Articles

- BLOG / Articles / View

- Articles

Pressure Pumping Ranking in Q1: Capacity Tightening Begins to Matter

By Avik on June 10, 2026 in Articles

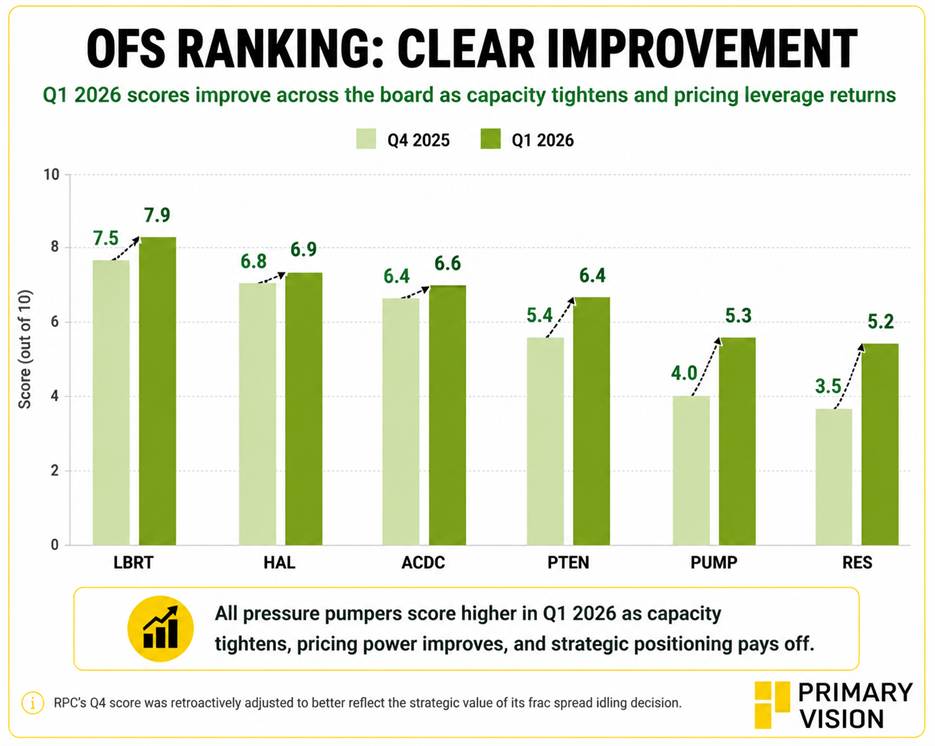

Ranking Pressure Pumpers in Q1

This analysis evaluates Halliburton, Liberty Energy, ProFrac (ACDC), Patterson-UTI, ProPetro, and RPC using the same framework applied in prior quarters. The focus remains on how effectively companies convert market conditions into operational performance.

The Q1 update reflects a market that is becoming increasingly constructive. Activity has not accelerated dramatically, but utilization remains high, frac spread attrition is reducing available capacity, and operators are beginning to discuss pricing improvements. The ranking order remains unchanged, but score dispersion narrows as industry conditions become more supportive. Read our previous article to know more.

Liberty Energy: Leadership Holds

Liberty retains the top position and improves its score from 7.47 to 7.90. The company continues to demonstrate the strongest execution profile in the group through high frac spread utilization, operational efficiency, and technology-driven optimization.

What differentiates Liberty increasingly is its ability to extend beyond traditional pressure pumping. Management continues to emphasize digiPrime, Liberty Advanced Equipment Technologies, and Liberty Power Innovations. Power generation and data center opportunities provide an additional growth vector that few peers can match. Liberty remains the benchmark against which the rest of the sector is measured.

Halliburton: Strong Position, Limited Change

Halliburton remains second with its score improving modestly from 6.78 to 6.90. The company continues to benefit from its scale, technology portfolio, and international diversification.

Management highlighted improving North American conditions while international operations helped offset regional disruptions. Technologies such as ZEUS and LOGIX continue to support performance as well complexity increases. Halliburton’s positioning remains strong, but the improvement in industry conditions appears to benefit some peers more directly, limiting relative score expansion.

PTEN and ACDC: Different Paths to Similar Rankings

Patterson-UTI records one of the largest score increases in the group, improving from 5.40 to 6.40. Management reported near-full utilization across active completion fleets while discussing pricing increases with customers. Those comments represent one of the clearest indications that frac capacity is tightening.

