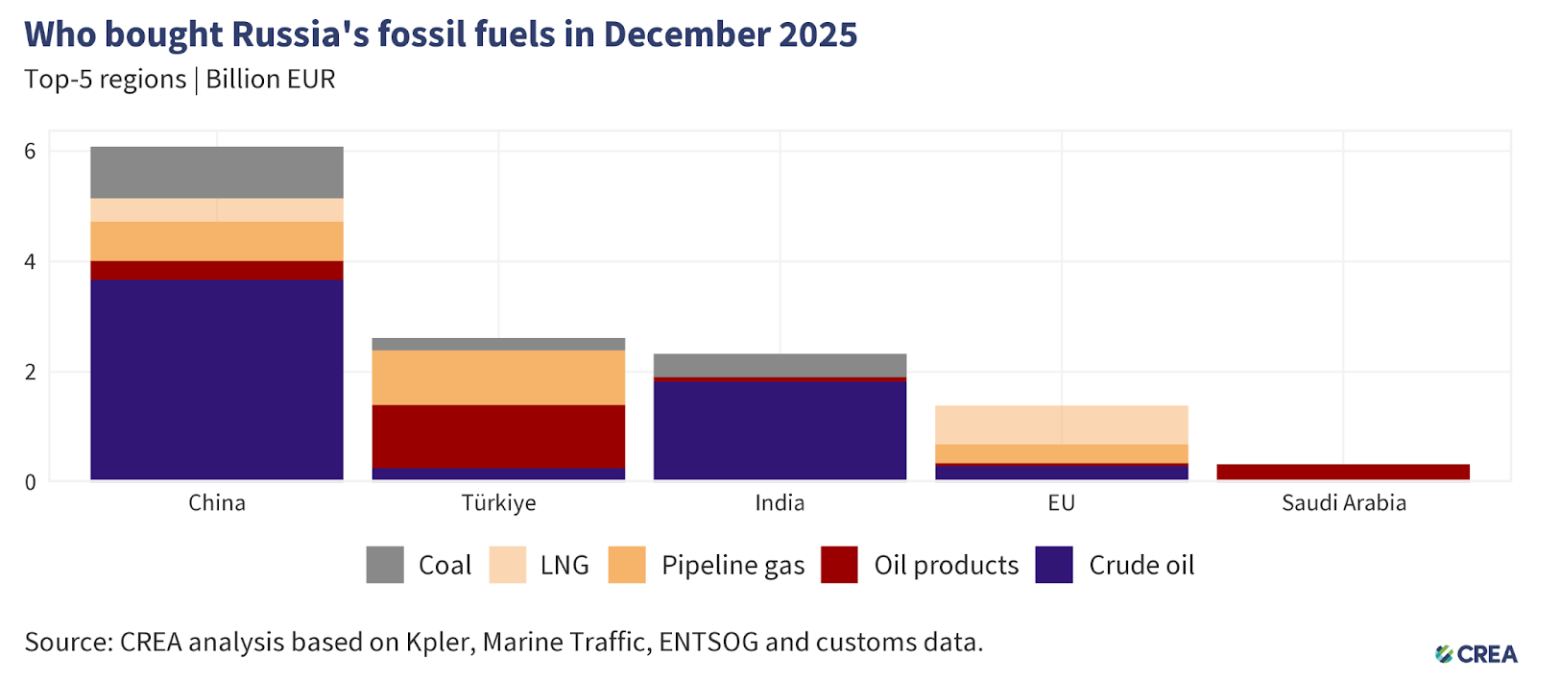

Another issue increasingly shaping oil market discussions is India’s evolving stance on Russian crude. In early 2026, India signaled to Western partners that it would seek to limit purchases of Russian oil where alternatives are available, stopping short of announcing an outright ban but acknowledging political pressure around energy trade. This matters because India imported roughly 4.8 to 5.0 million barrels per day of crude oil in 2025, meeting close to 87 percent of its total oil demand through imports. Within that import basket, Russian crude accounted for about 27.4 percent of India’s total imports in December 2025, making Russia the single largest supplier that month, while Russia’s average share across 2024–25 was closer to 35 percent due to heavily discounted barrels. Iraq remained the second-largest supplier, delivering roughly 850,000 to 900,000 barrels per day, equivalent to about 15–20 percent of India’s imports, with Saudi Arabia and the UAE together supplying another 20–25 percent. Iraq has theoretical capacity to increase exports, supported by plans to raise production capacity toward six million barrels per day later this decade and by upgrades to southern export infrastructure, including new marine pipelines. You can read more about this here.

Market positioning data suggest that traders are taking these geopolitical signals seriously despite oversupply narratives. While 2026 has been widely described as a year of excess supply, January prices largely matched last year’s levels, with ICE Brent averaging $64.7 per barrel for the month and closing January at $70.7 per barrel, defying weaker demand expectations. President Trump’s inconsistent rhetoric on Iran, shifting from threats of rapid military action to agreement on high-level nuclear talks in Istanbul, has helped restore oil’s geopolitical premium after it faded late in 2025. Reflecting this shift, open interest in ICE Brent futures climbed to a record 2.65 million contracts on January 26 before retreating by more than 200,000 lots in recent sessions. Hedge fund positioning has moved in parallel, with the net length held by money managers in ICE Brent futures and options doubling since the start of 2026 to 246,917 contracts, the highest level since early September 2025, signalling renewed speculative optimism despite the looming surplus.

Taken together, the oil market entering February reflects a tension between near-term geopolitical support, slowing US shale signals, and a still-intact oversupply outlook for later in the year, with pricing increasingly shaped by how long political risk can outweigh structural balances.