ACDC remains narrowly ahead in the rankings, with its score improving from 6.40 to 6.60. The company continues to execute well operationally and benefits from efficiency improvements and disciplined deployment. However, unlike Patterson-UTI, it lacks a direct catalyst tied to tightening frac spread availability. As a result, PTEN closes much of the gap despite remaining one position lower.

ProPetro and RPC: Improving Conditions Lift the Bottom Tier

ProPetro records a meaningful improvement, with its score increasing from 4.03 to 5.30. While completions remain under pressure, PROPWR is becoming increasingly relevant. Management continues to highlight power generation opportunities, including data center exposure and expanding generating capacity. The result is a broader investment case than pressure pumping alone.

RPC remains last in the ranking but posts the largest score improvement, rising from an adjusted 3.50 to 5.20. The company’s decision to idle a frac spread in 2025 initially appeared defensive. However, tightening capacity and improving pricing discussions increasingly validate that decision. RPC still lacks the scale and technology advantages of larger competitors, but industry conditions are beginning to work in its favor.

What Changed From Q4

The shift from Q4 to Q1 is not primarily about execution. It is about positioning. In Q4, execution quality separated operators in a soft market. In Q1, the discussion increasingly centers on frac spread availability, pricing leverage, power generation opportunities, and capital discipline. Operators with exposure to these themes recorded the largest score improvements.

Execution remains important. However, the market is beginning to reward companies positioned for the next phase of the cycle rather than those simply navigating the current one.

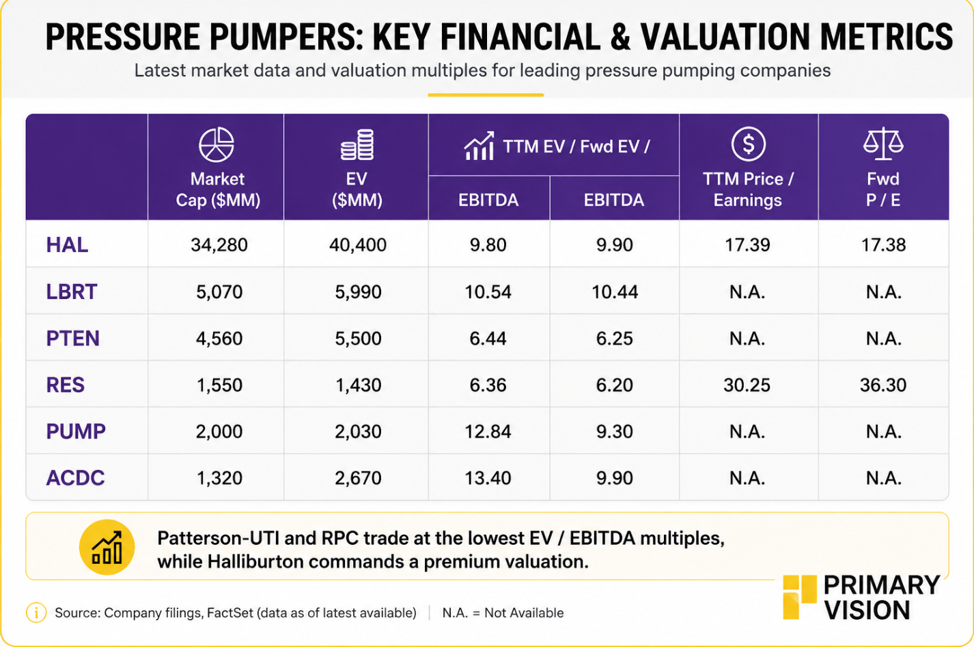

Relative Valuation

RPC remains one of the more attractively valued names despite its lower ranking position. Patterson-UTI also screens favorably given improving utilization and pricing conditions. Liberty continues to command a premium valuation, reflecting both execution consistency and growing exposure to power-related opportunities.

Takeaway

The Q1 update suggests that pressure pumping is entering a different phase of the cycle. Leadership remains intact, but the gap between operators is narrowing as capacity tightening becomes increasingly important. Liberty remains the execution leader, while Halliburton continues to benefit from technology and scale.

The most notable developments are occurring beneath the top tier. Patterson-UTI, ProPetro, and RPC all benefit from themes that carried less weight only a few quarters ago. I think the sector is gradually transitioning from an execution-driven ranking to one where pricing power, frac spread quality, and exposure to power infrastructure play a larger role in determining leadership.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform